With IFRS 16 fast closing in, treasury departments may soon be asked to provide incremental borrowing rates for calculating lease assets and liabilities under the new standard.

The new standard states that lease payments shall be discounted using the interest rate implicit in the lease, if that rate can be readily determined, or the lessee’s incremental borrowing rate, if not.

Interest rate implicit in the lease is the rate of interest that causes the present value of lease payments and the unguaranteed residual value to equal the sum of the fair value of the underlying asset, and any initial direct costs of the lessor.

It is therefore based on lessor cash flows arising from the lease transaction; it does not depend on lessee borrowing rates.

For many leases, however, the implicit interest rate will not be readily determinable, for example, if the lessee does not have a reliable estimate of the residual value of the leased asset.

Also, lessees applying the modified retrospective approach to transition are required to discount lease payments with incremental borrowing rates as at the date of initial application (1 January 2019 for lessees with December year ends).

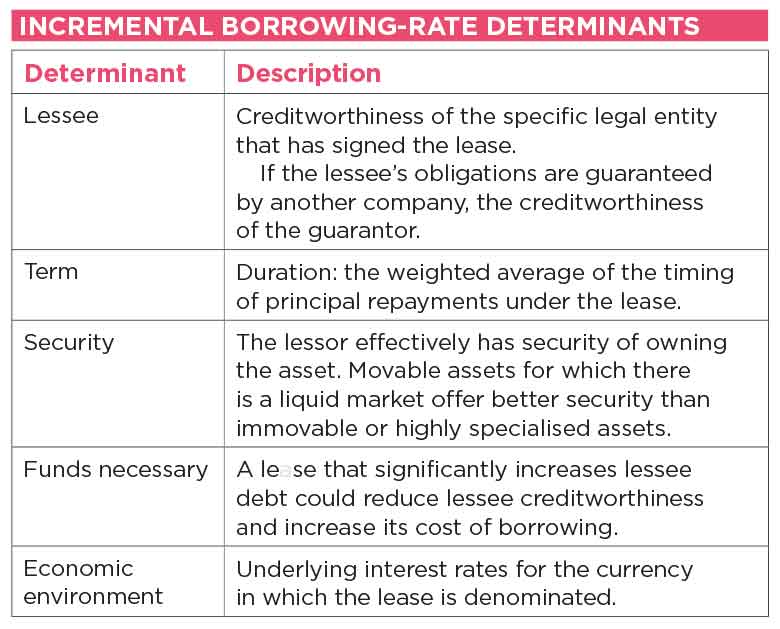

IFRS 16 defines the lessee’s incremental borrowing rate (IBR) as “The rate of interest that a lessee would have to pay to borrow over a similar term, and with a similar security, the funds necessary to obtain an asset of similar value to the right-of-use assets in a similar economic environment”.

The various elements of this definition are set out in the table below, and they should all be reflected in the IBR calculation.

For example, if a group’s Egyptian subsidiary were to enter into a 10-year lease, in Egyptian pounds, of an aircraft, the IBR would be the rate of interest on a loan in the amount of the lease right-of-use asset, to a company of the same creditworthiness as the subsidiary (taking into account the liability arising from the new lease), for the duration of the lease, in Egyptian pounds and with the aircraft as security.

Even if such a loan were to exist, details such as the rate of interest are unlikely to be publicly available.

In this case, and indeed in many cases, lessees will have to use best efforts to derive an interest rate based on the information available to them.

For the majority of leases, principal is repaid over the course of the lease, and so the lease duration is shorter than the lease term. The ratio of duration to term depends on the number and timing of rental payments and increases with interest rate as higher interest charges delay repayment.

For example, a 10-year lease with quarterly payments in arrears and an annual interest rate of 5% would have a duration of 5.5 years.

The interrelation with interest rates introduces an element of circularity, which can be dealt with by calculating the duration and the corresponding IBR for a range of interest rates, and then selecting the IBR, which rounds to the corresponding interest rate assumption.

Companies that have a range of borrowing instruments in place of different durations can create their own IBR yield curve, specific to the currency of borrowing.

In many cases, the majority of debt will be issued or guaranteed by the ultimate parent company or a similarly creditworthy company within the group, and borrowing rates will reflect this.

Leases, however, may be entered into by companies across the group, and their incremental credit spreads will have to be factored in.

These may be estimated by deriving a notional credit rating for the lessee, based on the strength of its balance sheet (with the new lease taken into account) and the geographical location of its assets, and then using market-observed data, such as credit default swaps, for companies with the same credit rating.

For companies with large lease liabilities, discount-rate assumptions will have a significant effect on amounts recognised in financial statements and so may require disclosure

For companies with little or no debt (and for leases denominated in currencies other than the group’s borrowing currencies), lessee IBRs may be calculated on the basis of published reference rates for the relevant currency, such as government borrowing rates or Libor, adjusted for the relative creditworthiness of the lessee.

In some cases, lease-by-lease analysis supported by specialist banking advice may be required, for example, to take account of any impact on the IBR of the lessor having security in the form of ownership of the leased asset.

Auditors may be prepared, however, to accept a methodology for deriving IBRs for the majority of leases based on existing processes for calculating group cost of debt and intercompany borrowing margins.

Standing data used to calculate IBRs will need to be updated at least annually and in the event of a significant change to the company or subsidiary creditworthiness (including a change to credit rating).

IFRS 16 states that lease liabilities shall be recalculated if there is a change in an index or rate used to calculate the leases payments.

If the recalculation arises because floating interest rates have changed, the lessee should use a revised discount rate, based on the new interest rates.

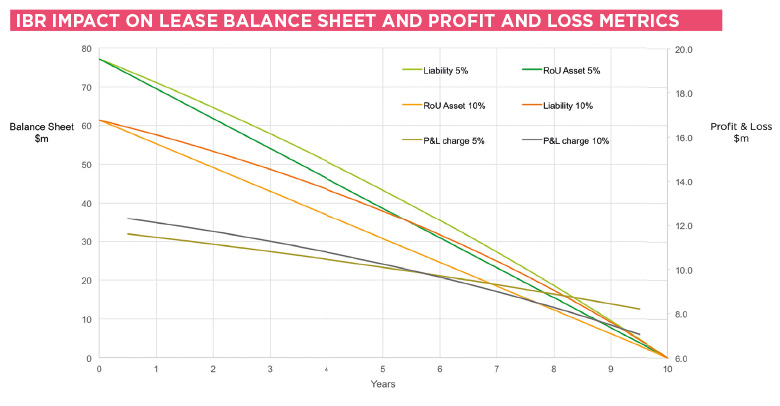

Right of Use asset, lease liability, interest expense and depreciation for a 10-year lease with annual payments in arrears of $10m, discounted at IBRs of 5% and 10% are shown in the diagram below.

Using a higher IBR decreases the asset, liability and depreciation, and increases interest expense.

The total profit and loss (P&L) impact always equals $100m (the sum of the lease rentals), but the front-loading of the P&L charge increases with IBR and interest expense.

On transition to the new standard, IFRS 16 states that lessees adopting the modified retrospective approach shall disclose the weighted average IBR used to calculate lease liabilities at the date of initial application and reconcile this against lease commitments disclosed under the current standard, discounted at the same rate.

For companies with large lease liabilities, discount-rate assumptions will have a significant effect on amounts recognised in financial statements and so may require disclosure.

In any event, audit committees and external auditors will seek assurance that robust processes are in place for determining lease discount rates.

Henry Wilson MCT is a manager in structured finance at BP

This article was taken from the Feb/Mar issue of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership