Corporate borrowers often need to renegotiate their existing loan liabilities, and in many companies this responsibility will fall on the treasurer. Although treasurers may not necessarily be accounting experts, they still need to carefully consider the potential accounting impacts when renegotiating loan terms. Under IFRS 9: Financial Instruments, loan modifications can trigger gains and losses for financial reporting purposes and may even have tax implications.

ABC PLC, a fictional firm, has a £500m bank loan entered into three years ago. ABC PLC pays interest at the Sterling Overnight Index Average (SONIA) plus 2.50%, and the term was originally agreed to be five years, leaving two years until maturity.

The original plan

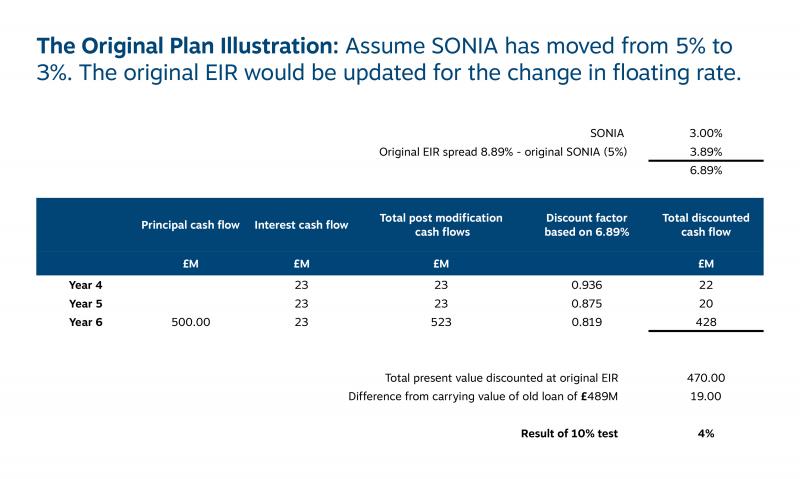

ABC PLC has been performing well recently, and its credit standing has improved significantly. As a result, ABC PLC renegotiates its loan with the existing bank, extending the term by one year and reducing the interest rate to SONIA plus 1.50%. The treasurer is delighted with the new agreement – until he gets a panicked call from the finance director. The loan renegotiation has triggered an accounting gain of nearly £19m which, while sounding positive, raises concerns about potential tax implications that could result in a £5m cash outflow.1 Emergency meetings with the company’s tax advisers ensue and, ultimately, the loan renegotiation is postponed owing to the associated tax and accounting risks.

The alternative plan

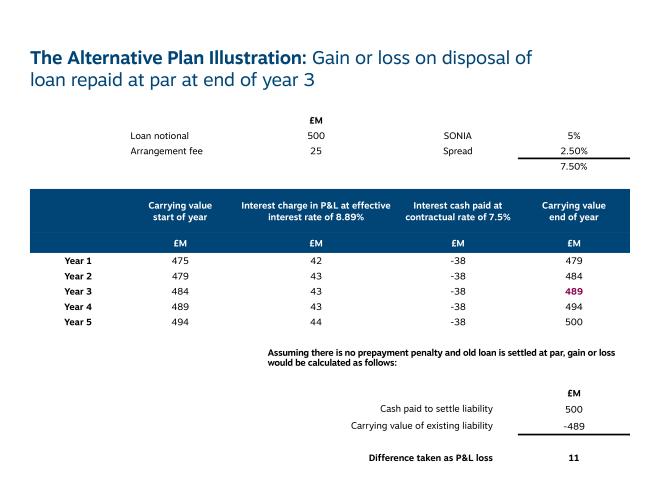

A few weeks later, one of the company’s advisers suggests an alternative plan: prepay the existing loan and take out a new three-year loan with another bank. This structure has the same economic impact as renegotiating with the existing bank – ABC PLC moves from a £500m loan paying interest at SONIA plus 2.50% with two years remaining to a £500m loan paying interest at SONIA plus 1.50% with three years remaining. However, to the treasurer’s surprise, the accounting outcome is entirely different. Instead of recognising a £19m gain, this new structure would result in an immediate £11m loss.

The accounting rules around loan modifications are complex and often misunderstood. The rules for IFRS preparers changed in 2018 with the introduction of IFRS 9, and even experienced accountants can be surprised by the requirements’ nuances, especially given that many companies encounter loan renegotiations infrequently. The best way to gain a high-level understanding of loan modification accounting is to walk through the process step by step.

1. Decide whether the transaction is a modification or not

Modification accounting applies when an existing contract is renegotiated or when there is an exchange of debt instruments between an existing borrower and lender. Conversely, settling an existing debt instrument with one lender and taking out a new one with another lender is accounted for as extinguishment of the old debt, followed by entering into entirely new debt. In ABC PLC’s case, taking out the new debt with another lender (the ‘alternative plan’) would involve derecognising the old loan, which is carried on the balance sheet at £489m. Under IFRS, loan liabilities are typically carried at an amortised cost (par value adjusted for unamortised issuance costs):

2. Determine whether the modification is substantial or non-substantial

Assuming ABC PLC decides that the transaction is a modification rather than an extinguishment, the next step is to determine whether it is substantial or non-substantial. First, ABC PLC must apply a quantitative ‘10%’ test. This involves calculating the present value of the modified cash flows, discounted using the original effective interest rate (EIR) and comparing this figure to the current carrying value of the old loan. For ABC PLC’s original plan, the calculation would look like this:

If the difference is less than 10%, the modification is deemed non-substantial, and the loan would be adjusted to a new carrying amount of £470m as per the 10% test. This adjustment would result in an immediate £19m gain in the profit and loss account. If the modification were deemed substantial due to qualitative factors, the transaction would be accounted for as an extinguishment of the old loan, leading to an outcome similar to the alternative plan.

Over the remaining three years of the new or modified loan, the profit and loss impact of the two structures would be the same. The original plan initially shows a £30m difference (£19m gain + £11m loss) compared with the alternative plan but will incur a higher EIR over the remaining term, resulting in interest charges £30m higher than under the alternative plan. However, these timing differences between different financial reporting periods can have significant accounting and tax implications.

Navigating the intricacies of loan modification accounting under IFRS 9 can be challenging, even for seasoned professionals. The financial reporting and tax implications of these decisions are significant, and missteps can result in unexpected gains, losses, or tax liabilities that may impact your organisation’s financial health. Given the complexity and potential risks involved, treasurers should ensure that they fully understand the accounting consequences of any refinancing strategy. Engaging with an expert in financial instrument accounting can provide the specialised knowledge and guidance necessary to manage these transactions effectively and avoid costly surprises.

1 Please note that the tax position of accounting gains from loan modifications varies by jurisdiction and is dependent on the specific facts and circumstances of the taxable entity. Professional tax advice should be sought when assessing the tax implications of specific loan renegotiation terms.

Kern Roberts is managing director, global accounting practice lead at global financial risk management firm Chatham Financial