Avatars. Central bank digital currencies. Invoice tokenisation. Machine-learning algorithms. Metaverses. Natural language processing. Underwater data centres. Quantum computers. Corporate treasurers have eyes on a wide range of technology with potential to reshape their future treasury infrastructure, but they are particularly interested in innovations and trends that could help them address issues and overcome the challenges they face today.

“There are still gaps where treasury and technology could come together to more effectively solve problems,” says Royston Da Costa, assistant group treasurer at Ferguson plc, a North American plumbing and heating products distributor. Treasury dealings with banks can offer some prime examples: “Payments, bank feeds, cash pooling and trade finance are just a handful of the areas where, in my view, we still haven’t got tech-savvy solutions,” he says.

If banks improve their systems and processes, other vendors will be less limited in what they can do to help treasurers address pain points, he suggests. “There are good software vendors working with what they have, but sometimes it’s about putting lipstick on a pig,” says Da Costa. “I still have to pinch myself about payments. It’s 2022 and we still struggle with value dating and with beneficiary confirmation of receipt.”

This also applies to know your client (KYC) procedures.

For Robert Scriven, treasury and financing director at Capricorn Energy, a UK-based oil and gas exploration and production company, procedures around KYC and anti-bribery/corruption are the areas where more tech-savvy solutions would be most welcome. “It seems there is no progress here and it’s a massive headache for everybody,” says Scriven. There are various repositories that aim to take some pain from KYC processes, but at the moment, he says, they don’t really solve the problem.

Global standardisation of KYC procedures across all financial institutions would do the trick, but is unlikely – and not the only option. “We need adoption of a standard way of verifying and transmitting documents electronically, and one organisation to step up,” says Scriven, with SWIFT in his sights.

“It has the widest set of relationships,” he says. SWIFT already has a global platform for sharing KYC data, used by 6,000 financial institutions, and could steer the sector towards a common standard for document verification and delivery.

Treasurers are increasingly aware of how much potential there is to address their pain points by leveraging technology. “It’s helped us to eliminate low value and inefficient processes that we had to run manually in the past,” says Da Costa. “It’s also allowed us to focus more on value-added processes, advising the business and getting more involved on the commercial side.” It can liberate time for and improve the quality of analysis and strategy planning, and enrich this with a better understanding of risks and the data underlying decision-making, he adds.

This can be seen in the application of machine learning (ML) to cash management. “We started implementing ML capabilities in cash-flow forecasting because the benefits are significant,” says Philipp Leitner, co-CTO and MD at ION Treasury, provider of cloud and on-premise treasury management systems (TMSs). With ML algorithms, he says, cash forecasts can be generated 3,000 times faster than manually, while neural networks can make cash forecasts more accurate by as much as 10%.

“Better predictions can free up money,” says Leitner, adding that ION Treasury was the first TMS provider with a cash-flow forecasting solution using ML with a neural network – and he’s keen to sing its praises. “Increasing cash forecast accuracy by 10% on a $75m average cash balance that’s invested at 2% leads to a $150,000 gain per year.” Recent ION Treasury innovations using ML involve transaction tagging, reconciliation and anomaly detection for payments.

More will become possible in the future, as ML capabilities are increasingly applied in treasury, because of their strengths in data analysis, finding patterns and solving difficult mathematical problems. “A TMS powered by ML can suggest alternatives for trading, hedging or optimising the capital structure. ML algorithms can find outliers and alarm the user in areas such as anti-fraud, sanction screening, security and operations,” says Leitner.

