Funding is a scarce resource and the banking sector, acutely aware of this fact, has started to incorporate funding adjustments into uncollateralised derivative contracts. The process is not without difficulties, however, and no consistent pricing framework exists, partly due to the disparity in funding costs experienced across the banking sector.

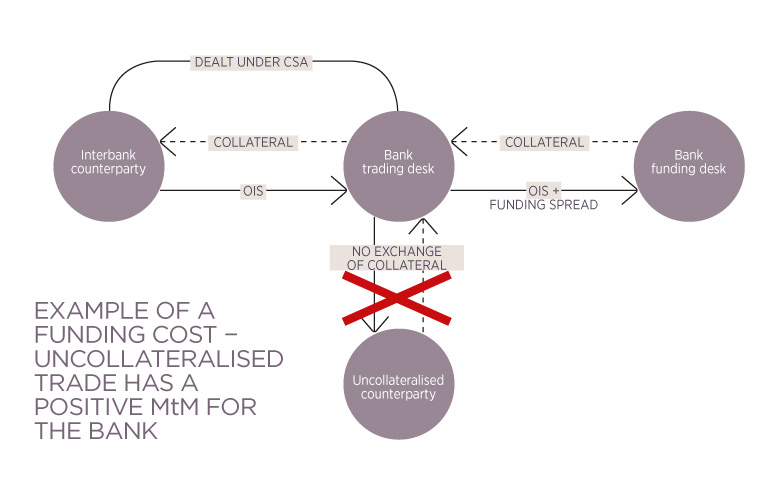

The main issue is the imbalance that exists between collateralised trades on one side – the interbank market, supported by credit support annexes (CSAs) between banks with daily margining and zero thresholds – and uncollateralised or partially collateralised trades on the other. The asymmetry creates a funding headache for banks. For example, if a bank trades an uncollateralised interest rate swap with a corporate client and this swap has a positive mark-to-market (MtM) value from the bank’s perspective (ie the bank is in the money), a funding cost exists because in the mirror interbank hedging trade the bank has a negative MtM and is required to post collateral to the interbank counterparty. The CSA governs the rules around posting collateral and stipulates the rate of interest payable on each currency that collateral can be posted in; this is typically an overnight index rate (OIS) such as euro overnight index average (EONIA), sterling overnight index average (SONIA) or the federal funds rate. Since collateral must be funded at a spread to these rates, there will be a funding cost related to posting collateral. For the banking industry as a whole, the Libor-OIS three-month spread may be the broadest indicator of this cost in the short term – OIS being the best proxy for the risk-free rate.

Lower-rated banks may find themselves very uncompetitive for certain derivative products

If the trade described above is reversed and the bank has a negative MtM on the uncollateralised trade, then the bank experiences a funding benefit. The bank will receive collateral in the interbank trade, pay an overnight rate and can reinvest the funds at a higher rate. If a bilateral approach to counterparty risk is taken, this also creates a debt value adjustment (DVA) gain.

From the above, it is reasonably clear to see how funding costs and benefits may develop in the future and how they might impact on a swap unwind where there is a significant settlement value. Conceptually more puzzling is the idea that trades initiated with zero net present value contain an element of funding. This seems counterintuitive because the derivative is neither an asset nor a liability at inception; but factors such as payment frequency, the shape of the yield curve, and whether a counterparty is paying or receiving the fixed rate, mean banks can estimate an expected future path for MtM over the life of a derivative. Once this expected path has been identified (usually through the process of Monte Carlo simulation), a funding spread is applied and an overall funding cost or benefit is derived. This funding value adjustment (FVA) is therefore the expected future funding impact from holding the uncollateralised trade due to the requirement to post or receive collateral in the interbank hedging trade. FVA is implicit in the overall credit charge a counterparty faces when they initiate a trade.

Similar to credit valuation adjustment (CVA), the management of derivative funding requirements has been centralised within banks where a specific internal desk is responsible for borrowing from or lending to trading desks at OIS plus a margin. This helps foster a consistent pricing framework that ensures uncollateralised counterparties receive fair adjustments from their bank whether the transaction involves a funding cost or benefit. This internal funding desk is also mandated to work closely with the CVA desk in order to maximise funding and reduce CVA of uncollateralised derivative portfolios in a way that may benefit all counterparties.

The desk must determine how to charge funding and at what spread. Careful consideration will be given to construction of the funding curve, whether to apply funding for the full term of a derivative transaction considering many are restructured or unwound before maturity, and how to apply the funding spread in various scenarios – new transactions may carry different spreads compared with novations that already contain a significant MtM. potentially, these decisions could have a detrimental effect on the underlying business. Lower-rated banks may find themselves very uncompetitive for certain derivative products if they attempt to pass on their own cost of funds in entirety, so there is often a trade-off between remaining competitive and accepting the costs of doing business.

The Libor-OIS spread may be a short-term cost, but perhaps the bond-credit default swap spread is a better barometer of an individual bank’s liquidity costs. What about a weighted average own cost of funds curve that would incorporate a bank’s own default risk as well as liquidity costs? After all, if a significant cancellation payment must be made to unwind a long-term swap, this must be funded with a long-term borrowing. The funding spread applied will be dependent on the internal counterparty credit risk model used.

Earlier, I referred to DVA, a curious accounting situation where a bank can benefit from its own default. If applied, this adjustment for a bank’s own default risk will reduce the credit charge of a trade at inception. I stated that a funding benefit and a DVA benefit occur in tandem when a trade has a negative MtM for a bank. An uncollateralised counterparty looking to unwind such a trade would have to compensate the bank for its funding cost and loss of DVA. If own cost of funds is used to charge funding, there is a double count. Therefore, in the bilateral CVA/DVA approach, a pure liquidity cost may be more appropriate to use as a funding spread.

DVA and FVA reflect the new reality in uncollateralised derivative pricing. Their implementation and the interplay between them continues to be the subject of much debate and financial literature, but what is not in doubt is that funding adjustments are now integral to recognising the true economic value of a derivative.

Paul Sills is in corporate derivative sales at BBVA.

E: paul.sills@bbva.com