The development of CBDCs across the globe continues with Nigeria’s recently launched e-Naira becoming the 9th country to begin a national rollout. More countries have made commitments including India, and the Philippines and Jamaica has offered 2,500 Jamaican dollars (US$16) to the first 100,000 Jamaican citizens to use the country’s new CBDC - Jam-Dex. In Australia one of the First Nations - Sovereign Yidindji Government (SYG) territory saw the first transaction of its own CBDC.

It is becoming increasingly difficult to keep up with all of the announcements from a raft of central banks and think tanks but here are some that caught my attention:

- The minutes of the February meeting of the Bank of England’s CBDC Engagement Forum were released. The Bank presented on CBDC ‘use cases’ and suggested a ‘use case’ would be important for all elements of the CBDC ecosystem – UK authorities, private sector intermediaries, and end users – but would likely differ for each. The Bank presented the discussion around whether CBDCs should be designed with one or more primary use cases in mind or be as adaptable a platform as possible with use cases development left to the private sector.

- US President Biden issued an executive order covering the Responsible Development of Digital Assets. The Order calls for a full-scale assessment of the potential benefits and risks of a CBDC, both for consumers and investors as well as the broader U.S. financial system. Biden has ordered the Treasury Department to spearhead the research and report, with input from other federal agencies, including the Secretary of Commerce and the Secretary of Homeland Security. The assessment is also supposed to determine whether the implementation of a CBDC would be in “the national interest.”

Several organisations are already researching and piloting CBDCs in the United States, including the Boston Fed, which has partnered with Massachusetts Institute of Technology (MIT) on CBDC technology, and the Digital Dollar Project. The Digital Dollar Project has promised five pilot projects, which are planned to kick off in the coming months, to evaluate whether and how a U.S. CBDC would benefit people who are unbanked (or underbanked) – a key point stressed in Biden’s executive order.

- The IMF issued a FinTech Note - Behind the Scenes of Central Bank Digital Currency that looks at the insights, lessons, and open questions arising from 6 advanced CBDC projects – The Bahamas, China, Uruguay, Canada, Sweden and Eastern Caribbean. Its findings include:

- Open issues including the nature of sustainable business models that will ensure cost recovery and provide sufficient incentives for private sector participation

- Innovation to allow for important features such as off-line capacity

- Key technology difficulties including making choices in a very new and rapidly evolving field, as well as costs associated with the development process

- The choice between centralised and distributed technology does not need to be either-or.

While individual country contexts remain important, there are also areas of convergence. All central banks:

- have explored the intermediated operational model. Countries are seeking a balance between preserving key aspects of the traditional monetary and financial system while at the same time updating the role of central banks in the digital era

- with CBDCs currently in circulation have design characteristics that limit competition with bank deposits

There are policy trade-offs and leveraging policy synergies could be a potential area of increased central bank attention in the future. There are policy synergies between anonymity, risk reduction, and financial inclusion and trade-offs such as the relationship between anonymity and illicit use of money.

- A new study from Deloitte - State-Sponsored Cryptocurrency, highlighted the potential of Bitcoin (BTC) as a base to create a cheaper, faster and more secure ecosystem for CBDC. The report pointed out five key areas where Bitcoin can help traditional fiat currency improve drastically — speed, security, efficiency, cross-border payments and collaboration with other payment participants.

The analysis suggests that governments that are first to roll out a nationwide CBDC will have an advantage in influencing the use of their local currency in international markets and trades. In a CBDC environment, Deloitte envisions crypto exchanges retaining their current position as a facilitator that will be used to convert “users’ cryptocurrency to paper currency when transacting across different currencies, and charges an exchange fee in return.” In such a scenario, banks will act as custodians of the distributed ledger who will compete with other miners to process transactions and collect the reward. The report concludes that while CBDCs will not serve as a one-to-one replacement for BTC and other cryptocurrencies, the mainstreaming of CBDCs will open up an additional option for users to choose the most appropriate medium of payment.

