Counterparty risk has increased in importance since the financial crisis. Indeed, in many surveys of treasurers, it is cited as one of the top three risks facing the treasurer or company. That’s not to say that the subject was not considered important prior to the crisis – it was, but it was just not assessed with the same rigour seen today.

Counterparty risk is the risk that a counterparty to a contract will not perform their part of the contract

Two major factors are behind this increased focus on counterparty risk. Firstly, the creditworthiness of banks has fallen as they are no longer seen as incapable of failure. Secondly, there is a rise in cash holdings by many of the world’s corporations (both large and small) as they hold back on capital expenditure in an uncertain economic environment and protect against future liquidity risk. Investing cash is probably the most obvious activity where counterparty risk is considered. It is by no means the only one, however, and banks are not the only class of counterparty where risk arises.

Counterparty risk is the risk that a counterparty to a contract will not perform their part of the contract, such as repay a deposit of cash, settle an invoice or supply goods when due. This is called ‘default risk’. It also refers to how much of the contract is performed. In some defaults, all the amounts at risk might be received (for example, in a secured lending), or just some might, or indeed none at all. The total amount of funds lost is known as ‘loss given default’.

In this article, we will look at how counterparty risk arises, how we might measure it and, finally, how we might manage it.

Before we can establish a policy for managing counterparty risk, such as setting an objective and assigning responsibilities, we need some way to measure these risks. There are two key dimensions to this. Firstly, we must measure the size of the risk. Secondly, we must measure the likelihood of default and any subsequent loss.

We can measure the exposures relatively easily (for example, size of term deposit or derivative valuation) although the measurement of long-term customer or supplier risk, for example, is a bit more difficult. There are also some other complications to be aware of, which take into account the complexity of banking groups. When measuring counterparty risk size, this should be done by:

A further dimension to consider is type of counterparty. For example, when measuring investments, types might include:

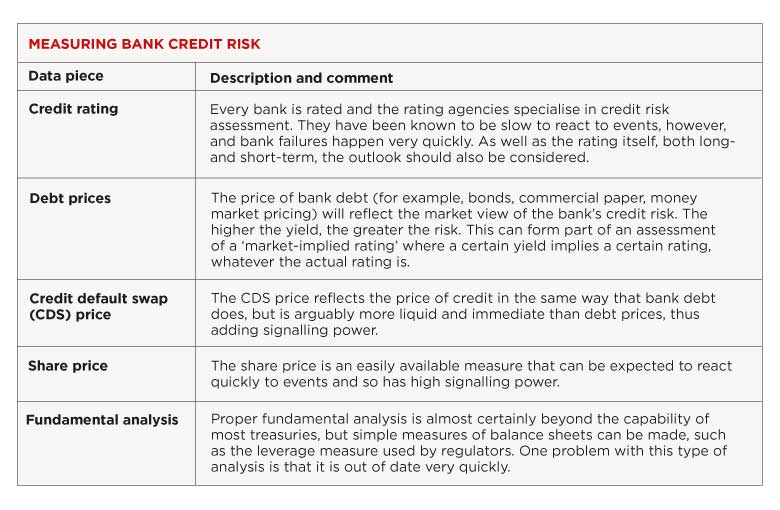

This measurement is arguably more challenging and amounts to an assessment of credit risk of the counterparty. We will restrict ourselves to measuring bank credit risk, although the same principles broadly apply to other types of counterparty.

A particularly useful way to analyse some of this data is to use it against a benchmark of the sector. So if, for example, the CDS price of a bank was rising (worse credit risk) faster than its peers, that would be a warning sign. Similarly, if the share price was falling (worse risk) faster than its peers, that would also be a warning sign.

Having measured the size and likelihood of an exposure, then the next stage in counterparty risk management is to establish a set of limits, which is the typical response to this risk. Limits should be set within an overall risk management approach using the concepts of risk tolerance, appetite and budgeting. Companies taking high business risk might decide to take minimal counterparty risk and invest only in ‘risk-free’ sovereign instruments. Some companies may take different amounts of risk with different cash segments, such as core long-term cash, compared with cash needed for paying wages or suppliers. Limits should be set, taking into account the following:

Limits should be aggregated across the company so that limits are not broken by two parts of the organisation acting independently.

Risks should be measured on a regular basis and there should be an ability to react to changes in risk quickly, bearing in mind how quickly banks, in particular, can fail. Some companies use a traffic light system, based on a combination of the measures in the table above left, which can be used as a trigger for action.

