In the space of a few short months, the subject of central bank digital currencies (CBDCs) has moved from an academic abstraction to an important question in central bank boardrooms around the world.

In addition to looking for a response to Libra, the digital currency proposed by Facebook, the practicalities of rapidly distributing cash to citizens as part of government responses to a pandemic have made the introduction of CBDCs a strong likelihood. The key question is not ‘if’, but ‘when and where’ a CBDC will be introduced.

According to Impending Arrival, a recent report from the Bank for International Settlements (BIS), 80% of the world’s central banks are working on launching their own digital currency. In addition, 10% of central banks had developed pilot projects, and banks that collectively represent 20% of the world’s population said they were likely to issue CBDCs in the next few years.

So, what are CBDCs and how do they affect treasurers, if at all?

There is no common definition of a CBDC, as the term refers to a range of possible designs and policy choices. It is a concept that brings together computer science, cryptography, payments systems, banking, monetary policy and financial stability.

The Bank of England defines a CBDC as an electronic, fiat liability that can be used to settle payments or as a store of value. It is in essence electronic central bank, or ‘narrow’, money.

Most treasurers will be familiar with the concept of electronic money, since they process large-value payments to support borrowings, investments and currency transactions. The main area of innovation would be for the retail market.

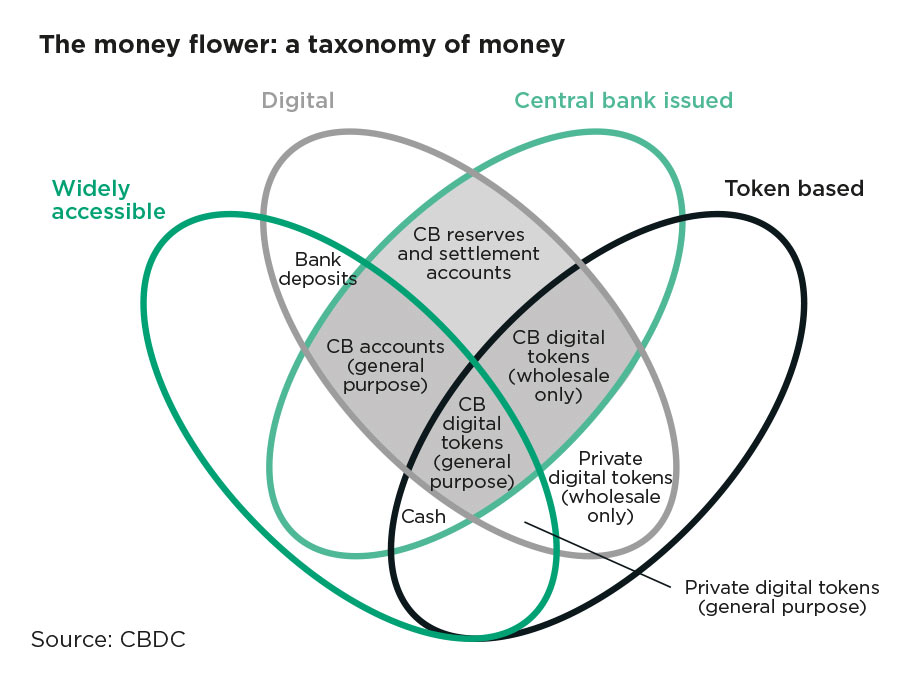

CBDCs can share many of the same characteristics of existing examples of money, as the following diagram shows.

Money is typically based on one of two basic technologies: tokens of stored value or accounts. Cash and many digital currencies are token based, whereas balances in reserve accounts and most forms of commercial bank money are account based. Token-based money relies on the ability of the payee to verify the validity of the payment object (for example, the coin) and to avoid counterfeits (or in the digital world identify whether the token has already been spent).

Account money depends on the ability to verify the identity of the account holder, and here a key concern is identity theft, which allows perpetrators to transfer or withdraw money from accounts without permission.

