Key performance indicators (KPIs) have been used as management science tools for many years, providing objective measurements of the results of important business processes.

KPI adoption has accelerated in corporate treasuries in the aftermath of the global financial crisis. Boards of directors and other stakeholders, such as investors and industry analysts, increasingly seek dependable measurements of treasury activities, such as a company’s evolving cash position, its funding situation and the status of its financial risk exposure management. KPI adoption provides a powerful and effective analytical extension to treasury’s management reporting output, to give objective insight into treasury’s performance. So selecting the right set of treasury KPIs contributes directly to enhancing the quality of treasury management.

Twenty-first-century treasuries are, overwhelmingly, organised as cost centres that add value by providing treasury services to the organisation. These services include cash and liquidity management, funding management, treasury risk management and regulatory risk management, all of which can cause severe problems if not properly performed.

In practice, treasury KPIs are probably best set by the treasury team itself, as they are the experts in a complex and technical professional discipline. It is essential to have the KPIs endorsed by all stakeholders, including the finance director, the board of directors, and even shareholders, auditors and analysts – and the treasury team itself.

A possible approach is to survey all interested parties, to understand their priorities for measuring the results of different treasury activities. The group treasurer must be happy with the chosen KPI set. After all, he or she will be responsible for implementing the KPIs and for generating the resultant management reporting. If the whole treasury team embraces the KPIs, they can help a group treasurer’s efforts to deliver a treasury process improvement project. If the KPIs are realistic and are linked to relevant goals, they can really help the treasurer’s efforts towards achieving best practice.

It is essential to adopt a practical number of treasury KPIs – if you try to deliver too many, it’s unlikely the results will be used effectively, and the improvement project will lose commitment, momentum and direction.

The optimum KPI set for a given treasury is dependent on multiple factors, most notably the commercial nature of the business, including business structures and cyclical patterns, and the scale of corporate leverage or surplus. A highly leveraged domestic utility company, for example, will require a rather different set of KPIs compared with a cash-rich export company that has a high proportion of foreign currency revenues. There are some obvious business sector differences, given the high level of variation in the cash, financing and investment patterns that are found in practice, for example, in the contrasting situations of energy companies, airlines, advertising agencies and retail enterprises.

So the selection process should reflect corporate organisation and stakeholder priorities – and the results should translate into a KPI policy that will be relevant and effective for the industry and for the specific company’s condition – and which will be enthusiastically supported by all.

A recent (Q3 2011) survey of international treasurers conducted by IT2 Treasury Solutions indicates that a significant proportion (68%) of the responding organisations is already using a treasury KPI programme – or has plans to implement one over the next three years.

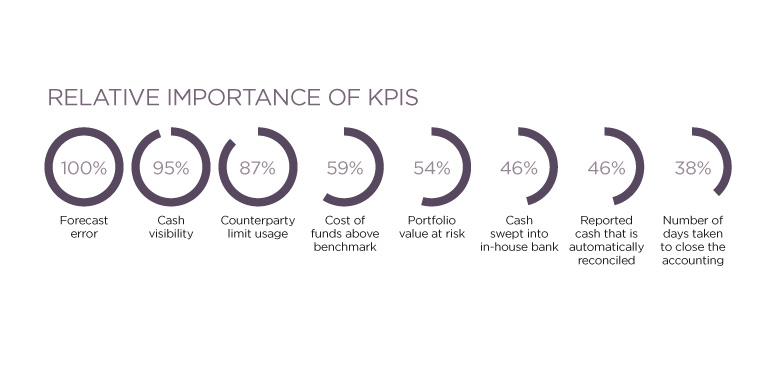

The survey asked treasurers to define the relative importance of different KPIs; among the survey respondents, the most popular KPIs relate to cash forecast error rates, cash visibility and level of counterparty limit usage – as illustrated on the previous page.

This article is supplemented with a table in which 10 important treasury KPIs are identified (see 10 important treasury KPIs). These are KPIs that are presently proving their practical value in optimising treasury operations.

Clearly, the KPI examples given here require a substantial and robust data collection, retention and analysis effort to translate them into dependable results that can be confidently reported to management, and that can be used as a basis to monitor and manage treasury improvement. So treasurers should look to their treasury management system to provide the required tracking and reporting facilities.

It is probably not advisable to keep changing the KPI set being used, as this would make it difficult to build up a robust set of statistics for effective benchmarking, and would probably be an unpopular complication for the treasury team. An annual review cycle should be considered.

We have seen how the demands of the global financial crisis catalysed the adoption of treasury KPIs. The KPI examples quoted here reflect some of the current priorities for the treasury industry, in the measurement and management of cash, funding, financial risk and corporate governance. Experience suggests that economic and market volatility will be the normal situation for the foreseeable future, and that a broad set of KPIs linked to liquidity, funding, financial risk management and best practice corporate governance will continue to be needed.

KPI management solutions should be sufficiently flexible to satisfy future shifts in demand for a particular category of KPI.

Some treasurers may feel concerned that the introduction of KPIs could have an adverse effect on the morale of their team. They might see it as a ‘Big Brother’ tactic, adding to the stress of a demanding treasury role by setting up and monitoring personal targets that may or may not in practice be reasonable – or useful.

Successful KPI programmes are invariably introduced sensitively, with emphasis on their underlying purpose being the strategic improvement of treasury operations through measuring the outcomes of treasury processes – not on micro-managing individuals. The KPI programme is best designed collaboratively, with all members of the team determining which KPIs are most relevant to the specific needs of their treasury environment – and which are most valuable in support of the evolution of treasury.

Paul Higdon is chief technology officer at IT2 Treasury Solutions.