It’s easy to think that this may never happen or that it is a 2021 issue… but alternate benchmarks are already being identified and products and markets developed. The regulatory direction of travel is strongly towards risk-free rates replacing Libor as the benchmark of choice.

And if you think that any transition away from Libor won’t affect you, think again.

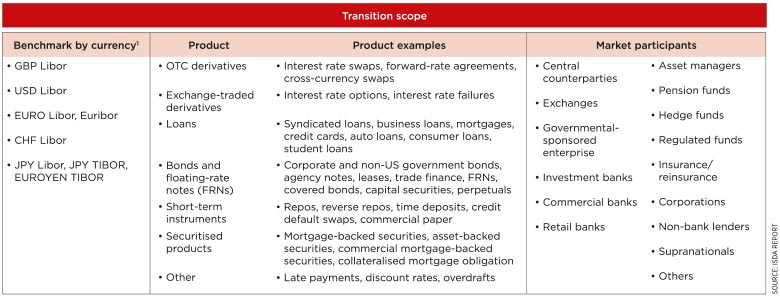

This table (from an International Swaps and Derivatives Association – ISDA – report) sets out the span of impact that benchmark transition will have and summarises which benchmarks and products are impacted.

So, if you have a loan that references Libor, interest rate or cross-currency swaps, FRNs, repos or commercial paper in issue, intercompany loans or late-payment clauses in commercial contracts, then any transition away from Libor is going to become your problem.

Furthermore, Libor is not being replaced by a benchmark with similar characteristics – so you can’t just ‘cross out the word Libor and insert SONIA’ (if it’s a GBP contract).

For example, it is currently proposed that the only benchmark that will be published will be an overnight rate, available T+1, so not only is there no term rate, any existing settlement arrangements will need to be amended, as the amount payable won’t be known until after it falls due.

Every existing contract that references Libor maturing beyond 2021 may need to be re-documented, which raises the questions:

And any contract that you put in place post-2021 may need to reference the new benchmark rate (so that could include intercompany loans and any commercial contracts traditionally referencing Libor – perhaps for late payment clauses).

The Risk Free Rate Working Groups (RFR WGs) in the various geographical jurisdictions are making decisions now on topics such as the requirement for a term benchmark.

And if the decision is taken not to publish a term benchmark, that may mean that every contact that currently references three-month Libor, for example, will need to have interest calculated on it daily and compounded to the end of the period.

This would result in no certainty of cash flow, a considerably increased workload and additional cost in systems developments.

Of course, many of these challenges can be resolved, systems can be redesigned to accommodate daily fixings and contracts can be renegotiated to accommodate delayed settlement.

However, two fundamental issues remain:

And then there’s the thorny problem about transfer of value as legacy contracts transition from Libor to the new benchmark rates.

How to calculate a new margin to be applied to contracts, while ensuring that there is no transfer of value between counterparties so that there are no winners or losers, is going to be a real challenge for all involved.

The frustration is that, as treasurers, we can’t start to make changes to transactions, contracts and systems until we know what the new world will look like – it’s the building of this New World that is happening now.

The RFR WGs around the world are already exploring whether there is a genuine need for a term benchmark, and are talking to key stakeholders, such as the IASB, to agree the approach to be taken on accounting issues arising from benchmark transition.

Corporates need to get involved in these conversations.

There will be speakers on this subject at the ACT Annual Conference in May, and there is a Corporate Forum being established under the auspices of the sterling RFR WG, to enable corporates to raise and debate the issues of particular relevance to them.

We would strongly encourage you to get involved this year – 2019 will be too late! Email our technical team and we will ensure your name is passed along to the WG Secretariat.

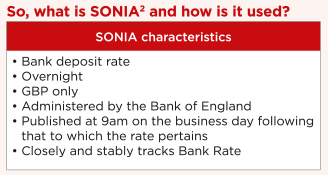

The sterling overnight indexed average (SONIA)[2] reflects bank and building societies’ overnight funding rates in the sterling unsecured market.

SONIA is a transactions-based benchmark. In 2017, the average value of transactions used in the calculation of SONIA was £46bn; this represents more than 95% of the overnight sterling wholesale unsecured deposit market.

In contrast, while significant improvements have been made to Libor since April 2013, the absence of active underlying markets raises a serious question about the sustainability of the Libor benchmarks based upon these markets[3].

On each London business day, SONIA is measured as the trimmed mean, rounded to four decimal places, of interest rates paid on eligible sterling denominated deposit transactions.

Eligible transactions include unsecured overnight transactions greater than or equal to £25m in value reported by banks and building societies to the Bank of England.

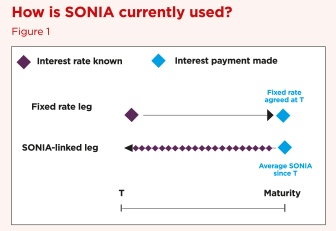

SONIA is the existing unsecured reference rate for the sterling overnight index swap (OIS) market. In an OIS, a fixed interest payment is exchanged for an interest payment based on a daily compounding of SONIA rates over the interest payment period – see the following diagram:

OISs are used by firms to hedge or take positions on Bank Rate as SONIA has historically closely tracked it.

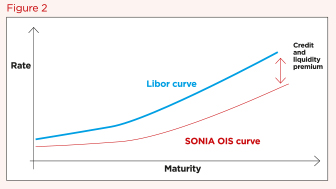

The OIS yield curve is widely used to value contracts and calculate margin requirements. OIS rates (the fixed leg) reflect the market’s expectation of the compounded SONIA rate over the term of the swap and a resulting yield curve can be constructed – see the following diagram:

This curve tends to trade at lower rates than the Libor curve as SONIA OIS is risk-free and does not include term bank credit risk.

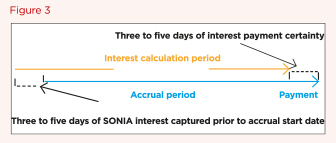

Other financial instruments, including bonds and loans, could have interest payments linked to the compounded SONIA rate for a given period (for example, three or six months).

However, similarly to OIS, the interest coupon payable would only be known with certainty after the end of the interest period.

There are potential workarounds in order to facilitate settlement.

For example, the contract could have an ‘offset’ approach in which the interest calculation period began a few days (for example, three to five business days) prior to the accrual start date and ended a few days prior to the interest payment date[4] – see the following diagram:

For hedging purposes, end users may want to replicate the same settlement structure for their swaps.

SONIA transition work is being coordinated by the market-led Working Group on Sterling Risk-Free Reference Rates[5].

In addition to talking to your counterparties to understand how they plan to structure your trades going forward, you can engage further with the work of the Working Group by expressing your interest via email.

The Working Group has set up a subgroup to consider whether a robust-term benchmark based on SONIA OIS could be created. It will consult on this in Q2 2018 and your input into this consultation will be vital.

Sarah Boyce is associate policy and technical director at the ACT

This article was taken from the April/May 2018 issue of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership