As defined benefit schemes mature, trustees are increasingly turning their attention to the endgame and how their scheme will service its liabilities over the long term. In many cases, this involves targeting a particular funding level sometime in the future through a combination of asset returns and deficit-repair contributions.

In order to maximise the certainty of reaching their target funding level, schemes must do three things well:

In relation to the first of these points, many schemes will already have in place liability-driven investment (LDI) strategies that mitigate their liability-related interest rate and inflation risks. However, few schemes will have in place any protection against the longevity risk inherent in their liabilities. As a result, many schemes are exposed to the impact of changes in life expectancy during the period before reaching their endgame.

One approach for schemes looking to hedge themselves against the potential impact of longevity risk, while retaining control over all of their assets, is to implement an unfunded longevity hedge (commonly referred to as a longevity swap).

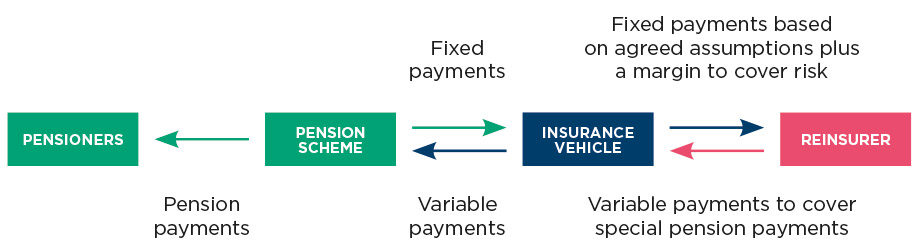

An unfunded longevity hedge transfers the risk of pension scheme members living longer than expected from the pension scheme to an insurer. Figure 1 provides an overview of how an unfunded longevity hedge works.

Figure 1: Overview of an unfunded longevity hedge

For illustrative purposes only

Although the concept of an unfunded longevity hedge is similar to an inflation swap, in that it exchanges fixed for floating payments, in practice their implementation and ongoing management are very different. For example, the payments under an unfunded longevity hedge are linked to the actual survival of a group of scheme members, rather than a quoted index.

For any scheme considering an unfunded longevity hedge, an important question to ask is how might this affect my future plans? In particular, many schemes are targeting buyout as their endgame, in which case there will inevitably come a time at which they wish to buy out the members covered by the unfunded longevity hedge.

In this scenario, the two primary options are to either terminate or novate the unfunded longevity hedge.

In the case of termination, the value of the unfunded longevity hedge would remain with the in-the-money party, but the scheme would almost certainly be required to pay a potentially significant termination fee.

An increasingly viable alternative to termination is novation. In this scenario – if carefully structured and documented – the unfunded longevity hedge insurer drops away, but the longevity reinsurer remains and instead contracts with the buyout insurer. Under this approach, the portion of the buyout relating to the unfunded longevity hedge is priced using the longevity assumptions underlying the original unfunded longevity hedge, meaning that the scheme has been able to lock into an element of buyout pricing many years ahead of the actual buyout, thereby reducing the risk associated with targeting buyout as the endgame.

As novation of unfunded longevity hedges becomes more commonplace, we anticipate that they will increasingly be seen as a stepping stone towards a buyout.

Given this, at Insight we believe longevity hedging can help pension schemes to evolve their LDI strategy, which will in turn increase the certainty of reaching their endgame.

There are a number of steps that schemes must carry out when implementing an unfunded longevity hedge, many of which are similar to those needed when considering an insurance buy-in.

1. Feasibility study

An initial feasibility study should be carried out in order to understand:

2. Intermediation approach

The scheme must decide whether it will transact with the longevity reinsurer through either a UK-domiciled insurer or an offshore insurer; both approaches have successfully been used by UK pension schemes.

3. Data preparation

When the reinsurers are approached for a detailed quotation, they will want to receive member-level information for both in-force and historic scheme members. The preparation of this data could represent a significant amount of work and should therefore be started as early as possible.

4. Reinsurance brokerage

Pricing and key terms must be negotiated with potential reinsurers, with several rounds of bidding taking place before one or more reinsurers are selected for the transaction.

5. Transaction documentation

Once the reinsurer(s) has been selected, the transaction must be fully documented. This process will involve lawyers and advisers acting for all of the key stakeholders.

6. Ancillary services

In order to support the longevity transaction on an ongoing basis, the scheme will need to make the following appointments, all of which can be provided by a single third party:

Howard Kearns is longevity pricing director at Insight Investment