There has been a flurry of activity from the UK Payment Systems Regulator (PSR) over the summer and two areas may be of particular interest to treasurers: commercial uses of payment data and reimbursement in the event of payment scams.

During the summer, the PSR launched a discussion paper to examine how commercial uses of payment data might affect the payments industry, businesses and consumers, and to gain a better understanding of the resulting opportunities and risks.

Traditionally, the value of payment data has been ignored due to the rigidity of the payments landscape in the UK, and indeed across the globe. However, one of the outcomes of the Open Banking initiative and the resulting growth in competition will be greater flexibility and choice brought about through a change in how payments and their associated data are exchanged.

Initial work by the PSR noted that an increase in the collection, analysis and sharing of payments data could drive innovation, resulting in more payment products and services being available to end users. However, there was also a concern that end users could receive a reduced range or quality of services as companies look for competitive advantage and target their products.

Furthermore, having witnessed how customer data has been misused, the regulator is keen to understand the implications of increased commercial use of payments data for end users in terms of privacy, data protection and product choice.

The PSR discussion paper is focusing on three areas:

Not a code on how to undertake a scam, but an announcement by Authorised Push Payment (APP) Scams Steering Group, established by the PSR earlier this year.

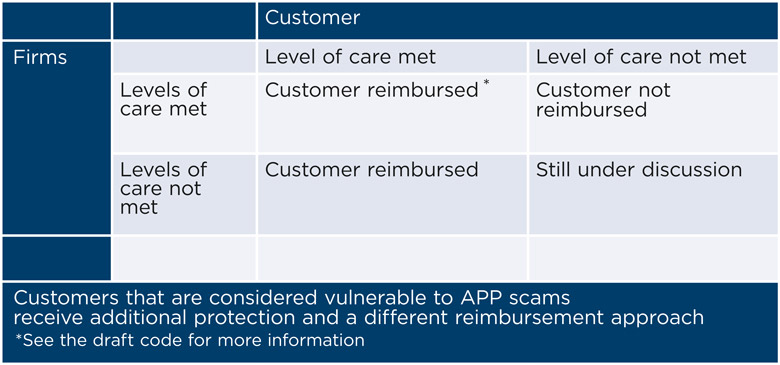

The APP released its consultation paper in September – Draft Contingent Reimbursement Model Code.

The key principle of the code is to consider under what circumstances customers can be expected to be reimbursed following a fraudulent event. This focuses on the levels of care applied by the relevant parties.

Source

Where a customer has met their requisite level of care, the Steering Group expects them to be reimbursed. However, where the firm involved in the payment journey has met its own level of care, the Steering Group is still working out who should meet the cost of reimbursements in these situations.

Naresh Aggarwal is associate director, policy & technical, at the ACT