Corporate treasurers and risk managers use a multitude of resources available to them in order to evaluate and implement their companies’ policies towards currency exposure and risk.

Over the years, it has staggered me just how few use charting as a tool within this process, particularly as charting can signify very clearly when an event has or is in the process of occurring that could influence a currency’s direction for many months, even years, into the future.

What is the standard response given when I ask “why not?” Because it’s a load of tea-leaf-starring hoodoo? I beg to differ. (Although I would, because I make my living covering the major currency pairs, interest rates, commodities and equity indices.) So, let me give you one recent example of why charts are important.

The recent move from the Bank of Japan to negative interest rates came just one week after I’d flagged a really important area on the chart for the US dollar to Japanese yen.

On 20 January, we saw a dip down to 115.975. Also on this day there were some whispers (I think out of Davos) that the Bank of Japan would do ‘anything required’ to defend its currency and sustain a weak yen.

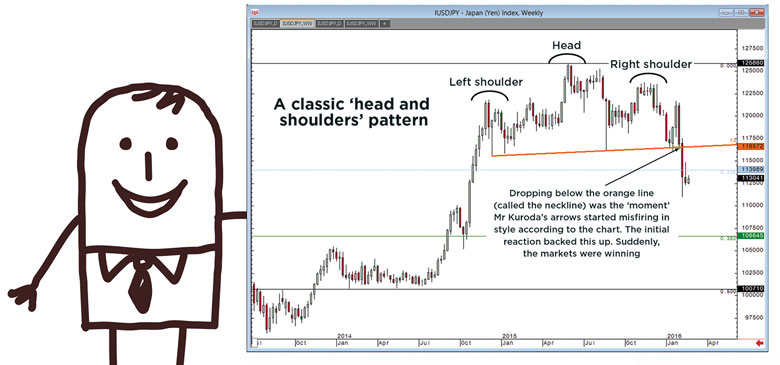

This caused a spike higher, and it was very timely because, as I’d flagged to my clients in my commentary earlier that day, 116.50 was a really important line in the sand on the chart. Had we established below 116.50, the chart (based on a chart pattern that we see repeatedly over many years, across many markets) would have given a sell signal with a target of 106-something.

Central bankers look at charts, hence the noise the Bank of Japan made on that day. They then made the move to cut rates to negative just a few weeks later, a move that saw USD/JPY spike up to 121.70. In subsequent daily commentary, I was able to highlight that this spike could just be temporary and it was actually capped by something Japanese chart watchers call the ‘Ichimoku’ cloud.

We are living in a world where central bankers appear to be the most important players in the markets, and I know central banks look at charts

It then started selling off again, and only a few days later, I was once again shouting from the rooftops to anyone that would listen, that if USD/JPY broke below 116.50, we could see a serious move lower. By 11 February, within four days of breaking 116.50, we were printing 111.00.

This was all on the charts. In fact, the charts were screaming this information. It wasn’t in the fundamentals because, according to the vast majority of analysts who don’t use charts, the Bank of Japan was going to keep ‘slinging arrows’ (to use the Bank of Japan governor’s phrase) to keep things where they wanted them.

On this occasion, the arrows missed, and the chart told us when and where this started failing, as well as offering an indication of the risks attached to such a failure.

We are living in a world where central bankers appear to be the most important players in the markets (until they’re not), and I know central banks look at charts, so surely knowing that, the rest of us need to watch the currency charts also?

Chart analysis deals with trends or, put another way, they translate the hoodoo into English, and are able to identify, most of the time, which of three trends we are seeing. I say three trends because markets can go upwards, downwards or sideways.

It is not a binary deal, and sometimes (in fact some would argue up to 70% of the time) markets trend sideways. This in itself is valuable information, and information that can be used to manage risk-mitigation strategies.

As a chartist, I am also able to approach my analysis in a very different way to economists and those analysts looking at the fundamentals. Their approach is to say “this pair should be higher because…” – which tends to mean that they are likely to still be saying the same thing a week or a month later, even if it’s lower, and even if those lower prices are clearly flagging up a change in sentiment.

A chartist, on the other hand, identifies certain price points that would change the trend, leading to a new directional skew and outlook. It is possible to be bullish one week, and then to see something happen the next week that turns the chart bearish.

I believe it is a key element of charting to have this flexibility and ability to say: “price action is signalling another sentiment change”.

Sentiment is the key word here. As per the ‘three principles of technical analysis’ (see below), everything known or thought about an asset is in the price. The price is set by the minute-by-minute auction that is open to everyone. And markets behave irrationally because they are driven by human beings.

My job isn’t to say whether I think something should be higher or lower next week or next month. It is to say whether it can – to look at the probabilities. I do not concern myself with the why, but rather the where – where things have been and where they may be going on that basis.

Technical analysis has stood up through crises past and present, and the advent of algorithmic trading is testament to its robustness.

Universities are increasingly adding it to their business and finance courses, and many businesses now make sure their staff has at least a working knowledge of the subject, or has access to analysts who can offer a technical view on market movements and potential risks.

Despite the rise of the machines, it is still people that move markets, and so markets will always be at the mercy of the irrationality of the human mind; an irrationality that can be best tracked with a flexible but robust trend-following approach.

Clive Lambert is director and chief analyst at FuturesTechs