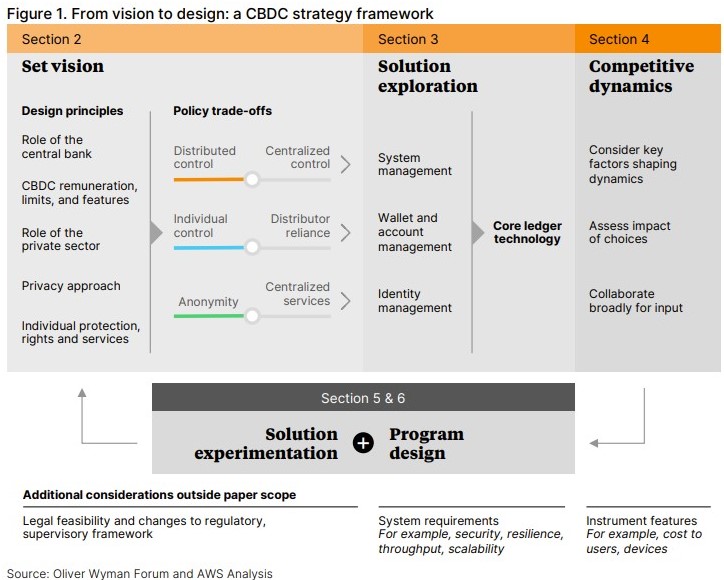

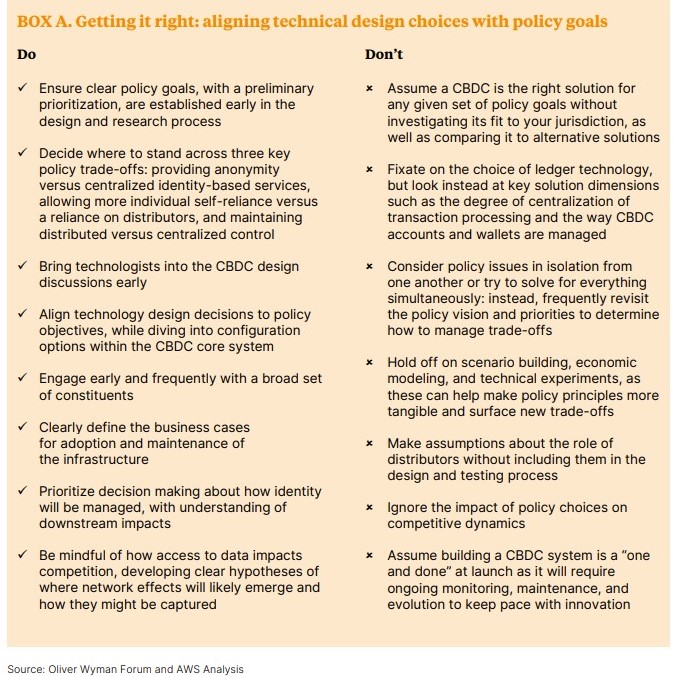

- The Oliver Wyman Forum and Amazon Web Services (AWS) have released a report - Retail Central Bank Digital Currency: From Vision to Design that looks at the relationship between policy objectives, technology design choices and competitive dynamics. This is critical for evaluating and determining whether to launch a CBDC and also for developing a tailored design. It includes the following:

- The Global Financial Markets Association commissioned a report from Boston Consulting Group and Clifford Chance LLP on key considerations for CBDCs in wholesale markets (wCBDCs). Its findings include:

- Central banks in collaboration with the private sector should continue to explore the role that wCBDCs can play in driving innovation and efficiencies in wholesale markets.

- Central banks should take a measured approach in the introduction of wCBDCs and the timeline should be cautious to mitigate any potential transition risk impacting safety and soundness, and financial stability.

- wCBDCs are expected to operate alongside legacy instruments and systems, and not to replace them. It is therefore important for wCBDCs to be interoperable with the broader financial market ecosystem.

- The use of sandboxes, proof of concept, dialogue with market participants, and pilot programs based on specific use cases will test the application of wCBDCs and help identify the impact on capital markets.