Recently, a public company reported a double-digit percentage decline in earnings mainly due to foreign exchange losses on operations. This is a recurring phenomenon with many large, sophisticated multinationals. These companies have well-established and board-approved policies aimed at curbing precisely such swings in earnings volatility. They are typically using a market standard approach to hedging operational FX risk that has been around for decades. Why is it then that public companies are still making these kinds of announcements?

The reason is that, often, currency fluctuations impact a company’s cash flow and earnings differently. Earnings at Risk (EaR) is a calculation of the possible deviation to earnings due to FX rate movements at a specified confidence level and over a time horizon, while Cash flow at Risk (CFaR) is a calculation of the possible deviation in expected cash flows due to FX rate movements over the same period. It is possible that hedging certain cash flows could negatively impact earnings at a group level.

Treasurers have liquidity objectives and are concerned about minimising cash flow volatility, while also managing FX risk. Thus, a treasurer’s hedging activity to accomplish their goals may be in direct conflict with the CFO’s objectives of delivering earning results that match their commitment to equity analysts. Managing only CFaR and ignoring EaR from a measurement and reporting perspective allows for an unknown movement in earnings due to FX rates in direct conflict with a board’s ability to effectively target an earnings per share (EPS) number they have advised to equity analysts and investors as a forecast.

A solution to this quandary that enables a more predictable earnings announcement, requires an understanding of this trade-off for each specific company, as well as the group entity. It requires adopting an optimisation strategy and choosing where along the spectrum of EaR vs CFaR a firm needs to be.

For example, a risk committee can adopt an approach with a maximum EaR target that has a 95% confidence level and leave the CFaR to be slightly higher than they may have tolerated in the past, to accommodate the group goal of less volatility to earnings due to FX rate movements.

The market standard for hedging FX is a simple percentage of exposure methodology, typically approved by the board and set into policy years ago. However, ask any board, CFO or treasurer for a rationale on why this percentage hedge is better than another and the answer is not particularly compelling.

This percentage hedging policy is often managed by treasury departments who receive monthly cash-flow forecasts from their business units. They apply a fixed minimum and maximum hedging percentage for the current financial year with rolling, usually lower, thresholds for subsequent years. This reduces cash-flow volatility and is generally considered best practice, accepted by auditors and boards alike.

The treasury department then executes these cash-flow hedges, often netting cash flows where practicable. The currency risk-management process is complete, and gross and net exposures are reported to the board. Currency risk discussions revolve around what is the right hedge percentage for a given currency or entity. A potentially more appropriate discussion should really be on how much EaR the board is willing to accept due to FX rate fluctuations.

Rather than managing to a hedging percentage, an alternative approach would be to manage both earnings and liquidity with a CFaR and EaR optimisation tool. Treasury departments will need to understand and identify all cash flows that can impact the FX gain or loss reported on the earnings statement, as well as those cash flows that impact the business units’ earnings and net cash flows.

An EaR target agreed with the board will change the way FX risk is managed by the treasury department. It will now need to identify all cash flows that will impact earnings and how it can mitigate it to comply with the board policy; the amount of CFaR remaining can then be reported using a risk model approach the board understands.

For a company with a good credit rating and low liquidity risk, very often our optimisation methodology will identify inefficiencies in the companies’ hedging strategy. This means that for the same level of CFaR you can lower your EaR by moving your hedges closer to an efficient frontier. Beyond the obvious improvements for the same CFaR, there are significant benefits to the organisation when the CFO and treasury offices consistently deliver within an agreed EaR number that the board understands and has approved.

Take, for example, a highly levered organisation. The typical approach of targeting lower EaR may increase the business unit level CFaR, thus impacting financial liquidity [at the business unit level]. If a company’s gearing is high or their credit rating is low, reducing liquidity risk from FX rate movements may be more prudent then targeting a lower EaR number.

Understanding the trade-off between hedging a business unit’s currency and liquidity risk and the group’s earnings means the discussion is no longer about arbitrary hedge percentages.

The discussion is about how much risk the board is willing to take on at the group earnings level and whether they can accept the requisite cash-flow impact at the business unit level from FX rate movements. Managing the trade-off between these risks is a key function of treasury, and now the board can enable it.

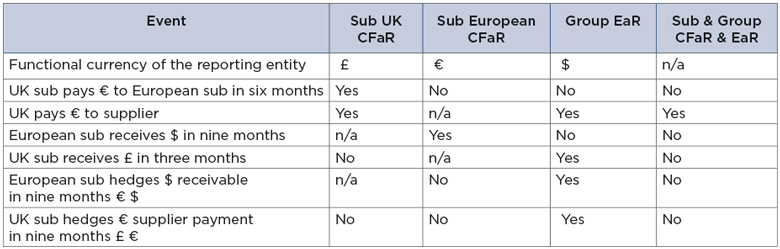

We begin by assuming that all cash flows are going to impact either group earnings or business unit earnings, or both. Models target FX risk, so we exclude all cash flows that are in the reporting currency of the group and any business unit with the same reporting currency as the group. For a US subsidiary with a US holding company reporting in USD, all USD cash flows can be excluded from the analysis.

We include all intercompany cross-border payments, where the payment is not in the reporting currency for at least one of the entities. These cash flows have a CFaR impact on the individual subsidiary but no impact at a group level. Hedging at a subsidiary level can increase risk at the group level, as is explained later.

The example below in Diagram 1 is a series of cash flows between subsidiaries, customers and suppliers in different currencies for a group with USD reporting currency. CFaR is measured at a business unit level to manage FX risk at each business, while EaR is measured at a group company level to manage the impact of FX rates on the groups earnings.

At a business unit level, hedging can create group-level risk. For example, hedging the cash flow in the first row above by buying EUR forwards to pay the European subsidiary in six months reduces the CFaR risk for the UK subsidiary. This creates EaR at a group level on both cash flows of the FX hedge. If the group had no exposure before, the hedge is effectively a new risk. Hedging the European supplier payment removes the CFaR for the subsidiary and removes the EUR exposure at the group level, but creates a GBP EaR.

If the value of the cash flow at a group level is variable because of FX rates, then it will have an impact on group-level earnings. Since it is the reporting currency of a foreign business unit, it is not a risk at a group level. For example, does GBP net revenue in a UK (GBP) subsidiary have an impact on the earnings of the US (USD) group company? The answer is yes. A fall in the GBP/USD FX rate will reduce the earnings of the group.

Looking holistically at the problem, we are managing the cash-flow movements of the business. This does not include amortisations, accruals or other non-cash items that are part of a business P&L, therefore cash-flow movements are a quasi-earnings currency risk position. We are applying a solution to identify cash flows that create volatility to earnings because of FX rate movements.

Modelling and monitoring EaR and CFaR is something treasury departments should consider engaging in either as their main FX risk management process or as a check and validation on an existing risk policy approach. Consistently applying this methodology could prevent your company from being in the news for a double-digit percentage fall in earnings due to unforeseen FX rate movements.

Mark Lewis is Bloomberg head of corporate treasury products