The UK once again finds itself in choppy economic waters. A major global energy supply shock, surging inflation and rising interest rates have tipped the economy into a recession that will deepen over winter. It will be the second downturn in two years following the mega-recession during the COVID-19 pandemic in 2020. The new decade has not started well.

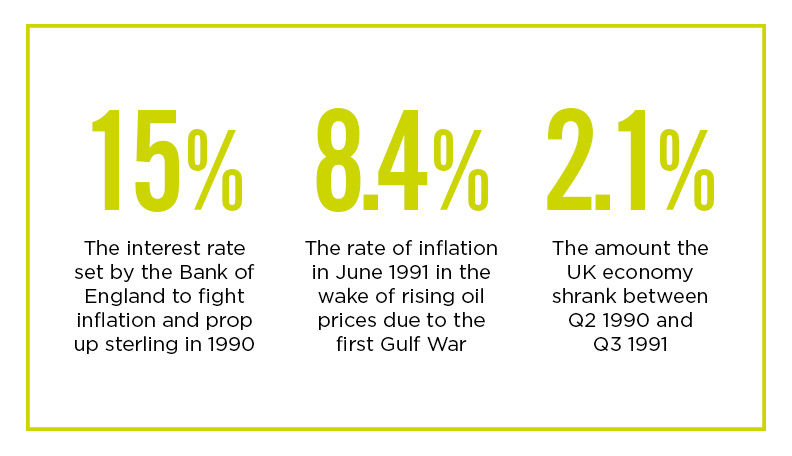

If any of the problems underlying the current turmoil sound familiar, they should. While the details differ, the UK suffered from a similar combination of challenges in the early 1990s. They produced a recession then, too. From Q2 1990 through to Q3 1991, the economy shrank by 2.1%.

Relative to previous recessions in the 1970s and 1980s, when GDP declined by 5% or more, the 1990s drop in output was modest. It was also much less severe than the approximate 6% plunge during the 2008 global financial crisis (GFC).

But was the 90s shock really less bad? That depends on how you measure it. If you focus just on output losses, which is standard for economists, then you might say yes. But when you ask people about the early 90s downturn, they recall bad memories that are in many cases worse than for the GFC.

The housing bubble that had been building in the previous years popped with a bang

Even though the overall drop in GDP was small, the economic troubles that came with the early 90s shock affected almost everyone in one way or another. Inflation surged from 5.7% in January 1990 to 8.4% in June 1991 as oil prices doubled in the wake of the first Gulf War. Inflation had already been building before the war on the back of excessive fiscal stimulus in the late 1980s.

Then, the Bank of England (BoE) lifted rates to nearly 15% in 1990 from 7.5% in the late 80s to stem the inflationary tide and to prop up sterling as part of the exchange rate mechanism. Surging mortgage rates and already high inflation hit household budgets. The housing bubble that had been building in the previous years popped with a bang.

Whereas the 2008 shock was terrible for people who were made unemployed, especially as many struggled to find new work for years afterwards, the personal circumstances of most people were less badly affected during the downturn than in the early 1990s. House prices fell by less. Inflation was much lower. Interest rates even declined sharply as central banks aggressively eased as soon as the troubles started.

In many respects today is comparable to the 1990s. Although the hit to GDP looks likely to be modest – probably around 2.0–2.5%, almost everyone will experience some kind of hardship.

The cost-of-living crisis, which is almost entirely due to Russia’s invasion of Ukraine, has pushed up global energy prices. The rise of inflation to 10% in the UK will cut real incomes by at least 5% this year for most households. On top of this, around half of households with a mortgage are at risk of seeing their interest costs triple.

Even though unemployment probably will not rise much – the 1990s recession and the GFC each put around one million people out of work – life has become harder for many millions.

Although the situation is bad now and may get worse, there is some room for hope. In one very important respect, it is good news that the setup is similar to 1990 and not 2008.

The GFC was borne out of years of worsening financial system fragility that became all too apparent when house prices started to correct in the UK and elsewhere from 2006 onwards.

The housing market had been built on sand during the 2000s boom. Too little capital in the banking sector. Too many risky loans. It was an accident waiting to happen.

The economic recovery that followed the GFC was painfully slow. Instead of lending and spending, banks were forced to build up capital and households had to pay down debt. This stripped growth momentum and resulted in a huge permanent loss of output from which the economy never fully recovered.

In the 1990s, however, the shock did not entail anything like the same degree of financial system turmoil or lasting economic damage. Largely because of a better fundamental starting position, the economy sprang back to life as soon as inflation and interest rates came down. Once the headwinds faded, the recession gave way to a long period of strong growth and rising prosperity.

The situation today is similar. UK banks have three and a half times more capital today than in 2007. Consumer credit as a percentage of incomes is near a 20-year low while households have excess savings worth some 8% of GDP sitting on their balance sheets. And 86% of all mortgage debt sits with the top 50% of households, who are at low risk from default as interest burdens rise. The UK faces a recession but not a financial crisis.

Once inflation starts to fall fast from early next year onwards, the BoE should be able to take its foot off the brake and lower interest rates somewhat during the second half of the year. As a best guess, the BoE bank rate will settle at around 3% once the current bout of high inflation passes. That would be no major obstacle to an economic expansion.

No question, the UK faces a serious economic situation. Beyond the ongoing fallout from Brexit, the outlook is clouded by the internal crisis within the government and policy risks that come with it. The uncertain outlook for the war in Ukraine adds an unpredictable international dimension to the course of the recession.

If the lights go out due to genuine energy shortages across Europe during winter, then comparisons to the 1970s may become appropriate. But, for now, that seems unlikely.

At any rate, things will be clearer by early next year. By then, with luck, we should be anticipating better times from spring onwards.

Kallum Pickering is senior economist at Berenberg Bank

This article was taken from Issue 4, 2022 of The Treasurer magazine. For more great insights, members can log in to view the full issue. If you're not an ACT member, you can sign up for eAffiliate membership