The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last month. If you think I’ve missed anything important, do please send an email to technical@treasurers.com.

Central Bank Digital Currencies (CBDCs) and other digital currencies

It is becoming increasingly difficult to keep up with all of the announcements from a raft of central banks and think tanks but here are some that caught my attention:

- The BIS Innovation Hub, the Bank of France and the Swiss National Bank announced that, together with a private sector consortium led by Accenture, they will conduct an experiment using wCBDC for cross-border settlement. The private sector consortium includes Credit Suisse, Natixis, R3, SIX Digital Exchange and UBS. Known as Project Jura, the experiment will explore cross-border settlement with two wCBDCs and a French digital financial instrument on a distributed ledger technology (DLT) platform. It will involve the exchange of the financial instrument against a euro wCBDC through a delivery versus payment (DvP) settlement mechanism and the exchange of a euro wCBDC against a Swiss franc wCBDC through a payment versus payment (PvP) settlement mechanism. These transactions will be settled between banks domiciled in France and in Switzerland, respectively.

- The Basel Committee has issued a consultation on the prudential treatment of banks' cryptoasset exposures. The Committee is proposing to divide cryptoassets into one of two groups. The first group, which would include stablecoins and tokenised versions of existing assets, would be eligible for treatment under the existing Basel framework. The second group would include all other cryptoassets and would be subject to a new conservative prudential treatment. Responses are due by 10 September 2021.

- El Salvador has passed a bill designed to recognise Bitcoin as legal tender ('Ley Bitcoin'). Once signed by the President, the legislation will enter into force immediately. Businesses will have 90 days to set up the required infrastructure, after which they must accept Bitcoin for payments. The International Monetary Fund (IMF) plans to meet with the President to discuss the 'macroeconomic, financial and legal issues' posed by the new legislation.

- The Bank of England issued a discussion paper on digital money, including CBDCs and stablecoins seeking feedback on the impact that moving towards digital money would have on the economy and public policy considerations, including issues around access to cash, financial inclusion, data protection and competition. Responses are due by 7 September 2021.

- Federal Reserve Bank of Richmond issued an economic briefing on the significance of Diem and Alipay to central banks and their currencies.

- The People's Bank of China announced it will launch another public lottery of the digital yuan, distributing 40 million digital yuan to Beijing residents as part of a pilot programme to test and promote the CBDC.

Interesting reports

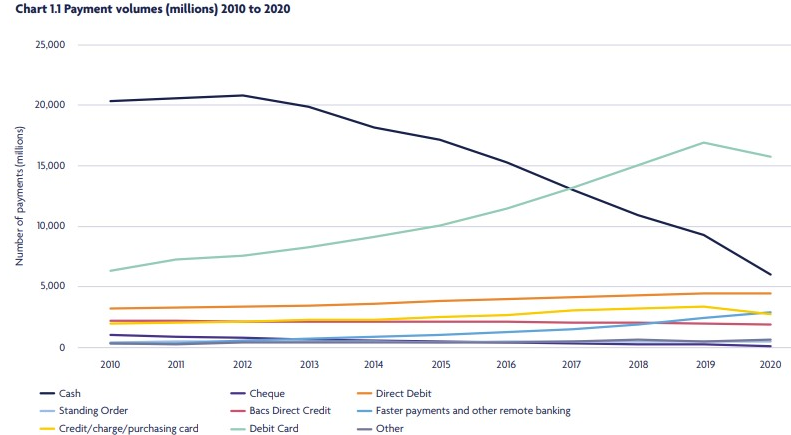

According to the recent UK Finance’s 2021 Payment Markets Report, the total number of payments in the UK declined for the first time in six years, falling by 11 per cent to 35.6 billion with contactless payments now account for more than a quarter of all payments in the UK. There was significant growth however in contactless payments, mobile payments and internet banking, alongside a continued reduction in cash usage. It includes the following chart:

The European Central Bank published its 20th annual review of the international role of the euro. Key findings include:

- The euro’s share in outstanding international loans, in the stock of international debt securities and as an invoicing currency for extra-euro area imports of goods remained broadly stable.

- The share of the euro in global foreign exchange reserves declined, as did the share of the euro in foreign currency-denominated debt issuance and in outstanding international deposits.

- The euro remained a key currency in international green bond markets, a small but rapidly growing segment of international debt security markets.

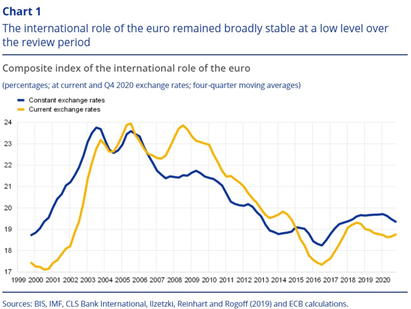

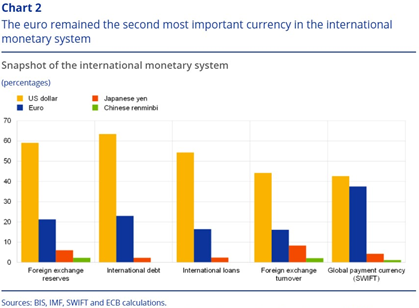

- A composite index of the euro’s international role remained broadly stable over the review period at a low level (Chart 1) with the share of the euro across various indicators of international currency use close to historical lows, averaging around 19%. The euro remained unchallenged as the second most important currency in the international monetary system (Chart 2).