Digital central bank money is at the centre of the money flower. The taxonomy distinguishes between three forms of CBDCs (the dark-grey shaded area in the diagram). Two forms are token based and the other is account based. The two token-based versions differ by who has access – the wholesale or the retail market. In the account-based version the central bank provides general-purpose accounts to all participants.

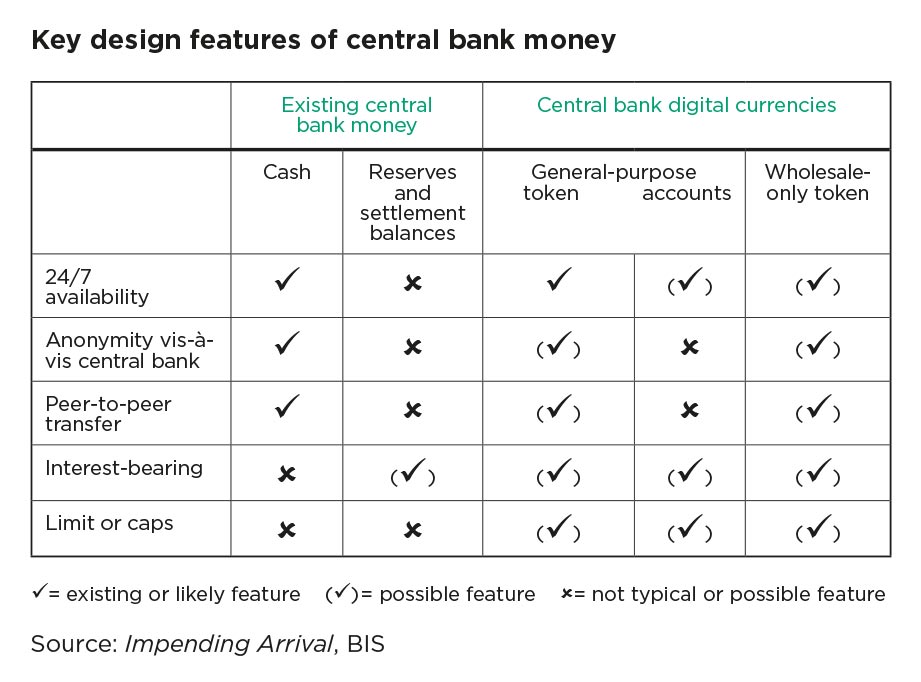

In its report the BIS lists five key components that central banks will need to consider when designing their own CBDC.

The table below provides a comparison between CBDCs and existing central bank money.

CBDCs are expected to be fundamentally different to cryptocurrencies or cryptoassets, such as Bitcoin. Most cryptoassets are privately issued and are not considered money because they are:

Some privately issued cryptoassets, known as ‘stablecoins’ (such as Libra), aim to provide stability by backing the coin with one or a basket of assets (such as market-traded currencies). However, there have been issues over the collateral backing stablecoins with problems at Tether being an example of the effects of a lack of transparency.

The UK CBDC would represent a new risk-free form of digital sterling, issued by the Bank of England and therefore performing all the essential functions of money without increasing any of the risks associated with other cryptoassets.

Central banks have been looking into CBDCs to achieve the following:

At the moment, CBDCs remain, like blockchain, more of a concept rather than a reality. However, the fact that the European Central Bank, Bank of France, People’s Bank of China and Bank of England to name but a few are all looking into it means that treasurers should at least be aware of the topic.

Significant sums are being invested by both the private as well as the public sector, as the current costs of running physical currency is high. The Bank of Korea spent approximately £40m on producing coins in 2016.

As the number of different stablecoins increases and as central banks move from proof of concepts to actual delivery, treasurers will need to understand these new currencies and assess the benefits to their business, their customers and their suppliers, and determine the impact on their own payment, accounting and reconciliation systems and processes. The lead time to implementing many of these changes is long. Nevertheless, treasurers should add CBDCs to their horizon-scanning activities now.

Naresh Aggarwal is director – policy and technical at The Association of Corporate Treasurers

This article was taken from the August/September 2020 issue of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership