It won’t have escaped anyone that market turbulence has increased substantially, with the treasury function playing a critical risk management role.

The importance of clear, consistent communication with debt markets has become paramount as companies seek to ensure liquidity and funding; and, importantly, also to reassure investors and underpin confidence.

This article sets out the background of the investor relations (IR) function, where it sits within debt markets – and what corporates must think about when they are looking to create a well-managed debt IR system.

IR as a profession developed initially in the US capital markets and provided the interface between US corporates and their institutional equity holders. Over the past 30 years, IR has become an established function globally, although with differing levels of maturity.

IR also reflects the specific structures of local financial markets. For example, the IR profession in the UK reflects the distinctive UK tradition of a corporate broker also providing market intelligence and advice to the CEO. In contrast, in Germany IR teams tend to carry out more activities in-house.

Debt IR was much slower to evolve than equity IR for a number of reasons. While companies have cared deeply who is holding their equity, the relationship with debt investors was more distant.

Traditionally, the reporting requirements associated with servicing debt investors have been less onerous than with equity investors, and debt investors were also historically less demanding than their equity counterparts.

The IR function is ideally positioned to take on the task of crafting the corporate investment case

The financial crisis of 2007/8 brought about profound change here. The systemic pressures focused attention on access to liquidity, and the subsequent low interest rate environment made debt funding attractive, in particular for strong corporate names.

Since 2008, the majority of large quoted and some unquoted companies have established a debt IR capability. The requirement for the banking system to substantially increase levels of capital adequacy has driven very high issuance levels in the banking sector. As a consequence, the specialist skills and expertise associated with debt IR are increasingly recognised.

The financial crisis also led to increased disintermediation of the banks and encouragement for issuers to engage more directly with investors. The distrust of complex financial instruments and push to move this trading on to exchanges also increases the requirements for effective debt IR.

Regulation of the financial services industry continues to have an impact on IR even if IR is not the main focus of this regulation.

For example, MiFID II Directives will apply in all EU member states in January 2018, furthering the sweeping regulatory reform represented by the original MiFID. MiFID II’s extension of the principles of open and transparent trading to all asset classes may impact the role of the debt IR function.

While in the UK there is a lack of visibility at present surrounding the extent to which future EU regulations will apply in the UK after Brexit, we assume UK and European market practice will continue to converge.

Moreover, the extreme levels of uncertainty generated by Brexit and a tumultuous 2016 US presidential election has made markets jittery. Strong communication skills become all the more important.

With all that in mind, here are the points that treasurers must consider when setting up a debt IR function.

As a working definition, IR is the corporate function that provides investors with the information they require to make investment decisions. It is also involved in the identification of new investors and subsequent outreach.

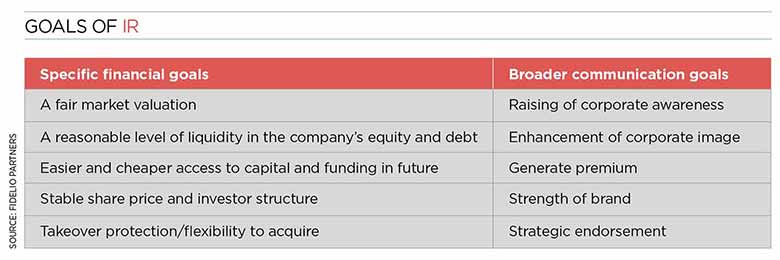

IR (both equity and debt) clearly has financial goals related to a fair valuation. There are also broader reputational benefits of an effective IR programme, which are set out below.

Clearly, the debt IR function is established to service the requirements of fixed-income investors. The rise in populism and anti-business sentiment since the financial crisis means that there is now greater awareness of the range of stakeholders that are critical for any business and also how these stakeholder groups interact and are relevant for valuation.

Communication with investors must be within the appropriate disclosure requirements. Communication to various stakeholder groups must also be consistent. It is certain that discrepancies between what is communicated to debt and equity investors will be rapidly identified by the market.

A debt IR officer must also be sensitive to the impact that communication to investors may have on employees or customers, for example.

