A lease separates the legal ownership of an asset from its use. The legal owner (lessor) allows the user (lessee) to enjoy the use of the asset, in return for periodic cash instalments.

The Financial & Management Accounting (FMA) syllabus covers just the current rules for accounting by the lessee. So this article is about lessee accounting only.

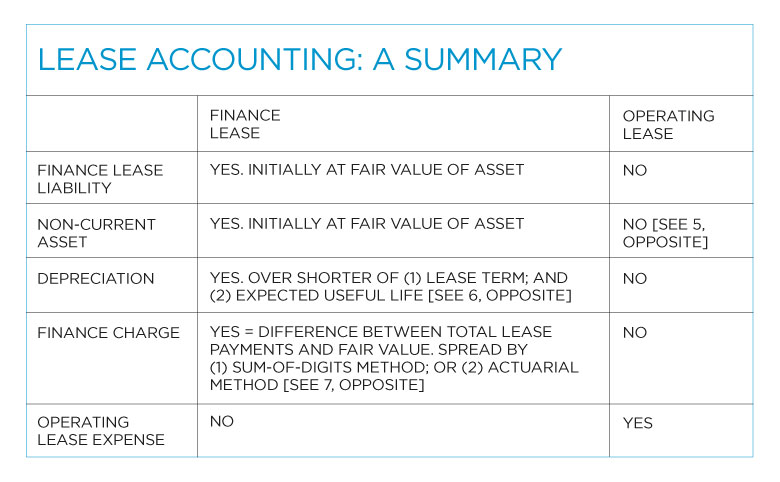

The lease accounting rules are an application of the ‘substance over form’ principle. Put simply, any leasing arrangements, which are effectively: firstly, ownership of the asset; and secondly, linked borrowings, must be accounted for as if they were an outright borrowing. (These arrangements are known as ‘finance leases’.) Importantly, the lessee must include an appropriate finance lease liability in its balance sheet (comparable with a loan taken out to finance the capital cost of the asset).

This is the inherently harder (and different) part of lease accounting. Perhaps for this reason most candidates tend to practise it, and to do very well at it.

All other leases – known as ‘operating leases’ – are accounted for more simply in exactly the same way as any other standard expense. This is the area where more practice can yield many more exam marks.

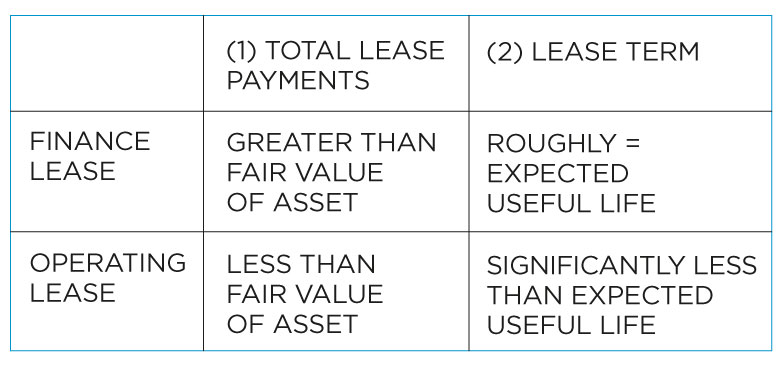

“Almost everyone identified that lease 1 was an operating lease and lease 2 a finance lease. Some, however, did not explain why this was the case, but merely stated their conclusion. This lost marks.”FMA Examiner’s Report

The most important reasons to write about are: the total lease payments, compared with the initial fair value of the asset; and the lease term, compared with the expected useful life of the asset.

In the case of a finance lease: the total lease payments normally cover the entire fair value of the asset, plus a return on top for the owner/lessor; and the remaining useful life at the end of the lease – if any – is not significant.