There are good software vendors working with what they have, but sometimes it’s about putting lipstick on a pig

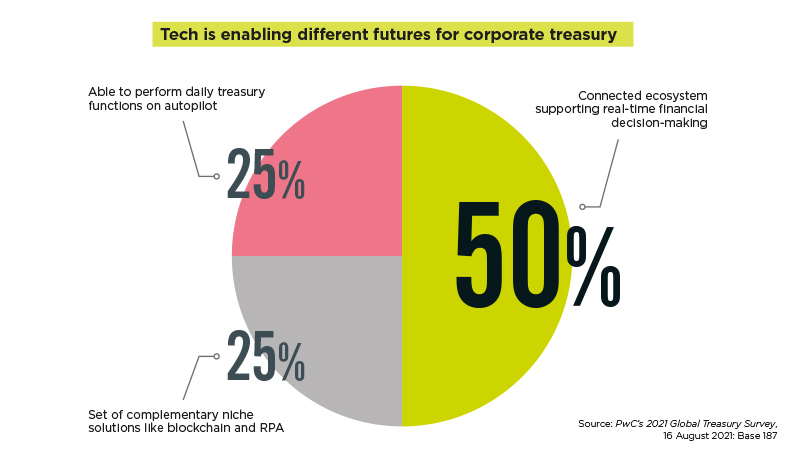

Recent research by PwC finds data analytics and visualisation tools embedded across corporate treasury, aided by ML and other artificial intelligence techniques, along with other tech-enabled developments such as application programming interfaces (APIs), blockchain and robotics process automation (RPA). “Tech is increasingly important for treasury, and a treasurer will not last long in their role if they are not seen embracing it,” says Sanjay Bibekar, director, treasury advisory, PwC.

Automation is spreading and getting smarter, and building on tech such as ML and RPA to power trends such as hyperautomation. “Organisations are transitioning from a loosely coupled set of automation technologies to a more connected automation strategy,” says Gartner analyst Cathy Tornbohm, and new tools are emerging to support this. Treasurers may want to stay close to IT and monitor automation plans that may impact on their corporate enterprise resource planning (ERP) system or TMS.

APIs and the integration they can facilitate are another enabler on the journey from automation to hyperautomation. The API has already done wonders for connectivity – by allowing separate software applications (such as ERP and TMS) and services (such as those provided by banks) to talk to each other and share data more quickly, easily and economically than would otherwise be possible – and they’re being used to offer corporate treasurers a number of benefits.

“We are investing a lot in APIs,” says Jean-Baptiste Gaudemet, senior vice president of data and analytics at Kyriba, a web-based cash and treasury management solutions provider. Its enterprise liquidity platform unifies treasury, risk management, payments and working capital. They’re connected in quasi real time by APIs originating from and providing access to data from banks, ERPs and various other software and services outside Kyriba, which manages the APIs on behalf of its customers.

Some TMSs, ERPs and other systems now sit within an ecosystem of interconnected API-enabled ‘plug-and-play’ software applications that can extend each other’s functionality, although the benefits aren’t always easy to access for treasurers with complex global infrastructures. “APIs allow us to open up the application,” says Gaudemet. Kyriba, for example, has created a development portal with a portfolio of APIs openly available to support and enable systems connection.

“Anyone can engage with us through the APIs,” continues Gaudemet. The APIs are catalogued, documented and supported by explanatory videos. “Even without talking to us, anyone can consume those APIs and create an integration with Kyriba, so the potential is massive.” This approach can be powerful from a business model perspective, for innovation and for users such as corporate treasurers, because it can help to keep a system that you have invested in at the cutting edge.

“Whatever the size of Kyriba, we simply can’t do everything internally. When it comes to innovation, we will always need to look outside of our organisation for new smart and creative solutions we can then integrate with APIs,” says Gaudemet – although it is also true for any software developer or service provider. The open availability of the APIs and the critical mass of its customer base both help Kyriba to attract and unlock the potential of other, often more specialised fintechs that can complement Kyriba.

Examples range from Sis ID (a collaborative platform for securing payments) to Copper (a secure gateway to investment in digital assets). “Our job is to facilitate access to such innovative solutions. We’re not crypto-technology experts and we’re not a custodian,” says Gaudemet. But Copper does have an app for that. So, treasurers can use Copper to invest in cryptocurrency, integrate this into their Kyriba cash management, and consolidate the liquidity balance across fiat currencies, cryptocurrencies and money market funds.

