The UK government appears to be on a pathway to amend the underlying calculation of the retail price index (RPI), to bring the measure into line with the consumer price index, including owner occupiers’ housing costs (CPIH) between 2025 and 2030. This would reduce the expected future change in RPI by around 1% per annum.

This change would have significant and immediate financial consequences.

For any organisation with income or expenses linked to RPI, the implications could be significant – potentially both positive and negative. Significantly, the value of assets linked to future changes in RPI will suffer a meaningful fall. We estimate the proposed RPI reform could reduce the total value of the index-linked gilt market by around £90bn. RPI-linked assets with longer-dated income streams would suffer the most.

We believe the change would have a negative impact for many. We would encourage all stakeholders to engage now to shape the January 2020 consultation on the proposal, to submit a response to the consultation when it opens – and to make the case for an element of compensation to avoid unintentional wealth transfer.

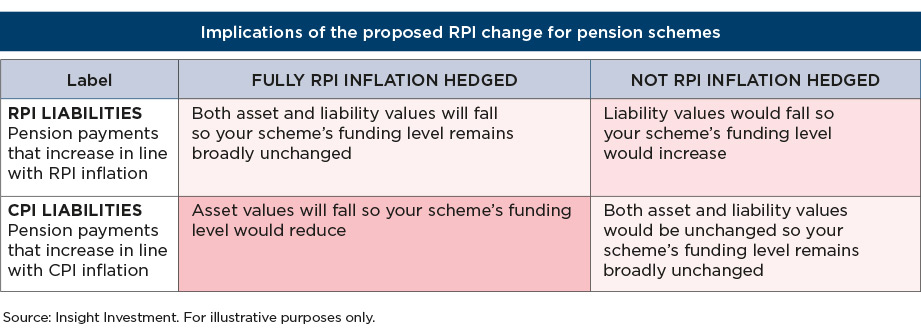

How the proposed change to RPI affects your organisation’s pension scheme will depend on the type of assets the scheme holds and the nature of its liabilities (see table, below).

Pension funds with CPI-linked liabilities who have taken prudent steps to hedge these liabilities using RPI-linked gilts will see their funding status deteriorate. RPI-linked assets are used because CPI-linked assets are in short supply; the total value of CPI-linked assets available is less than £10bn compared with the total value of RPI-linked bonds in issuance of around £700bn.

This change would come after many UK pension schemes have allocated significant portions of their assets to RPI-linked gilts – probably the biggest single shift in pension asset allocation made over the last 10 years – and significant purchases having being made after official reviews and consultations have concluded that RPI would not be amended.

The proportion of schemes that would benefit from the change is low, as most corporate UK schemes have hedged a significant portion of their inflation risk.

Some of the most significant impacts of changing RPI include the following:

We believe it would be wise for key stakeholders, including treasurers, to:

We urge all key stakeholders, including corporate and local government organisations, pension scheme trustees and members, and advisers and asset managers to engage with policymakers over the change.

In particular, we would also encourage you to engage in the debate over the possibility of a compensation formula for recipients of contractual RPI-linked payments to achieve an outcome that avoids an unintentional wealth transfer.

For more information on the issue, please see Insight’s in-depth white paper, Proposed changes to RPI: nobody needs to lose out. The paper can be viewed here.

Important information

Unless otherwise attributed, the views and opinions expressed are those of Insight Investment at the time of publication and are subject to change. This document may not be used for the purposes of an offer or solicitation to anyone in any jurisdiction in which such offer or solicitation is not authorised or to any person to whom it is unlawful to make such offer or solicitation. Insight does not provide tax or legal advice to its clients and all investors are strongly urged to seek professional advice regarding any potential strategy or investment. Issued by Insight Investment Management (Global) Limited. Registered office 160 Queen Victoria Street, London EC4V 4LA. Registered in England and Wales. Registered number 00827982. Authorised and regulated by the Financial Conduct Authority. FCA Firm reference number 119308. © 2019 Insight Investment. All rights reserved. IC1836

Jos Vermeulen is head of solution design at Insight Investment