The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last month. If you think I’ve missed anything important, do please send an email to technical@treasurers.org.

Regulatory announcements

- The Payment Systems Regulator (PSR) has announced plans to extend the scope of the Confirmation of Payments programme to an additional 400 payment service providers which will increase coverage from 92% of Faster Payments transactions to 99%. Two distinct groups have been identified and set a deadline of 31 October 2024.

- The PSR’s review of card acquiring services in the UK in 2021 identified that found that the supply of card-acquiring services does not work well for merchants with annual card turnovers of up to £50 million. These merchants could make savings by shopping around or

negotiating with their current supplier, but many do not. In its final decision on remedies, the PSR set the following directions:

-

- Summary boxes containing bespoke key price and non-price information to be sent individually to each business and shown prominently in their online account

- Online Quotation Tool using the information provided in the summary boxes to make comparisons with different providers online

- Trigger messages to prompt businesses to shop around and/or switch

- A maximum duration of 18 months for Point of Sale (POS) terminal lease and rental contracts with a rolling monthly contract thereafter to prevent businesses from being locked into length contracts over several years

- The PSR has launched a series of proposals to put mandatory reimbursement in place for all online and mobile payments and has opened up a consultation that closes on 25 November 2022.

- The Financial Conduct Authority (FCA) introduced several changes to the Regulatory Technical Standards on Strong Customer Authentication and Secure Communication (SCA-RTS) including a new exemption under which customers will not need to reauthenticate when they access their account information through a TPP. Instead, TPPs will be required to obtain explicit consent from customers at least every 90 days. The FCA encouraged ASPSPs to apply the exemption as soon as possible after the changes to the SCA had come into effect on 26 March 2022 with a view to the widespread adoption of the exemption by 30 September 2022.

- Paym – a service in the UK that links bank accounts to mobile phone accounts, announced plans to close by March 2023 citing a “rapid evolution” in payments tech since Paym’s launch in 2014 with payment volumes diminishing over the past three years.

- The PSR issued a consultation to direct around 400 more financial firms to introduce Confirmation of Payee (CoP) protection in two phases:

- The first group will be prioritised based on the complexity and size of the institution and/ or firms where the adoption of CoP could have the biggest impact in preventing APP scams. This first group would see an increase of CoP coverage from 92% of transactions made via Faster Payments to 99%. This group would need to have implemented CoP by 30 June 2023.

- The second group includes all other firms which use either unique sort codes, or that are building societies using a Secondary Reference Data (SRD) reference type. This group would need to have implemented CoP by 30 June 2024.

Around the world

- The launch of Canada's Real-Time Rail (RTR) payments system has been pushed back from the middle of next year to an as yet undetermined date to provide additional time to validate and test the components and end-to-end integration of the RTR system. RTR will allow Canadians to initiate payments and receive irrevocable funds in seconds, 24/7/365. The system will also tap the ISO 20022 messaging standard to support payment information traveling with every payment.

- Tencent's WeChat launched a palm print enabled payment mini programme in Shenzhen which alongside passwords, fingerprints, and facial recognition, allows users to settle payments in an alternative way, with customers now being able to pay for orders with a hand swipe.

- Using SWIFT Go, BNY Mellon recently announced it had successfully facilitated one of the first fully transparent payment transaction between Egypt and China. Delivery of funds to the beneficiary and confirmation to the originating bank were achieved in less than three hours compared with cross-border transactions between Egypt and China which had previously taken over two days.

- The Federal Reserve Banks have specifically targeted a production rollout of the service in the May to July 2022 timeframe and comes as the FedNow Pilot Program prepares to enter technical testing for the service starting in September.

Interesting reports

- UK Finance provided its 2022 Half Year Fraud Update showing that:

- criminals stole a total of £609.8m through authorised and unauthorised fraud and scams, a decrease of just under 13 per cent compared to H1 2021. The advanced security systems used by banks also prevented just under £584m from being stolen.

- During the first half of 2022 criminals have continued to focus activity mainly on socially engineering their victims, usually with the intention of tricking them into authorising a payment to an account within their control (known as Authorised Push Payment (APP) Fraud)

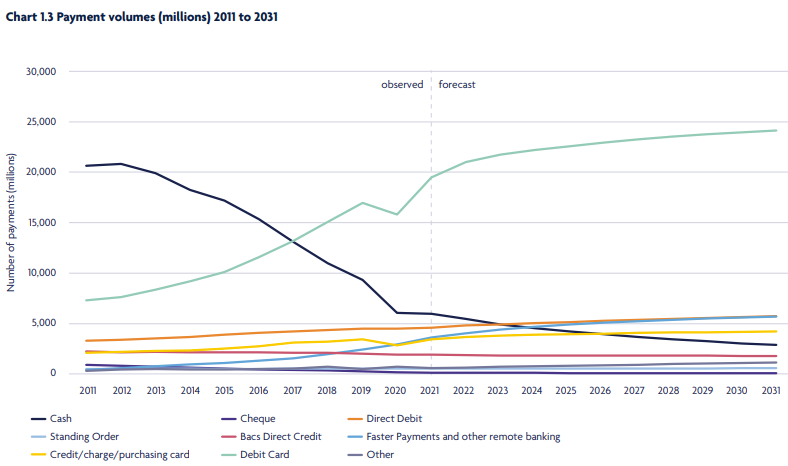

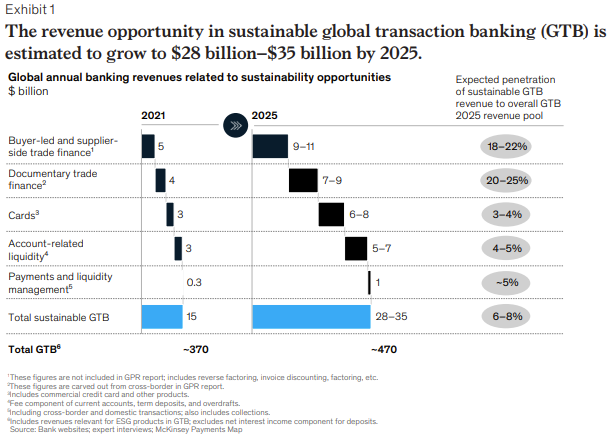

- McKinsey has released its annual Global Payments Report. The reports cover a range of challenges and opportunities and includes the following:

- Capgemini has released its World Payments Report 2022. It includes a number of useful messages and infographics including:

- An increasingly mature digital payments infrastructure has fuelled non-cash transaction growth

- Regulatory and industry initiatives have been numerous and far-reaching during the current period

- SMBs’ expectations of their banks and other payment service providers are rising

- Payments services provider executives admit that SMBs face unresolved process and technology issues

- Composable architecture enables payment firms to configure services, capabilities, and features on the go

- Central banks are collaborating to explore DLT use cases with other financial service provider