How many will do this remains to be seen.

Cryptoassets can seem like a mixed blessing for treasurers, but so can other tech with potential to address their pain points. Take APIs and in particular, bank APIs.

Da Costa says: “Over the past few years all I’ve heard is APIs, APIs, APIs. But we’ve got SWIFT and we’re happy with our MT940s.” So, setting up individual APIs for myriad banks and software vendors has not seemed particularly appealing. But Da Costa recently saw a development in this area that does impress him: FinLync, an API aggregation tool that can do the heavy lifting.

“Many teams are dealing with issues that come from having multiple bank relationships which, compounded by various TMSs, can cause a snowball effect,” says Tahreem Kampton, ex-Microsoft corporate treasurer, and FinLync’s adviser. This situation can leave treasury and departments including IT and payroll with a complex patchwork of connectivity. This API issue may be much easier to overcome for corporates and for service providers such as banks.

Kerstin Montiegel, global head, client connectivity, at Deutsche Bank, says: “Integration with FinLync makes it much easier for corporates to adopt our banking APIs and shortcut the road to automated real-time treasury.” With FinLync’s quick and easy plug-and-play access to any ERP or TMS, more treasurers may be able to access benefits such as real-time payment tracking and liquidity management, and faster, more informed decision-making.

Clearly, it’s not all sunshine and roses as treasurers embrace digital technologies as a basis for data networking, connecting systems such as ERP and TMS to the cloud, digitalisation of payment transactions, everything as a service and other routes to efficiency and effectiveness. “This creates new threats and vulnerabilities, along with a growing need for appropriate security measures,” says Nils Bothe, partner, finance and treasury management, corporate treasury advisory, at KPMG, Germany.

Cybercrime is now highly organised and focused. So, with changing working practices and myriad gateways, points of attack and areas of vulnerability for treasurers to be mindful of, where should the focus be? Tech is part of the solution but, says Bothe: “Apart from an up-to-date IT security structure, the first and most important step in protecting against cybercrime is to educate and raise awareness among employees. Only those who know the tactics of fraudsters can protect themselves against cybercrime.”

As we move from the new normal to the next normal, treasurers are likely to see more automation and more emerging technologies as part of their day-to-day working lives. But whatever technology you are exploring or thinking of exploiting in and around the treasury function, today or tomorrow, you’ll need to consider both the potential benefits and the downsides, and ensure that all members of the treasury team – and others in the business – also appreciate them.

Treasurers are interested in the possibilities offered by digital assets, but that doesn’t mean they are rushing to embrace cryptocurrency. Michael Aandahl, head of treasury digitalisation at IKEA, says there are three important aspects for treasurers to consider:

There are other matters to consider, too, in areas such as brand management. “There’s still a perception of crypto as a black-market currency, and some environmental, social and governance issues to consider,” says Aandahl, as cryptocurrency processes are very energy-consuming. Similar concerns are shared by Da Costa: “We are interested, but don’t want to break new ground. We will be comfortable as close followers of cryptocurrency.”

Decisions on cryptocurrency will, both say, be driven by business needs, and early adopters tend to be in sectors such as tech, where cryptocurrency isn’t far from the core business. Da Costa sees initiatives such as JPMorgan’s cryptocurrency (JPM Coin) and the prospect of central bank digital currencies (CBDCs) as possibly enabling wider crypto uptake, particularly for cross-border payments. Although impetus from at least one big ‘fiat’ CBDC may be needed.

Meanwhile, blockchain technology that enables cryptocurrencies (such as Bitcoin) is already being used to support other initiatives that can benefit treasurers, such as enabling execution of smart contracts. The underlying technology may also address some liquidity issues by helping to free up non-liquid assets such as unpaid invoices. Marco Polo network, for example, tokenises payment obligations and invoices, which can make invoice financing faster and easier while reducing costs, risks and delays in trade finance.

Lesley Meall is a freelance journalist specialising in the technology sector

This article was taken from Issue 3, 2022 of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership