Gearing and leverage are important factors in determining the riskiness of a company. This applies whether lenders are assessing credit risk or shareholders are weighing up equity risk. Equity carries more risk than debt in a company and equity holders will want to assess their risk. A simple view of the overall risk in any firm could look like this:

Business risk refers to the volatility of earnings or cash flows and financial risk refers to how risky the capital structure is. So, a firm with high financial risk is said to have high leverage or high gearing. In other words, leverage and gearing are measures of financial risk.

A firm with higher risk, from whatever source, should reward investors with a higher return and so shareholders seeking returns can find it either from business risk, from financial risk or from both. Generally, higher financial risk should lead to higher equity returns for a given business risk and the major reason why companies take on debt is to enhance their returns to shareholders.

A technology company might be considered to have high business risk, whereas a utility or a property company may be seen to have low business risk. In fact, companies with a low-risk business model must adopt some financial risk to get equity returns to acceptable levels. Some business models, including private equity, deliberately adopt high financial risk to achieve extraordinary equity returns.

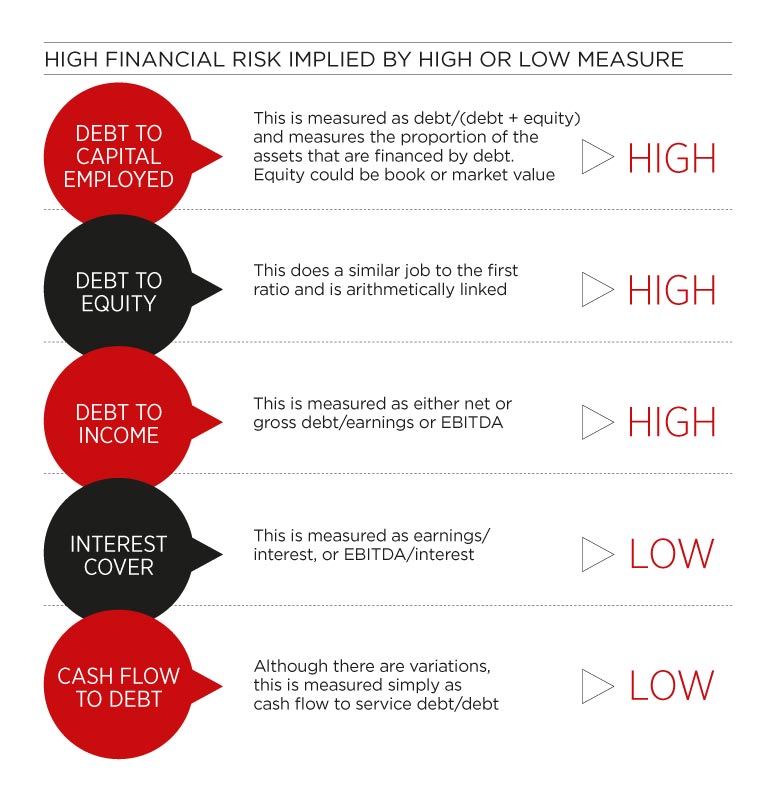

These ratios are the main measures of financial risk, but by no means the only ones. Debt to turnover and return on capital are other examples. Some ratios refer only to the balance sheet, some only to the profit and loss account, and some to both financial statements.

There is no rule that says a particular ratio level indicates above- or below-average risk; it will vary by industry. A very creditworthy property company will have low interest cover and high debt to capital employed. Similar ratios in an industrial company may send lenders running to the hills. Ratios can be used most productively when making comparisons between companies in similar sectors and over time. For any one firm, more than one measure might be required to properly understand the financial risk.

Unsurprisingly, the above measures are heavily used by credit rating agencies, although analysis of business risk is also important to them.

There are several measurements used to assess financial risk and many of these have become the language of the credit markets. Some of the most commonly applied ratios include:

Will Spinney is associate director of education at the ACT.