All treasurers as well as finance professionals with treasury responsibilities will have recently found that their management teams have developed a welcome preoccupation with the liquidity of their organisation. This article offers three tips that may be helpful.

Many organisations will already have such forecasts under way as a matter of course. If your organisation has not already done so, now is the time to start.

The reason is that the 13-week forecast is an incredibly helpful tool for the majority of businesses in understanding whether the organisation is in danger of running out of cash. It allows the management team to understand the short-term liquidity picture and gives it a perspective on what needs to be achieved – and how quickly – in order to remain solvent.

It is also helpful in establishing credibility with lenders if you need to engage with them for further potential funding. It shows how quickly they need to react, and the scale of the short-term requirement. Interim arrangements may be agreed, while all parties work together to determine a longer-term solution to any financial difficulties faced.

In my experience, it generally takes a few weeks before the forecasting processes settle down, so it is best to start as soon as possible – if these are not already in place.

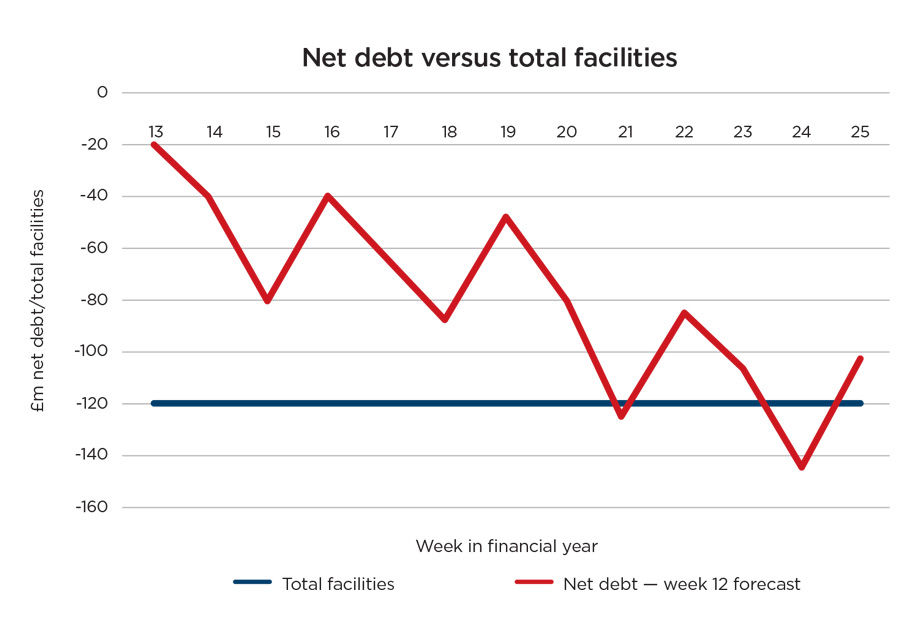

Many numbers will be involved in generating a cash-flow forecast, but it is important to keep the message as simple as possible for stakeholders to understand. Some visual presentation of the facts may help to get the key messages across. For example, the fact the organisation runs out of facilities in week nine of this forecast (and more seriously in week 12) is quite easy to grasp from the graph below.

