The long effort to transition away from LIBOR that began following the 2008 financial crisis seems to be nearing its end. A timetable has now been set by the regulators in the UK and the US running to mid-year 2023.

With a nod to former US Secretary of Defense Donald Rumsfeld, in this effort, we have some things that we know, the knowns, and some that we have identified as not yet knowing, the known unknowns.

What are these, and how will corporate treasurers resolve them in the time allowed?

When Andrew Bailey was chief executive of the Financial Conduct Authority (FCA), he famously sent up a red flare to the markets in July 2017.

That was when he warned that the FCA had obtained a voluntary undertaking from the LIBOR panel banks to continue submitting their quotations until year-end 2021 – but that those relying on LIBOR should plan on that as the end date.

If we fast-forward to March 2021, the FCA announced that while certain USD LIBOR rates, such as the one-week and two-month quotations, would cease as of year-end 2021, other maturities very commonly used in financial instruments and contracts, including those for one, three and six months, would continue to be quoted until 30 June 2023.

That would allow some additional time for USD instruments and contracts to be amended to provide alternate references to the secured overnight financing rate (SOFR).

Consider the known unknowns from just this decision:

These known unknowns will have to be settled soon. But US treasurers complain that their banks are not yet engaging with them on the details of the transition away from LIBOR.

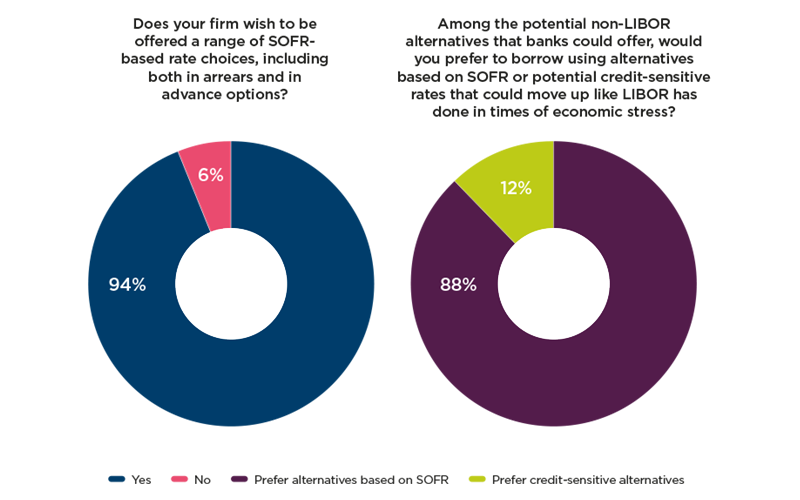

In the Non-financial Corporates Working Group of the Alternative Reference Rates Committee, fully two-thirds of those responding to a recent survey report that they have been unable to receive detailed proposals or timelines for implementation from their bankers.

These graphs illustrate the gap in communications and readiness:

For many corporate treasury departments, another set of known unknowns is made up of all those commercial contracts negotiated by other departments such as sales, procurement and engineering that may have references to LIBOR of which the corporate treasury is unaware.

In most companies, even this long into the LIBOR transition process, there have been no meaningful estimates of the commercial exposure NFCs manage as a result of business contracts they enter into as part of their day-to-day operations.

Consider these examples, which could apply to contracts in any IBOR currency and not just US dollars:

Example 1: worldwide supply agreement

Example 2: long-term construction agreement

With all these known unknowns, the way forward for the corporate treasurer is to identify all the many as yet unknowns in LIBOR transition and drive as quickly as possible to resolve them.

The best practice we see is for the treasurer to bring together a cross-functional team with representatives from those departments who manage these commercial relationships and to identify the contracts with LIBOR references, to work out a replacement strategy, to make the customers or suppliers know of the urgency, and finally to get their agreement on how to amend the contracts in time.

In parallel with this, we have to engage with the banks on the conventions of loans after LIBOR and to adapt systems to these new mechanics.

Learn more about the known unknowns of USD LIBOR transition from this National Association of Corporate Treasurers (NACT) webinar, hosted by the Association of Corporate Treasurers

Tom Deas is chairman of the National Association of Corporate Treasurers, the US national treasurers' association. From 2001 to 2016, he served as vice president and treasurer of FMC Corporation. Prior to that he was vice president, treasurer and CFO of Applied Tech Products Corp, of Airgas Inc and of Maritrans Inc. He has served as a member of the Financial Stability Board’s Market Participants Group and is a current representative to the Federal Reserve’s Alternative Reference Rates Committee.

Further ACT resources on the LIBOR transition can be found here: treasurers.org/hub/technical/libor.