This blog is part of a regular series of blogs on the wide topic of Environmental, Social and Governance and covers items that have caught my attention.

Official announcements

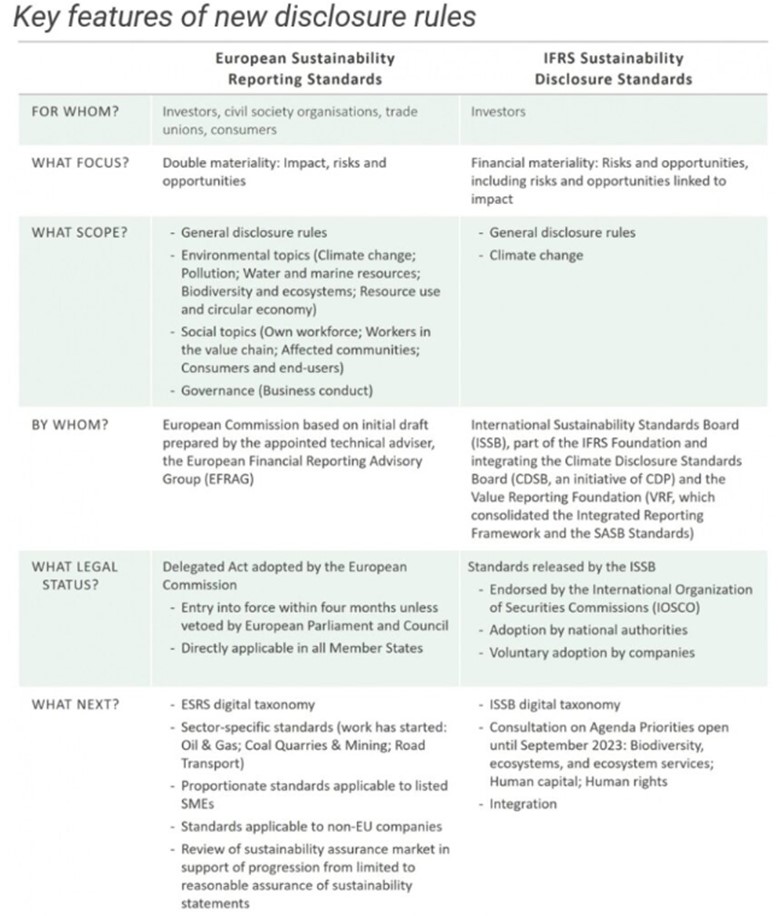

- The European Commission has published the final text of its first set of 12 European Sustainability Reporting Standards (ESRS). Disclosures will be required for the 2024 reporting period for public interest entities and companies with listed securities on EU-regulated markets which are large and have more than 500 employees (e.g., those already subject to reporting requirements under the NFRD). The new standards are intended to provide relevant, consistent, and comparable data under the new reporting framework - the Corporate Sustainability Reporting Directive.

- The FCA published a letter to banks and companies, outlining a series of market integrity concerns related to the sustainability-linked loan (SLL) market that it said could hold back the development of a useful net zero transition financing tool and raise the risk of greenwashing. Corporate interest in sustainability-linked loans has grown rapidly over the past several years, as the financing provides flexibility to use proceeds for general corporate purposes. Integrity-related concerns included weak incentives in the sustainability-related terms of the loans, and low-ambition sustainability targets and indicators chosen for the loans.

- The ESG Data and Ratings Working Group (DRWG), an industry group formed at the request of the FCA, launched a draft voluntary Code of Conduct for ESG ratings and data providers. The DRWG also established a consultation into the draft Code, which will remain open until October 5, 2023. Key aims of the code include:

- improving the availability and quality of information for investors at both the product and entity level

- improving transparency, governance and systems and controls in order to enhance market integrity, and

- fostering better comparability of products and providers in order to improve competition in the ESG data and ratings space.