It is impossible to eliminate credit risk, but a company should understand the risks it faces and be in control of them.

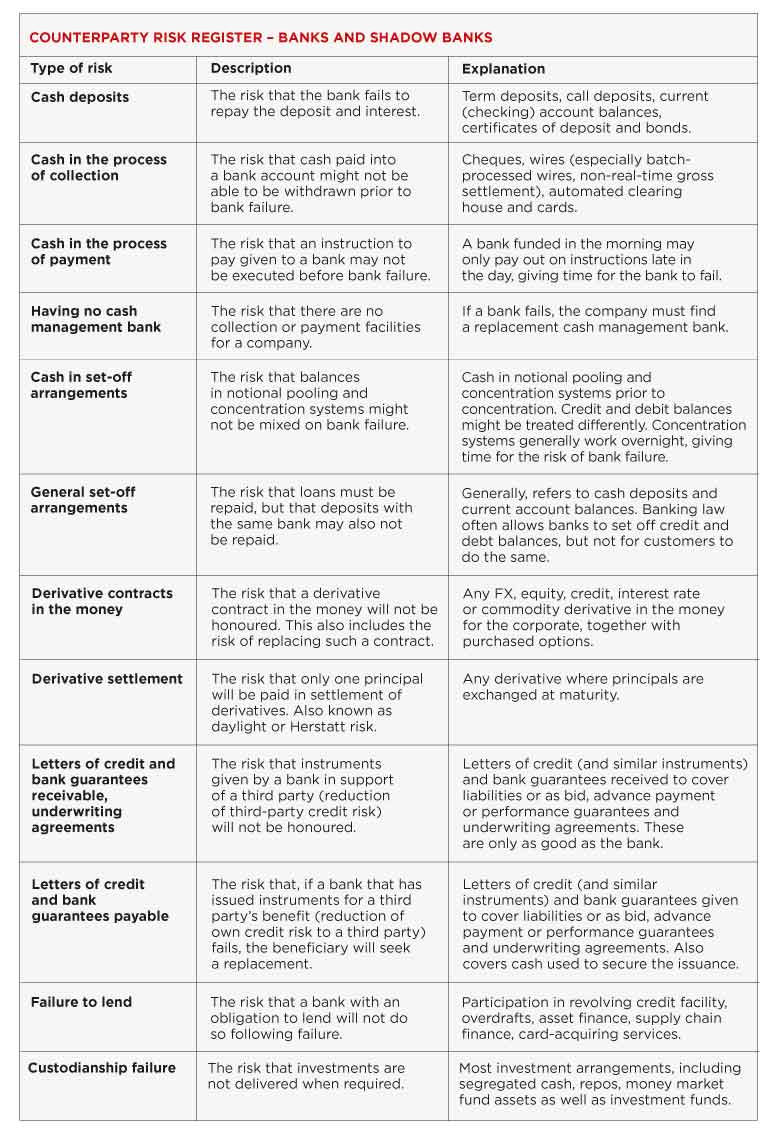

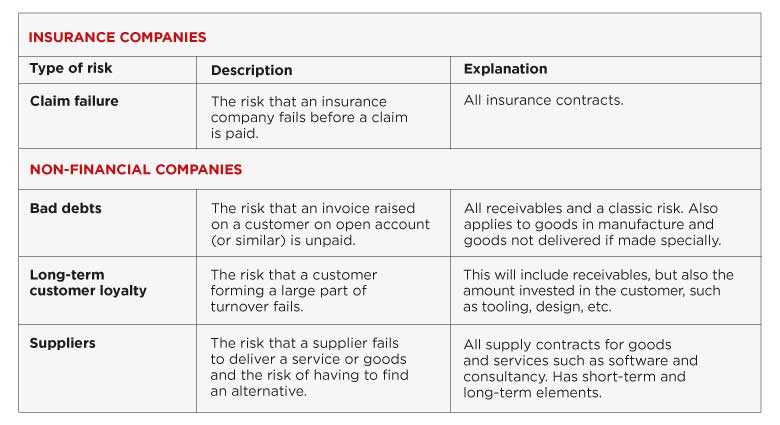

Counterparty risk can arise for a corporation in the following most important ways:

Note: Shadow banking includes activities such as money market funds and hedge funds, although it also involves securitisation and collateral intermediation. Firms that mimic banks, for example, in providing FX derivatives, would also fall into this category.

One positive aspect of assessing bank credit risk is that there is plenty of data available to use:

Will Spinney is associate director of education at the ACT