As with everything else in 2020, company accounts will be remembered for all the wrong reasons.

There are COVID-19-related uncertainties in virtually every element of the balance sheet and profit and loss account.

One response has been the ingenious but implausible earnings before interest, tax, depreciation, amortisation and coronavirus (EBITDAC).

However, COVID-19 accounts are not like other accounts. Even the priorities have changed and, for many, it’s a case of cash first, then forecasts, and only then profits.

Those compiling accounts early in the crisis understandably took a cautious line, but as time went on, ‘wait and see’ was less and less tenable.

Not taking a view on prospects and valuation is action. Nor can the accounts be dismissed as one-off and irrelevant. They are just as important as ever as signals for shareholders and internal decision-making, including pay.

Recognising that treasurers will be in a variety of roles – including preparers, interpreters and users – central to each is the role of judgement.

Even before COVID-19, this regularly topped the Financial Reporting Council list of top issues of concern.

This year, the plausibility of revenue assumptions is only the start. What about supply chains and getting the right people in the right place?

Even if the customers are there, there must be credible plans to supply them. Then there is the question of whether the customers have the means to pay and whether they will do so.

The biggest elements of judgement related to the COVID-19 accounts are often loss of provisions, asset impairment (including goodwill) and above all whether the company is a going concern. Even the non-financial elements of reports are full of judgements.

How are these to be approached?

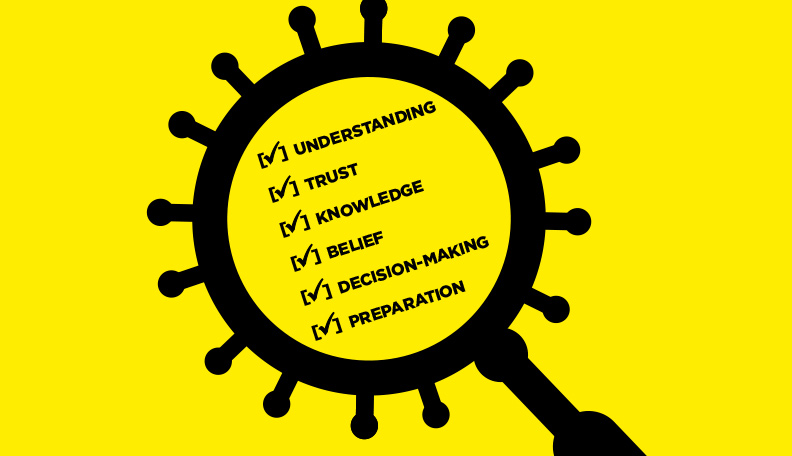

Using a definition of ‘the combination of personal qualities, relevant knowledge and experience with professional standards to form opinions and make decisions’, I discussed how to improve the chances of getting judgements right with regulators, preparers and users.

The framework – endorsed by the Brydon Report in December 2019 – has six elements. These are set out below, with some examples of the special factors in COVID-19 times:

The quality of what is understood in written material and heard in meetings is an important basis for judgement. The current uncertain situation puts a premium on clear explanation.

So, distanced working may have many upsides, but it has limitations as a form of nuanced communication. There is also the need to be aware of what others are doing and the changing nature of what is acceptable.

This is essential to the quality of judgement, whether it is in the competence of a member of the team or the integrity of those preparing the accounts.

Establishing credibility through probing consistency and track record remains the key. Again, remote working makes extra effort essential to observe personal demeanour.

At a time when so much is uncertain, a background of professional knowledge and experience are of great value.

However, personal flexibility and adaptability is essential to put that knowledge and experience into the context of the current situation. For example, the appropriateness of analogies, proxies and generalisations (“It’s just like the financial crisis”) need to be questioned.

It is inevitable that we approach matters with personal views, beliefs and biases. That includes our risk tolerance or appetite. What matters is not that we deny or try to eliminate these, but that we are aware of them.

It may be even more important to use colleagues and/or panels institutionally as independent checks and/or sources of advice.

Experience, knowledge and personal qualities come together to formulate choices. The question is whether the right options have been brought forward for consideration, particularly for the most contentious areas of the accounts.

It’s important to seek out comparators where possible and to check for unintended consequences.

And finally, for those taking decisions in preparation, rather than only needing to form an opinion…

Awareness of the issues on taking action, for example, on the timing of closing. As a preparer, there is the need to anticipate reactions to the choices made.

How are big-name corporates handling this?

There have been many different approaches to forecasts. For example:

National Grid had a single estimate of the financial effect.

Shell took a three-year timescale with estimates of prices per barrel in each.

Vodafone widened its assumptions from plus or minus 2% to plus or minus 5%.

Next gave three possible numbers covering the next year by quarter, explaining that it was using the middle one.

HSBC also had three – mild, moderate and severe – and said that it was “giving greater weighting to the mild and moderate scenarios”.

In its current guidance to companies in preparing the accounts, PwC uses the term ‘management should consider’ 21 times.

As we know, for ‘should’, read ‘must’.

The onus is indeed firmly on the management. And it doesn’t end with the end of lockdown – there is the transition into the post-COVID-19 world, adjusting the risk profile and (even) taking advantage of any opportunities that arise.

Just how credible is the story for getting out of lockdown?

A couple of red flags:

One is a statement that it’s just too difficult to make an estimate. That is not enough. Those compiling the accounts must be using some estimates. Why are we not being told what they are?

The second is the absence of a change in objectives, or at least the timescale to achieve them. There are few companies that do not need to reassess their plans in the light of COVID-19, and there has to be a plausible reason if they haven’t.

Anyone looking at the 2020 accounts without looking at the judgements involved is being as sensible as treating a virus without protective equipment. I rest my case.

Financial Reporting Council – Covid-19 Thematic Review: Review of Financial Reporting Effects of Covid-19 (July 2020)

Professor Likierman – details of the judgement framework are in ‘The Elements of Good Judgement’, Harvard Business Review (January 2020)

Andrew Likierman is professor of management practice and former dean of the London Business School

This article was taken from the October/November 2020 issue of The Treasurer magazine.