The new code of conduct comes as IOSCO (the securities regulator standards setter) urged regulators to focus on improving transparency in the ESG ratings and data space, and to begin to apply regulatory oversight. At the same time, the EU Commission unveiled a proposal for ESG ratings providers to be supervised by European markets regulator ESMA, to ensure quality and reliability, with requirements including the use of rigorous and objective methodologies, conflict of interest prevention, and improved transparency into methodologies, models and key rating assumptions

- S&P Global Ratings announced that it will no longer include its ESG credit indicators in its reports on rated entities. The ESG credit indicators were introduced in September 2021, outlining the influence of ESG-related factors such as climate risk on its credit rating analysis on a 1 (positive)-to-5 (strongly negative) scale. S&P stated that it has “determined that the dedicated analytical narrative paragraphs in our credit rating reports are most effective at providing detail and transparency on ESG credit factors material to our rating analysis.”

- The International Auditing and Assurance Standards Board (IAASB) announced the launch of International Standard on Sustainability Assurance (ISSA) 5000, a new proposed standard focused on assurance on sustainability reporting. The new standard comes as companies begin reporting on sustainability and climate-related risks, opportunities and impacts, following the series of new sustainability disclosure standards and regulatory requirements, including the EU’s CSRD rules, the U.S. SEC’s upcoming climate disclosure rules, and the IFRS climate and sustainability reporting standards by the International Sustainability Standards Board (ISSB).

- The ISSB will take over responsibility for monitoring progress of companies’ climate-related disclosures from the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD) as of next year.

Resources, reports and announcements

- According to a survey by Fidelity International, of 123 of its in-house analyst from across the firm’s Equities, Fixed Income, Private Credit, and Sustainable Investing teams, aggregating bottom-up information from approximately 15,000 company interactions, approximately 60% of analysts estimated that the ESG credentials promoted by the companies that they cover are not backed up by their actions. This is despite companies becoming more responsive on ESG issues, as they increasingly tie sustainability factors to remuneration and assign board-level oversight to ESG.

- The Voluntary Carbon Market Integrity Initiative launched its Claims Code of Practice - a rulebook for companies to navigate carbon markets and make credible climate claims. The code aims to build market confidence for companies’ engagement with voluntary carbon markets (VCMs), to accelerate corporate VCM use as part of their net zero pathways. Demand for carbon offset projects and related credits is expected to increase significantly as companies and businesses turn to offsets as a bridge to their own absolute emissions reduction efforts, or to balance difficult to avoid emissions.

- Microsoft announced a series of new features being added to its sustainability platform - Microsoft Cloud for Sustainability. These include capabilities to help companies meet emerging ESG reporting requirements and regulations, calculate Scope 3 emissions, and collect and manage a broad range of ESG data across categories and data sources. Its platform enables companies to record, report, reduce and replace their emissions.

- Spanish insurance company MAPFRE announced it had decided to discontinue its membership in in the Net-Zero Insurance Alliance (NZIA) – joining firms such as Lloyds, AXA, Sompo, Allianz, Scor, Munich Re, Swiss Re and Zurich insurance Group.

- Fitch Group launched a ESG Regulations and Reporting Standards Tracker - aimed at monitoring significant regulatory developments in the ESG space, including sustainable taxonomies, ESG and climate disclosure regulations, and ESG fund requirements. The downloadable Excel-based database will be updated quarterly and maintained by Sustainable Fitch’s Research team, with information collected from sources including government statements, media reports, participation in sustainable finance working groups, and others.

- The Science Based Targets Network (SBTN) released the first corporate science-based targets for nature, aimed at guiding companies in assessing and prioritizing their environmental impacts and setting a standard for targets to address these issues. The new targets come as businesses increasingly focus on nature and biodiversity risk, and as global efforts to address nature-related issues begin to pick up pace. It follows global governments adopting the Kunming-Montreal Global Biodiversity Framework at the COP15 UN Biodiversity Conference. The SBTN is a collaboration of more than 80 organisations, established to help businesses and cities meeting society’s needs through the setting of science-based targets (SBTs) to transform their impact. The initiative was aimed at building on the momentum of the emissions-focused Science Based Targets initiative (SBTi).

- The 12th edition of Deloitte’s Gen Z and Millennial Survey looks back to see how the last three years have impacted these generations. It found that while they acknowledge some positive change, they remain deeply concerned about their futures. These concerns are likely to impact business’ recruitment and retention efforts, with around 55% of respondents reporting that they research brands’ environmental impact and policies before accepting a job, and more than 40% reporting that they already have, or plan to, change jobs due to climate concerns.

Naresh Aggarwal

Associate Director, Policy & Technical