-

- The share of the euro as an invoicing or settlement currency for extra-euro area trade decreased slightly in 2020 for most transactions in goods and services. Over the medium term, the share of the euro as an invoicing or settlement currency for extra-euro area trade has remained stable and close to the levels observed a decade ago. The European Commission continues to support the use of the euro in international trade, through initiatives including the development of euro-denominated instruments and benchmarks, and to foster its status as an international reference currency in the energy and commodities sectors. The euro is used as vehicle currency not only in Europe but also in parts of Africa, suggesting that the euro plays a dominant role in some regions, even if the US dollar is the dominant currency globally.

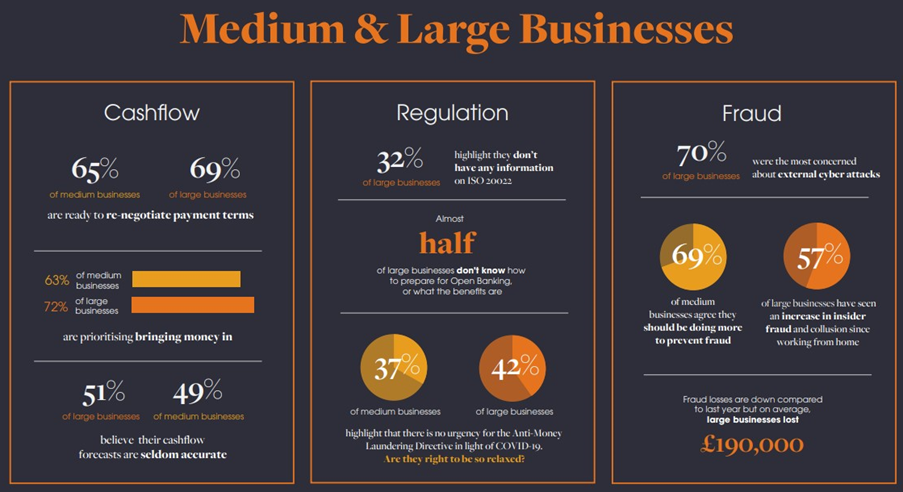

- Bottomline released its 2021 Business Payments Barometer. Some of its findings include:

- 68% of businesses say receiving money quickly has never been more important

- 1 in 4 still using excel to monitor their financial position

- Around half of the businesses surveyed saw an increase in insider fraud and collusion, driven mostly by the large (57%) and enterprise (53%) sized businesses

- 20% of small companies are unaware of any of the upcoming payment initiatives

UK payments landscape

- The UK’s Payment Systems Regulator published a Call for Views on Confirmation of Payee Phase 2. The request also included analysis of Phase 1 which found that CoP has prevented what would otherwise have been a larger increase in APP fraud scams. The PSR had anecdotal evidence of CoP having had a positive impact, notably by resulting in customers abandoning potentially fraudulent transactions. Additionally, it found that there had been a reduction in the relevant types of APP scams sent to CoP-enabled PSPs, while APP scams sent to PSPs not participating in the service had increased. This suggests CoP has improved transaction security for PSPs offering the service.

- The PSR published its 5-year strategy plan focused around:

- Priority 1: Ensure users have continued access to the payment services they rely upon and support effective choice of alternative payment options

- Priority 2: Ensure users are sufficiently protected when using the UK's payment systems, now and in the future

- Priority 3: Promote competition in markets and protect users where that competition is not sufficient, including a) between payment systems within the UK and b) in the markets supported by them

- Priority 4: Ensure the renewal and future governance of the UK's interbank payment systems supports innovation and competition in payments

- The PSR had earlier asked for views on the scope of the initial contract for delivery of NPA central infrastructure services and on the appropriate way to secure this contract. Following an initial submission, Pay.UK (the scheme operator responsible for delivering the NPA) carried out further analysis on the approach to the procurement of NPA central infrastructure services. It subsequently sent a second submission outlining its position on this matter. The key messages are:

- In its August 2020 application to the PSR, Pay.UK argued for a direct award for the procurement of the NPA central infrastructure. This was primarily on the grounds of minimising overall programme risk, but also as it could be quicker than continuing with the competitive award approach.

- In light of changes since making that application, and in particular the narrower initial procurement scope proposed in the PSR’s consultation document, Pay.UK concluded that the optimal approach is to restart the existing competitive procurement process.

Global payments landscape

- Visa has joined forces with Goldman Sachs Transaction Banking to deliver seamless payments solutions and improved treasury operations for corporate clients. Through Visa B2B Connect and Visa Direct Payouts solutions, Goldman Sachs can now offer an efficient and cost-effective payment channel. The solutions will be particularly effective for cross-border business to business and business to consumer payments for high and low value payments offering real-time visibility of payments. High-value flows will leverage Visa B2B Connect, an account-to-account (A2A) cross-border payments network now available in 97 markets whilst low-value payments will leverage the cross-border capabilities of Visa Direct Payouts, offering push payments to consumer and small- to medium-sized enterprise (SME) accounts.

Naresh Aggarwal