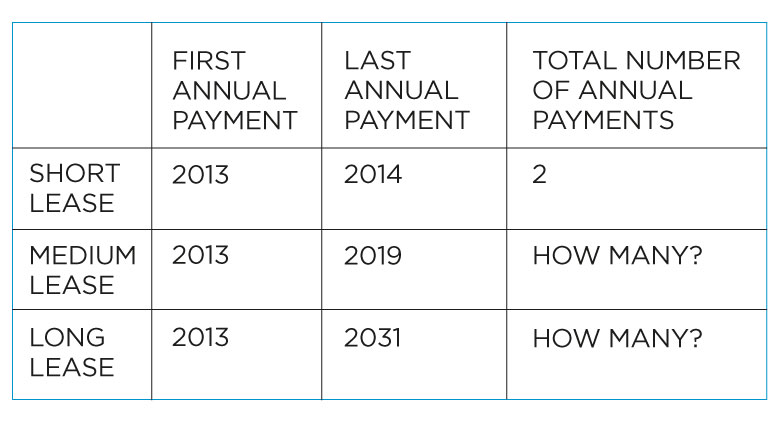

“The main problems included calculating the total amount payable [based on counting annual payments of £40,000 each].” FMA Examiner’s Report

Many of us find the number of payments between two inclusive dates: obvious for very short periods; but strange for very long periods (with one more payment than we might have expected). Consider the table below, relating to three different leases:

The short lease has two payments, in 2013 and 2014. This can also be calculated from the related years as (2014 – 2013 = 1) + 1 = 2.

The pattern here is that:

Total number of annual payments = difference in years + 1

The medium lease has seven payments (not six), in 2013, 2014, 2015, 2016, 2017, 2018 and 2019. This can similarly be calculated as (2019 – 2013 = 6) + 1 = 7.

In the same way, the long lease has 19 payments (not 18), in 2013 to 2031 inclusive, if you can count all these years individually and not lose count. Or this can more quickly be calculated as (2031 – 2013 = 18) + 1 = 19.

The exam question here included payments of “£40,000 annually on 1 March 2012 to 2018 inclusive”.

How many payments of £40,000 were there? (Answer: seven: in 2012, 2013, 2014, 2015, 2016, 2017 & 2018. Not six. (April 2012, Q5.)

“As the lease was not entered into until 1 March, only 10 months’ cost should be included in the statement of comprehensive income for the year ended 31 December. Many charged for a full year.”FMA Examiner’s Report

Operating lease expenses are spread on a straight-line basis over the lease term. In this exam question, the annual expense (per 12 months) was £38,750. With a 31 December year end and a 1 March starting date, the correctly calculated charge for the 10-month period was £38,750 x 10/12 = £32,292.2 (Note: 2 April 2012, Q5)

Year ends are not always so helpfully on 31 December. An earlier exam included another question with an operating lease starting on 1 March, for a company with a year end of 30 September. How many months’ charge should be included? (Answer: seven: for March, April, May, June, July, August and September. (April 2011, Q5.)

“Most correctly calculated the average annual cost was £70,000, but then struggled to work out that as the lease had only run for seven months of the current year and because the company had paid £65,000 in the year there was a prepayment at the year end.” FMA Examiner’s Report

If there’s a difference between the accounting charge and the lease instalment paid, this is dealt with by an accrual or a prepayment. Accruals deal with costs underpaid, to be paid later. Prepayments deal with amounts paid in advance (prepaid).

In this exam question, the accounting charge for the first year was £70,000 x 7/12 = £40,833. As a larger instalment than this of £65,000 was paid in the first year, there was an amount prepaid of £65,000 less £40,833 = £24,167 (a prepayment in the balance sheet). (4 April 2011, Q5)

“A significant number of students stated that an asset should appear on the balance sheet of the [operating lessee] company, but this is inappropriate – for an operating lease no asset or liability is recorded at the start of the lease.”FMA Examiner’s Report

For operating lessee accounting, there is no capital asset to be recorded on the balance sheet. So don’t write about operating lease assets.

“Almost all students correctly identified that the lease was a finance lease and most gave an adequate explanation of the accounting treatment – although the fact that the asset should be depreciated over the shorter of the useful life and lease term was often missing.”FMA Examiner’s Report

To score this easy mark, get into the habit of writing: “Finance-leased asset depreciated over shorter of useful life and lease term.”

“The quality of calculations was better for the finance lease. Some, however, used sum-of-digits instead of the stated policy of actuarial.”FMA Examiner’s Report

There are two acceptable methods for spreading the total finance charge in a finance lease. These are the sum-of-digits method; and the actuarial method.

The two previous exams had indeed required using the sum-of-digits method. This resulted in some candidates answering last time’s question (sum-of-digits) instead of this time’s question (actuarial method).

Invest time in reading all the questions carefully to pick up on these important variations.

Download the previous articles from this series and other useful study information from the exam tips area of the ACT student site at study.treasurers.org/examtips

Doug Williamson FCT is an examiner, tutor and exam scrutineer for six ACT exam courses