Firms concentrate on a handful of KPIs when presenting their financial performance externally. Commonly, these include revenue growth, operating profit growth and margin, earnings per share (EPS), and return on capital employed (ROCE). The first four metrics look at key items from the income statement and, to many people, these really are the KPIs that count. But in a nod to the concept of value, cash and the balance sheet, ROCE also often gets reported on. Indeed, ROCE is now a common metric in remuneration schemes and longer-term performance plans. But while the income statement KPIs are often explained and analysed in great detail, ROCE is almost, without exception, left to speak for itself. But what exactly is ROCE trying to say?

Speaking to equity analysts about their valuation approaches, none of them identified ROCE as a metric that plays into the share price targets they set. Many look at multiples of income statement elements such as net operating profit after tax (NOPAT) or EPS. All of them triangulate these multiple-based valuations with a discounted cash flow calculation. ROCE is noticeable by its absence.

So, why do so many firms insist on reporting ROCE? The straight-bat answer is that it is accepted that returns on capital are the underlying driver of value creation, they are higher in well-run firms with good strategy and execution, and this, in turn, feeds the profit-related metrics that most people actually focus on. What I mean by that is that good underlying returns on capital drive revenue because they represent good market positions. They directly drive operating profit because the depreciation charges are lower (more cash profit per £ of capital invested). However, an alternative, more cynical, answer is that ROCE almost always looks impressive when put alongside the firm’s weighted average cost of capital (WACC).

This is for two reasons:

1. The ‘return’ part is based on NOPAT and, very often, this is a higher value than the cash equivalent number (EBITDA less capital expenditure and tax).

2. The ‘capital employed’ part is based on balance sheet book values. These book values are out of date, depreciated, and often bear absolutely no relationship to a true replacement value.

So ROCE invariably benefits from a higher numerator, profit being greater than the cash equivalent, and a lower denominator, with the balance sheet amortised and based on historic cost, when compared to a value-based analysis which would prescribe the cash equivalent of NOPAT and replacement, not book, asset values. Attempts to address these shortcomings result in a plethora of potential adjustments, such as the 150 plus attributed to Economic Value Added.

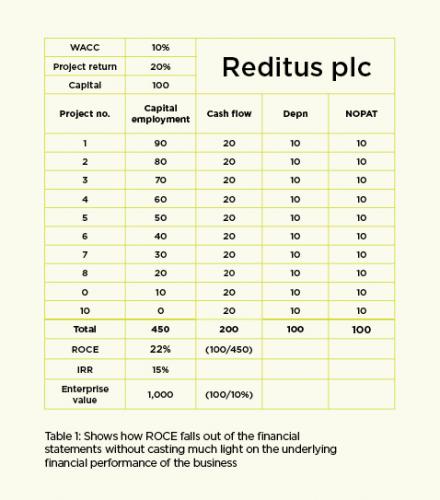

Table 1 (below) shows a fictitious business, Reditus plc, which invests £100 a year in a project that produces an internal rate of return (IRR) of 15%. It repeats this year after year, and the life of each project is exactly 10 years. Once in steady state, after 10 years of repetitive investing, the firm reports a NOPAT of £100, and has a balance sheet book value of £450. Reported ROCE drops out at 22%, and this is much higher than the IRR of each project. If we also assume that the WACC of the firm is 10%, we can derive a theoretical enterprise value of £1,000.

When reporting the results of the business, management can claim amazing returns on capital of 22%, “way in excess of our cost of capital”. But if you are confused as to what the ROCE value of 22% is telling us, then join the club. It doesn’t really tell us anything.

Fundamentally, ROCE is a valiant attempt to apply the economic concept of value to accounting numbers. Unfortunately, ROCE doesn’t really work, and this leads to a number of drawbacks:

1. The absolute value of ROCE does not relate to the economic rate of return.

2. It deters investment over and above anything other the ‘run rate’ level of growth.

3. There’s no meaningful way of setting a target if it is to be used in executive awards.

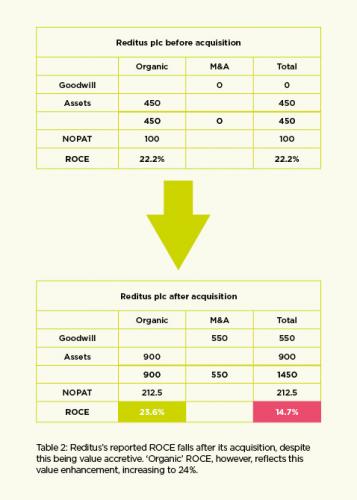

Let’s develop the Reditus plc story further, with the addition of some M&A activity. The firm takes up the opportunity to acquire another business for £1,000, £450 of which is underlying PPE, £550 is goodwill – i.e., the premium paid to book value to acquire the business. This new business is forecast to generate an IRR of 11%, so it is value accretive compared with Reditus’s WACC of 10%.

The firm is correct to take this opportunity. However, unfortunately, ROCE drops to 15% after this acquisition. A bit of a conundrum to explain externally, and worse – if ROCE is part of the executive award programme – potentially quite unpopular. Table 2 shows the balance sheet and NOPAT of Reditus under this M&A scenario.

But all is not lost. I want to introduce the concept of ‘organic’ ROCE to you. Organic ROCE strips out M&A-related balances to at least get back to an unadulterated figure. Table 2 illustrates this. The organic ROCE of Reditus after the acquisition has risen from 22% to 24%, reflecting a deal that has added value.

Without carving out organic ROCE, reported ROCE shows a decline to 15%. Organic ROCE does allow for some comparability across sector peers to gauge who might be generating higher returns from capital. Many caveats persist to this analysis.

There is another indirect source of affirmation for ROCE to which I want to draw your attention. Joel Greenblatt, in his book The little book that still beats the market (2005), describes an investment rule that incorporates ROCE. His method is to rank firms according to ROCE and earnings yield (taken to be earning over market value). He then scores each ranking, one being highest, combines each firm’s score, and chooses the top 30 (the 30 firms with the lowest score) as an investment portfolio.

Back-testing this portfolio produced a return of 189% over a 10-year period. This is an annual capital gain of 11%, which, when combined with dividend yield, far outperformed the equivalent return from the whole market. Indirect proof that ROCE does have some bearing on value creation and, ultimately, enterprise value.

In my next article, I will introduce a concept that, when applied to ROCE, transforms it into a much more useful, transparent and explainable metric. This very simple change can make ROCE fit for purpose after all.

Ben Walters is the former deputy treasurer of Compass Group

This article first appeared in The Treasurer Issue 1, 2025

You may also like