What do long-only funds want?

What do convertible arbitrage funds look for?

What do both groups want?

I have heard a number of treasurers and CFOs joke that a banker will happily tell you whether or not it is possible to issue a convertible, but if they believe that you can, they will almost always also tell you that you should. So how can a company identify the right time to issue a convertible? And what are the elements that make for a good opportunity in this market?

First, let’s think about who buys convertible bonds and what drives their investment decisions. The first group are the ‘long-only’ or ‘outright’ funds, which buy convertibles because the combination of downside protection and upside exposure appeals to their investors. The second are the convertible arbitrage funds, which buy convertibles based more on technical factors, and which actively hedge the share price exposure (and possibly the credit exposure as well). These two groups are currently of similar importance and size.

The box [Investor considerations when buying convertibles] provides a rundown of the features each group cares about when looking at a convertible.

In short, the ‘perfect’ issuer for a convertible bond should be a large company, looking to raise $500m or more, with a strong credit rating, a volatile stock price, no dividend and a strong stock story.

But can this really be correct? Such an issuer would meet many of the criteria desired by a convertible arbitrage fund, but would probably pay a very low coupon, and also insist on a high conversion premium (the amount by which the conversion price exceeds the stock price when the bonds are issued).

In fact, what you find in practice is that investors (especially outrights) would often prefer a company with a slightly weaker credit rating, and which pays a 2-3% dividend yield, such that the convertible they issue will actually pay some coupon and have a more moderate premium (say 25-30% above the stock price). In practice, we see that the convertible market is frequently used by small- to mid-cap issuers, often those who have less access to other bond markets and may be unrated.

For an issuer, different considerations come into play when deciding whether the timing is right for a convertible:

In other words, as an issuer, the ideal timing to issue a convertible is when either (a) the absolute terms are very appealing (high prevailing share price, high conversion premium, low coupon) or (b) the relative pricing (compared with issuing equity or debt) makes a convertible attractive for the issuer.

The question of ‘absolute’ terms is relatively easy to analyse. If the stock is strong, the company needs money and the coupon is attractive (ie low), then it is probably a good time to seriously consider issuing a convertible. This is not driven by the strength of the convertible market (or how appealing the issuer is to convertible investors on any technical basis), but rather by the strength of the company. In some cases, issuers have been known to sell convertibles in such an environment even without a clear use of proceeds, just to lock in the terms.

For an issuer, different considerations come into play when deciding whether the timing is right for a convertible

However, it can be harder to identify when the terms are ‘relatively’ appealing, so I like to think about the potential all-in costs of various financing tools to decide when a convertible can make the most sense relative to alternatives.

As an issuer, consider three options: (i) issue a non-convertible bond, (ii) issue new shares, or (iii) issue a convertible. In each case, think about the returns that the new investors will earn as being the ‘cost’ of the instrument to your current shareholders. (In the case of the bond and the convertible, it also makes sense to adjust these costs for the tax benefit to the company.)

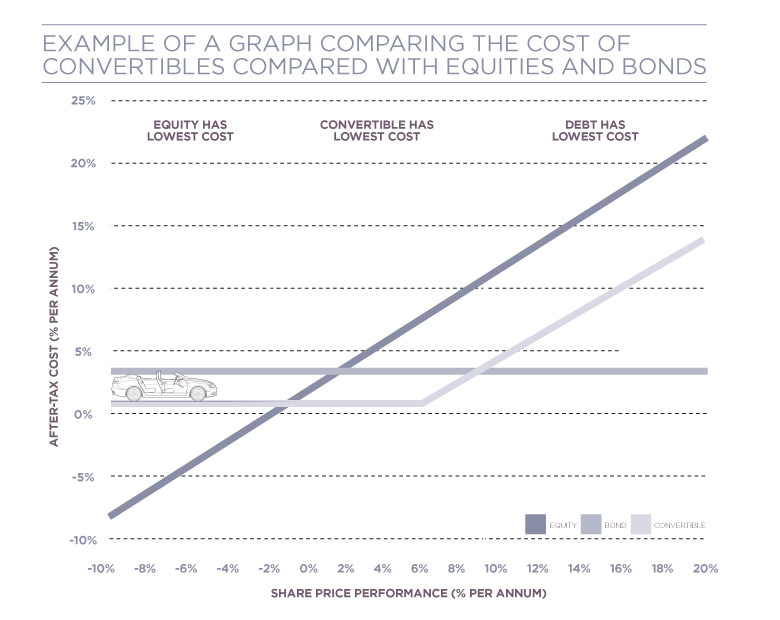

On a graph, plot the return that a new investor would earn against a range of potential future share price performances.

For equity, if you pay a 2% dividend yield, and the stock rises 10% per annum, the new shareholders will be making 12% per annum. If the stock falls 10% per annum, the new shareholders’ return will be -8%. (Equity is also likely to be sold at some discount to market, which we ignore here.)

For a bond, so long as the company is able to repay it at maturity, the share price does not impact on the total returns to investors. So, if the coupon were 5%, that will be the return to investors, and with a 30% tax rate, that becomes a 3.5% after-tax cost for the company.

Now, plot a convertible on the same graph. So long as the return to shareholders does not result in the stock price exceeding the conversion price, the bonds will not convert, and the cost is simply the coupon less the tax shield (which in many jurisdictions is based on the issuer’s normal cost of debt, not the coupon). So for a company that might pay a 5% coupon on straight debt, and would pay a 2% coupon on a convertible, the after-tax cost ends up around 0.5%. If the share price performs strongly and the bonds do end up converting, the stock price still needs to go quite a bit higher than the conversion price before the all-in cost exceeds that of non-convertible debt. In this example, a convertible with a 35% premium actually needs the stock to rise by 9.5%pa (a return to shareholders of 11.5%pa) before the convertible has a higher cost than straight debt.

The chart [below] shows this example. What you can see is that if the share price falls, equity will be the ‘cheapest’ financing tool. If it rises materially, straight debt will be cheapest. However, if the stock has a modest positive performance, the convertible will be cheapest. For an issuer, then, the time to consider issuing a convertible due to its ‘relative’ appeal is when there is the greatest range of potential share prices in which the convertible will be the ‘cheapest’ source of financing for the transaction.

So when will this be at its greatest? Clearly, the more appealing a new convertible is to the widest group of investors, the better the terms (coupon saving and conversion premium) that can be achieved. If this also coincides with a time when the ‘absolute’ terms are appealing, it is probably the right time to think seriously about a convertible.

A bond that can be converted into a predetermined amount of the company’s equity at certain times during its life, usually at the discretion of the bondholder. Source: Investopedia

Mark Dalton is the founder of Conv-Ex, an independent advisory firm specialising in convertibles and equity derivatives.

E: dalton@conv-ex.com

W: www.conv-ex.com