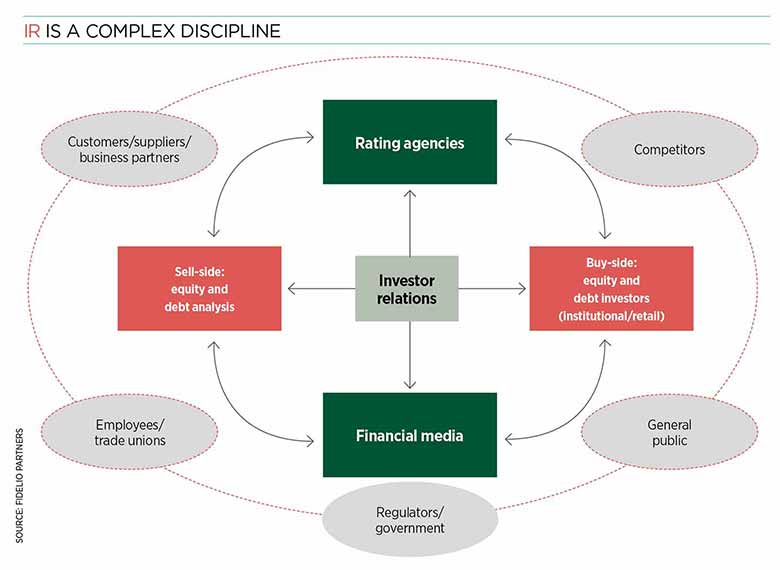

Experienced CFOs and treasurers recognise that, for a large quoted corporate in particular, there are multiple points of contact with the capital markets. It is important to ensure consistency of message across all investor groups.

The simplest way of achieving this is for one team to be tasked with producing the core investment message. This material will then be used as the key building block for all communication with key investor groups, especially:

The IR function is ideally positioned to take on the task of crafting the corporate investment case. This also serves an important compliance requirement helping to ensure proper disclosure, in particular around sensitive topics, such as corporate outlook.

There is no hard and fast rule as to what size of funding programme warrants a dedicated debt IR function.

For companies that are infrequent issuers, it is typical and most economical for the treasurer and treasury team to manage the issuance process and also to act as the point of contact for investors.

For more frequent issuers, however, two key questions need to be addressed:

If the answer to either question is yes, then the treasurer should consider a debt IR function.

Frequently, debt IR will be established within an existing equity IR function. A debt IR programme must have the technical expertise to address the specific questions of fixed-income investors relating to the instruments that they have invested in.

There are also some strong elements of similarity between debt and equity IR. Investors have an interest in the health of the company. Therefore, both debt and equity IR must present an investment case for the company and not just the underlying securities.

Thoughtful investors will be interested in the overall capital and funding structure of the company, as well as its strategy and outlook.

If skills, experience and processes are already in place to service equity investors, the treasurer should look to equity IR as a starting point and avoid reinventing the wheel.

When structuring a debt IR function, it is helpful to have a clear understanding of the deliverables:

Based on the above criteria, the treasurer establishing a debt IR function should look for the following skills:

The structure of the debt IR function is clearly company specific.

Regardless of the reporting line, debt IR requires very substantial input from the treasurer and the treasury function. So there needs to be a dotted reporting line or at least a very open and effective relationship between debt IR and treasury.

This works most smoothly when IR and treasury are both part of the finance function. When IR sits within the communications or corporate affairs function, at times the flow of information with colleagues in the finance function can be more problematic, and more thought needs to be given to promote cooperation.

A typical division of labour between debt IR and treasury is as follows:

That third point is easily achieved if IR sits within the treasury function and is therefore an extension of corporate finance and funding. However, in cases where IR sits outside treasury, the situation will be more problematic. Few treasurers would want to see the relationship between their organisation and its rating agencies being run from outside treasury.

In larger corporates we are also seeing evidence of increasingly structured cooperation between treasury, debt IR and corporate finance.

This recognises that all three functions have distinct contributions to make.

Just as diversity matters in the boardroom, it matters for IR.

Shareholders care increasingly about the composition of the board and of employees. If diversity matters to investors, it should also matter to IR directors. Treasurers should be conscious of encouraging diversity when structuring the debt IR function.

It is very visible and, importantly, also contributes to the pipeline of tomorrow’s treasurers and CFOs.

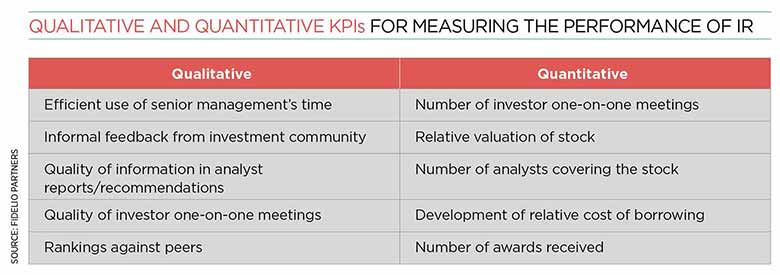

A treasurer establishing a debt IR function should rightly be concerned about how to measure success. However, a roster of key performance indicators (KPIs) has been developed for equity IR, which we consider to be broadly applicable to debt IR and which we set out above.

The KPI relating to stock performance can be replaced by metrics relating to maintaining the attractiveness of the corporate’s debt in the market. The other metrics shown in the table offer a simple method of monitoring performance and provide relevant tools for promoting effective and professional debt IR.

Debt IR has now become an established profession. Success will be determined by the ability of the debt IR officer to service existing investors, source new investors and potentially new pools of funding and, at the same time, contribute to an increase in stakeholder value. There is clearly much to play for.

Gillian Karran-Cumberlege is founding partner at Fidelio Partners board development and executive search consultancy.

This article was taken from the February 2017 issue of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership