Historically, environmental, social and governance (ESG) investing was about excluding stocks of undesirable companies from portfolios — often because they violated one’s sense of ethics or values. ESG investing has since expanded to include consideration of ESG criteria alongside financial ones. ESG is growing in importance among institutional, wealth and retail investors. In recent years, institutional and high-net-worth investors’ adoption of ESG, along with the subsequent growth in ESG assets under management, has accelerated with ESG, green, climate change and so on all becoming labels we increasingly hear about in the news. As treasurers, we can play an important part in improving the impact of our company on the planet. This article is based on an interview with Tom Bolton – head of corporate finance at Thames Water – one of the UK’s largest utility companies. Utility companies like Thames Water have been keen advocates of green bonds (generally thought of as a fixed-income instrument launched to fund specific environmental or green projects, such as CO2 reduction). They have been active issuers in the market, with Anglian Water being the first to issue in 2017. Others have followed suit and Thames Water was the first UK corporate to issue a green US private placement market in 2018.

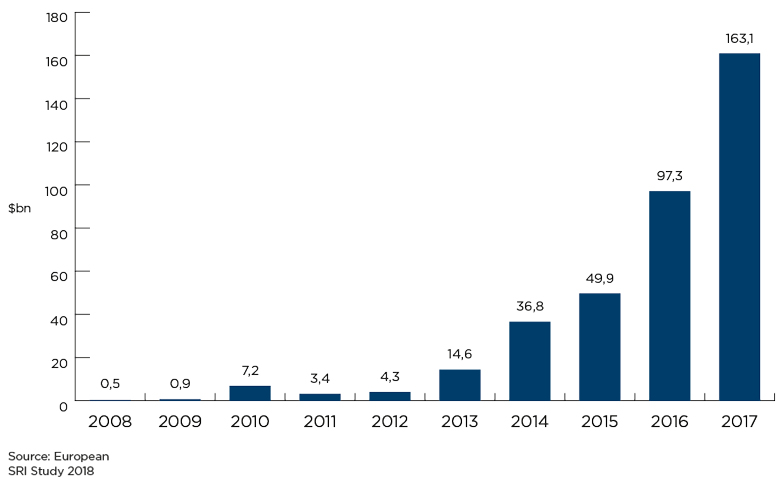

Historically, issuing green bonds was a way of diversifying investor bases and potentially reducing borrowing costs. There was a lot of sceptism over the true impact on the environment as investors chased scarce projects, and many investments were made to hit management targets rather than for genuine effect. Issuing green bonds can typically result in more effort and costs for a corporate. An extra layer of due diligence is required to validate the green credentials initially and on an ongoing basis and costs can range from anywhere between £20,000 and £100,000. In some cases, the funds raised need to be segregated from general corporate purpose funding, and this requires additional reporting and monitoring, and can lead to disclosure considerations over net debt and liquidity. The assumption that green bonds could attract cheaper funding hasn’t always been the case and many corporates have historically found that the overall effect of issuing green bonds has been cost-neutral at best. The market has grown exponentially (see table below) and at the same time matured, with new variants including ‘blue’, ‘sustainability’ and ‘social inclusion’ bonds.  There are several factors driving this increase, including:

There are several factors driving this increase, including:

Asset managers have always been interested in the ESG agenda, but typically this has been as a small proportion of their portfolio and addressing the needs of a small segment of their market. In recent years, there has been renewed focus driven by various initiatives, including:

As a result, and as noted by Bolton, UK and European investors are now carrying out much more thorough ESG credit analysis. This illustrates the growing maturity in the investment community and that ESG investing is no longer a side project, but one where serious investment in staff and methodologies is being undertaken. (We will be covering the role of the credit rating agencies in the ESG space in an article later in the year.)

Bolton has been following the ESG market for a number of years, including during his previous role within debt capital markets at BNP Paribas. Increasing the focus on green financing has been one of his main objectives since joining Thames Water. Over the years, there has been a temptation, for companies to engage in what is often referred to as ’greenwashing’. This occurs when an organisation spends more time and money claiming to be green through advertising and marketing than actually implementing business practices that minimise environmental impact. Bolton has been keen to demonstrate that Thames Water is making a genuine difference and explained that the sustainability team at Thames has taken a purist view towards ESG and that they are keen to focus on doing the right thing and not oversell the programme. This might account for why we haven’t heard much about their US dollar private placement of green bonds and their revolving credit facility, which now has ESG KPIs associated with it and under which charities benefit if the company outperforms its targets.

A key requirement for issuance is setting up a green bond framework. This communicates the key message to investors and offers details about the use of funds. For Thames Water, along with other issuers, this messaging should already be a key component of the communications strategy. There are a number of examples available, including guidelines from the International Capital Market Association (ICMA), The Prince’s Accounting for Sustainability Project and one from Thames Water. Once the framework has been defined, it is important that any projects are fully aligned. While the ICMA Green Bond Principles provide a framework for issuance, these are voluntary, and there remains some ambiguity as to what defines a green bond. The EU is working on a standard taxonomy (which is due to conclude during 2019) as a key part of developing an EU system of classification, creating an EU green bond standard, introducing minimum standards for low-carbon indices and improving climate information disclosure. It is hoped that this will offer clear guidelines on the definition of what constitutes a green rather than brown issuance. This means that any issuer currently has to create its own framework, which right now allows for a broad range of interpretation. The framework then typically requires an independent organisation to verify the KPIs that govern the project and will provide ongoing monitoring to ensure that it remains in line with the agreed framework. Bolton’s approach is to listen to investors to understand what they want and to take account of different requirements across different geographies. He finds that most investors are more focused on the overall approach adopted by the company as this sets the tone. Investors seem to want to understand that ESG has been truly embedded across an organisation rather than purely for financing reasons or as a specific project, and this includes the focus that it receives as a topic at executive and board levels.

As I reflect on my conversation with Bolton and others recently, I can see that my original scepticism of a few years ago is being replaced with a recognition that genuine and meaningful promotion of ESG is under way. There are still plenty of challenges ahead, but I look forward to stories of who is not doing something ESG-related, rather than who is, and to hearing more about how organisations are building natural capital calculations into their business models, alongside traditional forms of capital, such as economic and human.

Naresh Aggarwal is director – policy and technical – at The Association of Corporate Treasurers