We last wrote on group financing in June 2014. This refresher considers structural subordination, the use of funding secured on specific assets, and the difficulty of maintaining optimal models. We also consider part-owned subsidiaries.

The above is not unusual. At FTSE100 stage of growth, several pages of A3 paper may be required if brave enough to try a printout of the corporate structure, let alone the funding structure.

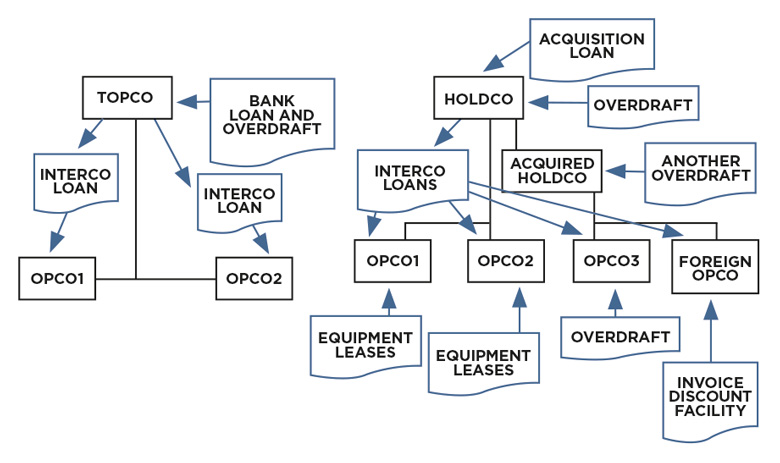

There are two optimal approaches to funding a group, although maintaining either is usually impossible. The first model is where all external borrowing is unsecured and is through the top company or topco, which funds the remainder of the group with intragroup loans and equity. The lender, or syndicate, relies on exclusive access to the group’s assets in the event of default.

The alternate is that the top company funds partly with equity, and each group company obtains its own external funding. Intragroup loans may also be made. Each external lender relies on the borrower company’s assets for security. This is known as structural subordination: the lower-level borrower has better rights to subsidiaries’ assets than a higher-level borrower.

The first model will attract a lower cost of credit, because no lender has a call over the assets of a subsidiary. The cost goes up as the sources of finance become more diverse.

The reason optimal models are often not achievable is that businesses may need to accept whatever funding they can as they grow, and usually develop a portfolio of secured asset funding, unsecured bank loans and sometimes shareholder loans. Acquired subsidiaries may come with debt. It is for these reasons that some groups occasionally resort to complete refinancing as they grow.

In the long run, a growing group may want to move to the top-down funding model because unsecured, cost-effective bond finance is more likely to be available to the topco with minimal structural subordination. The choice is not simply a matter of pursuing the cheapest and most flexible form of funding. The group needs to consider not only the preferences of lenders, but local regulation, withholding tax and its funding strategy.

Structural subordination can be further complicated if lenders seek topco parent company guarantees (PCGs) that push the liability up to the top company. While this often makes financing more readily available, it does not necessarily reduce the credit margin to that of the topco, while increasing the legal complexity of the group. This is the reason why subsidiary funding is often secured by physical assets or receivables.

A 100% group operating wholly within one country can easily move funds around the group by means of intragroup loans and the use of bank notional pools. Many groups operate across borders. Governments will be wary of intragroup loans that cross borders, and may apply thin capitalisation rules to try to stop such loans being used to distribute capital by means of loan repayments.

It is not unusual for external auditors to be required to sign off the borrower’s ability to repay an intragroup loan. This can be a barrier to efficient cash management because it slows down the process of using surplus cash and can lead to blocked cash.

It is not unusual for an acquired subsidiary to come with a minority interest, which is retained by the vendor, whose rights to capital distributions must be respected. This will require similar due diligence to that required for intragroup loans to offshore subsidiaries.

Capital market lenders, for example the bond markets, offer simpler terms and covenants than bank lenders and lend unsecured. (Some bonds are issued as debentures and the lender is preferred over unsecured lenders in the event of insolvency.) This becomes an attractive alternative to bank-based lending, which is becoming less attractive and more expensive as banks digest post global financial crisis (GFC) banking regulation. Bond markets also prefer to lend to the company of a group that holds the main physical assets of a group, but will lend to top holding companies, providing there is little or no structural subordination.

As a group grows, it may progress from bank and lease borrowing to a mix of bank and capital markets borrowing. Structural subordination will be reflected in the credit margins of the borrowers. Simple funding structures may achieve lower funding costs. They will also enable ready visibility to a centralised treasury and reduce the risk of inadvertently triggering defaults.

Steve Baseby is a former executive director in policy & technical at the ACT