The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last three months. If you think I’ve missed anything important, do please send an email to technical@treasurers.org.

Regulatory announcements

In November the Chancellor of the Exchequer announced the UK’s National Payments Vision. Its key goals are:

Innovation: Encouraging the development of new payment solutions that meet the evolving needs of users, including advancements in digital and mobile payments.

Inclusivity: Ensuring that everyone, including underserved or vulnerable groups, can access and benefit from secure and affordable payment systems.

Security: Strengthening the resilience and safety of payment systems against fraud, cyberattacks, and other risks.

Collaboration: Fostering cooperation between government, regulators, financial institutions, and tech innovators to create a cohesive and forward-thinking payments ecosystem.

Global Integration: Ensuring the UK’s payment systems are compatible with international standards and can seamlessly handle cross-border transactions.

The vision is focused on creating a payments infrastructure that is future-proof, responsive to changing user needs, and supports the broader economy and includes the following specific goals:

Clarify upgrades to FPS and assess longer-term requirements.

Seamless account-to-account (A2A) payments must be developed to provide greater choice to consumers and merchants including the development of a commercial Variable Recurring Payment model.

For treasurers and businesses, it aims to create a more seamless, efficient, and secure payments ecosystem, by simplifying processes, reducing costs, and enabling more strategic financial management.

The Payment Systems Regulator (PSR) published the Final Report on its Market Review into Cross Border Interchange Fees along with an associated consultation paper which seeks views on potential remedies to the issues identified. The consultation paper ends on 7 February. Key findings from the review included:

A lack of competition: Mastercard and Visa were not subject to effective competitive constraints, allowing them to increase their fees to an unduly high level.

Costly increases: Mastercard and Visa raised their fees without regard to the potential impacts on or interests of businesses and their customers. The PSR found that the increases are costing businesses £150-200 million extra annually.

Unclear rationale: The PSR did not identify any justifications for the increases. Mastercard and Visa were not able to show that they undertook any specific assessment when deciding to increase their fees and the PSR has seen no evidence that the pre-increase fee levels were not working.

The consultation paper identifies a two stage intervention plan:

A short-term, interim cap on fees (and if so, at what level).

A long term cap based on an appropriate methodology.

Interesting reports

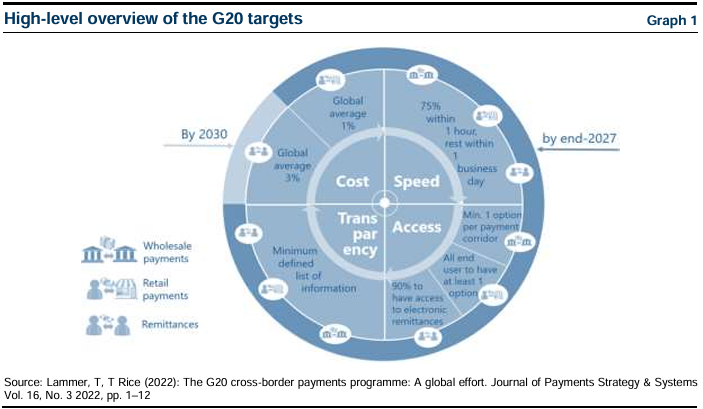

The Financial Stability Board issued its Consolidated progress report for 2024 on the G20 Roadmap for Enhancing Cross-border Payments. Details of the targets are below.

It found that overall at the global level, this year’s KPIs indicate that significant progress will be needed to meet the targets across all market segments. While some regions are close to meeting some of the targets, other regions continued to face greater challenges, particularly in meeting the targets set for cost and speed. It will take time for the actions carried out under the Roadmap to be fully reflected in the KPIs as jurisdictions will need time to implement the agreed policies and industry participants adapt to the relevant changes.

For the wholesale segment it found that:

The overall speed of wholesale cross-border payments decreased marginally due to technical factors. The share of payments over Swift crediting funds within one hour and one business day decreased to 50.6% (-3.2%, compared to 2023) and 92% (-0.7%), respectively.

The Middle East showed the largest improvement for both in-flight and beneficiary-leg processing times, while Africa remained the farthest from the target. Several regions experienced notable improvements in speed, with the largest improvements observed in the Middle East’s in-flight and beneficiary-leg processing times (+1.8% to 87.5% and +5.8% to 35.3% respectively, within one hour). Despite these improvements, the Middle East, Sub Saharan Africa (24.7%), and Asia-Pacific (29.5%) remained the regions with the slowest beneficiary leg.

The European Payments Council 2024 published its “Payment Threats and Fraud Trends Report”. Key findings included:

An overview of the most important threats and other “fraud enablers” in the payments landscape, with focus on recent attacks and outline of the broader attack vector landscape including:

social engineering,

malware,

advanced persistent threats (APTs),

distributed denial of service (DDoS),

botnets,

third-party vendor risks,

monetisation channels,

liability for social engineering fraud.

For each threat or ‘fraud enabler’, an analysis of the impact and context was provided, along with suggested controls and mitigations.

The 2024 update of the report discusses in detail the topic of social engineering, including the liability aspects. Other attention points in the 2024 update of the report are:

How the increasing use of QR-codes has attracted fraudsters

The risks of AI being used for malicious objectives

A scale up of Automated Teller Machine (ATM) skimming and relay fraud has been observed

Capgemini released its World Payments Report 2025. Key findings included:

Asia-Pacific stands out as one of the fastest growing regions for non-cash transactions with a 20% YoY increase in 2024 compared to Europe (16%) and North America (6%). Globally, most industry executives (77%) identify e-commerce growth as the critical driver accelerating the shift to non-cash transactions.

Naresh Aggarwal

23 January 2025