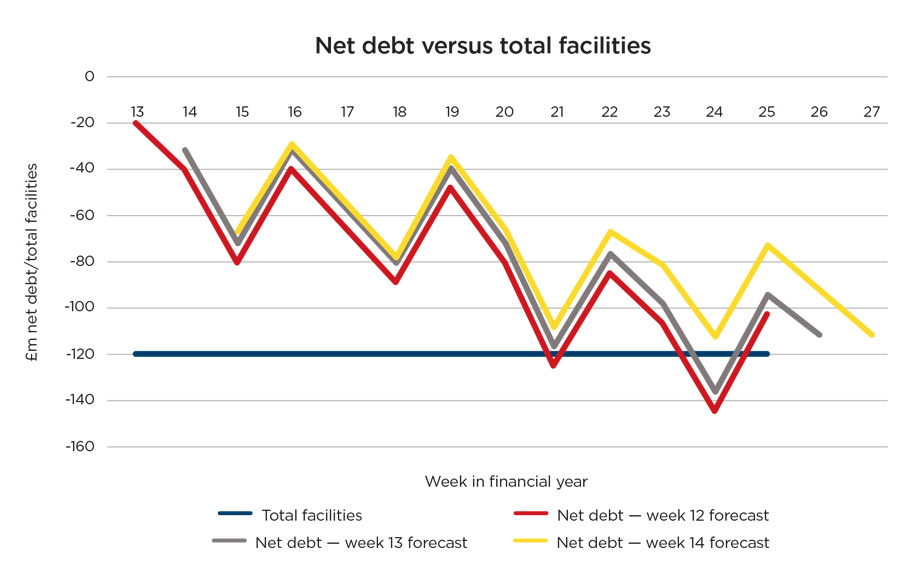

Clearly, a graphic such as this will concentrate minds as to what actions can be taken to mitigate cash outflows and improve the overall position. This will yield hopefully improved forecasts in subsequent weekly forecasting. While again there will be much numerical analysis, the position can be visually illustrated as per the graph below, which may feel more intuitive to some stakeholders.

Many organisations will be in for a prolonged period of uncertainty in the current environment. Judgements around assumptions will need to be dynamic and responsive to up-to-date information. Major assumptions may well change from one week to the next and need to be based on the best view at the point in time the forecasts are compiled.

The volatility of cash flows can be much more significant than the volatility of accounting profit measures. The knock-on impact of changes in demand on working capital needs to be carefully scrutinised.

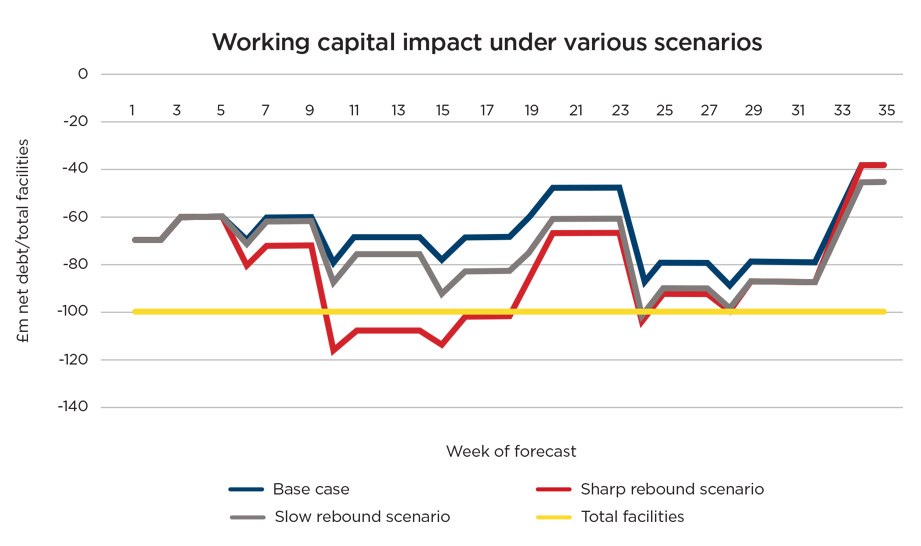

To demonstrate this, I have constructed a simplified financial model projecting weekly net debt predicated on a manufacturing company with total debt facilities of £100m and normal working capital ratios. In the current environment, it operates at broadly cash break-even on an annual basis (the ‘base case’). I have then generated two scenarios. One assumes a sharp rebound scenario where monthly sales increase by 30% to a new level in a single month (the sharp rebound scenario). The other assumes a 5% increase in monthly sales for three consecutive months such that, in due course, monthly sales end up approximately 15% higher than the base case. This is the ‘slow rebound scenario’.

The base case scenario shows that the company can operate safely within its total facilities.

The sharp rebound scenario shows a problem. Despite the fact that the company will be earning greater accounting profits given the higher sales, the extra cash generated from increased profitability is insufficient in the short term to fund the additional working capital requirements. Consequently, the company breaches its available debt facilities, despite the trading environment improving, unless it is able to organise additional short-term funding.

The slow rebound scenario shows that the business can just about manage within its existing debt facilities – providing it takes some temporary action at the two points where debt facilities are marginally exceeded. This scenario features a lower increase in profitability from increased sales combined with lower working capital requirements to fund the upturn in trading.

In summary, the treasurer can make an important contribution to protecting and enhancing the value of their organisation if they:

Ensure a 13-week rolling cash-flow forecast is produced and updated weekly;

Communicate effectively the outlook and implications of the forecast to stakeholders; and

Be vigilant to the working capital implications as any economic recovery progresses.

David Tilston is a fellow of The Association of Corporate Treasurers, a chartered accountant and a member of The Institute for Turnaround