Update on the Payments landscape – Sept 2021

The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last month. If you think I’ve missed anything important, do please send an email to technical@treasurers.org.

Central Bank Digital Currencies (CBDCs) and other digital currencies

It is becoming increasingly difficult to keep up with all of the announcements from a raft of central banks and think tanks but here are some that caught my attention:

- The number of pilot schemes looking into cross-border is increasing.

- A couple of months back the BIS Innovation Hub, the Bank of France and the Swiss National Bank announced that, together with a private sector consortium led by Accenture, they would conduct an experiment using wCBDC for cross-border settlement known as Project Jura.

- Back in February, China and the UAE joined the m-CBDC Bridge project run in partnership with the BIS Innovation Hub, the Hong Kong Monetary Authority and the Bank of Thailand.

- This month Project Dunbar was launched by the BIS Innovation Hub and central banks of Australia, Malaysia, Singapore and South Africa to test CBDCs for international settlements.

- In the UK, Project Fire has recently been launched. This will explore the use of hardware devices that allow consumers to hold central bank digital currencies (CBDC). Other participants in the project include the Bank of England, British Standards Institution (BSI), University College London (UCL), and the University of Edinburgh.

- In a recent blog post, the Head of Future Technologies at the Bank of England, William Lovell, shared his views on the progress of UK CBDC research. In it he envisages a digital future where different apps based on a CBDC can deal with the various use cases that cash currently addresses.

- In a recent speech the President of the ECB said that the central bank is launching a two-year investigation into a digital euro as more consumers switch from banknotes and cash. The actual release of the ECB-backed cryptocurrency in the bloc’s 19 members could take another two years on top of the technology design and investigation stage (itself expected to take a couple of years). In theory, if all goes to plan, the central bank could launch a digital currency by 2025 if European regulators give the project the green light.

- She noted that the project would complement the existing banking system rather than trying to ‘jeopardise’ it adding that experiments to consider the merits of minting a ‘digital euro’ were going through a complex decision-making process. The bank has not yet decided to issue a CBDC.

- From 7 September 2021 bitcoin will become legal tender in El Salvador despite warnings from the IMF and the World Bank citing the potential impact on macroeconomic stability and bitcoin’s environmental costs.

- In a recent speech to the Aspen Security Forum, the new chair of the U.S. Securities and Exchange Commission Gary Gensler set out his latest views on the shape of digital currency regulation in the country.

- The Bank of Thailand (BOT) announced plans to begin testing a Retail Central Bank Digital Currency (Retail CBDC) in the second quarter of 2022 following a study on the implications of a retail CBDC on the country’s financial sector as well as published results of a survey on the development of a CBDC based on the paper ‘The Way Forward for Retail Central Bank Digital Currency in Thailand’, published in April 2021.

- Trials will begin with testing and evaluating the usage of CBDC in conducting cash like activities within a limited scale, such as accepting, converting, or paying for goods and services. The central bank will then move on to test and evaluate the ways in which CBDC can be further developed for innovative use cases, by allowing for participation from the private sector and technology developers.

Interesting reports

The Arab Monetary Fund has issued a policy guide which sets out a very helpful introduction to the world of Distributed ledger technology (DLT) and blockchain as well as a road map and guidance for its adoption in the financial sector.

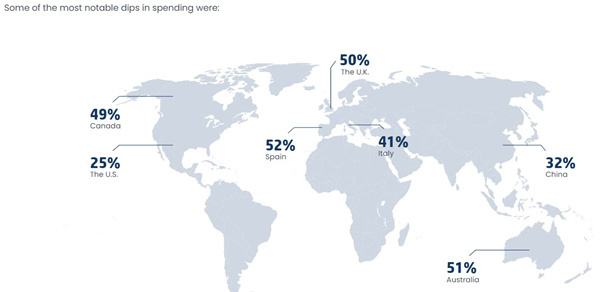

A recent report by UpgradedPoints on a cashless society showed how COVID-19 had affected the use of cash across a number of different countries and includes the picture below:

A recent report from PwC – navigating the payments matrix looks at a number of emerging trends and the impact on the payments market. It includes the following infographic.

A recent report from Ravelin looking at global payment regulation and authentication had this analysis:

The Paypers has released its latest Payment Methods Report which looks at recent payment trends with a number of different guest contributors. It looks at number of developments including how Account-to-Account (A2A) payments, Buy Now Pay Later, mobile payments, and payment cards have been developed to meet acceptance and adoption in the payments ecosystem.

UK payments landscape

- The Payment Systems Regulator (PSR) launched a consultation on lowering risks to the delivery of the New Payments Architecture (NPA). Most respondents agreed with an earlier consultation that Pay.UK should phase the development of the NPA by narrowing the scope of the NPA central infrastructure services (CIS) contract and secure this contract through a competitive tender. As a result, the PSR will mandate that Pay.UK:

- must, as a minimum, buy services needed to support single-push payments (which will allow most Faster Payments transactions to migrate to the NPA); and

- may buy additional services and system functionality only if the PSR does not object

Global payments landscape

- SWIFT announced recently the launch of its Payment Pre-validation service. This will prevent incorrect or missing information about the beneficiary when the payment is initiated - a main cause of payments being returned to remitter, incurring additional charges or taking too long to get to the beneficiary. It allows a sending bank to confirm account details, via an API, with the receiving bank from the very beginning of the process so that any data or account problems can be identified and corrected before the payment is sent.

- Payments Canada has launched Lynx, the country's new high-value payment system to process large value, time-critical payments with real-time settlement finality and which it says will provide enhanced cyber security and resiliency capabilities. A second release scheduled for late 2022 will introduce the ISO 20022 message standard, which will bring new products and services, and the digitisation of manual and paper-based processes related to invoicing and payment reconciliation. Lynx is one part of Payments Canada’s multi-year, multi-system payments modernisation initiative, that also includes a real-time payments system that is currently being built.

- The BIS’s Committee on Payments and Market Infrastructures published its work programme for 2021-22 for the first time. The plan outlines the strategic priorities for its monitoring and analysis, policy, and standard-setting and implementation activities, under its two overarching themes:

- Shaping the future of payments by enhancing cross-border payments and addressing policy issues arising from digital innovations in payments (such as central bank digital currencies and stablecoins), while monitoring changing trends in payments

- Evaluating and addressing risks in financial market infrastructures by working on issues related to central clearing and others that emerged or were accentuated over the course of the Covid-19 pandemic.

Naresh Aggarwal