The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last month. If you think I’ve missed anything important, do please send an email to technical@treasurers.com.

Central Bank Digital Currencies (CBDCs) and other digital currencies

It is becoming increasingly difficult to keep up with all of the announcements from a raft of central banks and think tanks but here are some that caught my attention:

- As part of the ACT Annual Cash Management, it featured a webinar by the Bank of England

- The Atlantic Council has produced an interactive map of the world showing which countries are undertaking work on CBDC

- The central banks of China and United Arab Emirates joined the Multiple CBDC (m-CBDC) Bridge digital currency project for cross-border payments being run in partnership with the BIS Innovation Hub, the Hong Kong Monetary Authority and the Bank of Thailand

- The Board of Governors of the US Federal Reserve System issued a Note setting out the pre-conditions for a general-purpose central bank digital currency

Interesting reports

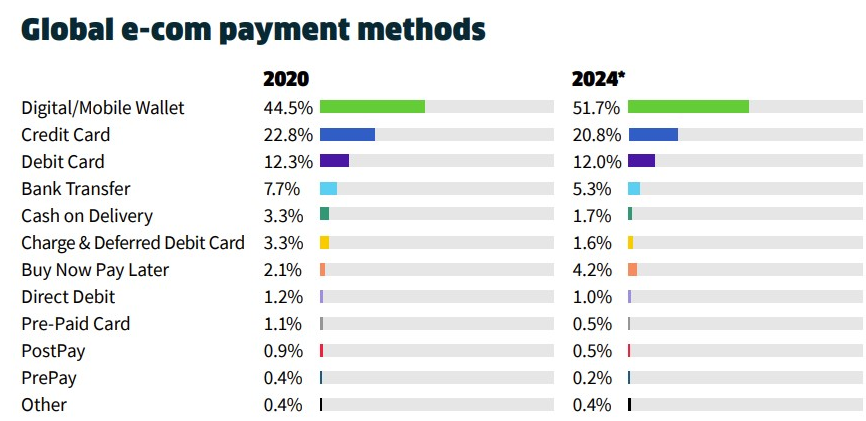

Worldpay issued its annual payments report.

Key findings include:

- Direct debit is a form of bank transfer where a retailer withdraws funds directly from a consumer’s bank account on a specified date after the purchase. Most popular in Europe where it earned 4% of share, direct debit was used for 1.2% of global e-commerce payments in 2020.

- Point-of-sale felt the impact of COVID-19 most directly, with 2020 global transaction volume falling 4.4% from 2019. Projections see recovery from the global recession transaction volumes taking 18-24 months, returning to 6.5% global growth rates in 2022, and then 3.3% growth in 2023 and 3.5% in 2024.

- Cash transaction values fell steeply around the world in 2020: by 21.9% in North America, 33.6% in Europe, 34.7% in Latin America and 36.6% in APAC. Cash has fallen to historically low usage around the world, representing only 5.4% of POS transaction volume in Canada, 4.5% in Norway, 11.9% in the U.S. and less than 10% in markets as diverse as Australia, Hong Kong and Sweden.

- A new category in our POS 2020 analysis is POS financing, which represents a mix of legacy and emerging payments that extend consumer credit at the point of sale. This includes credit offered by retailers, financial institutions, marketplaces and BNPL services. The spectrum of POS financing is broadening consumer payment choices while boosting merchant conversions. POS financing represents 3.5% of global 2020 POS share, projected to maintain fairly steady share at 3.3% in 2024.

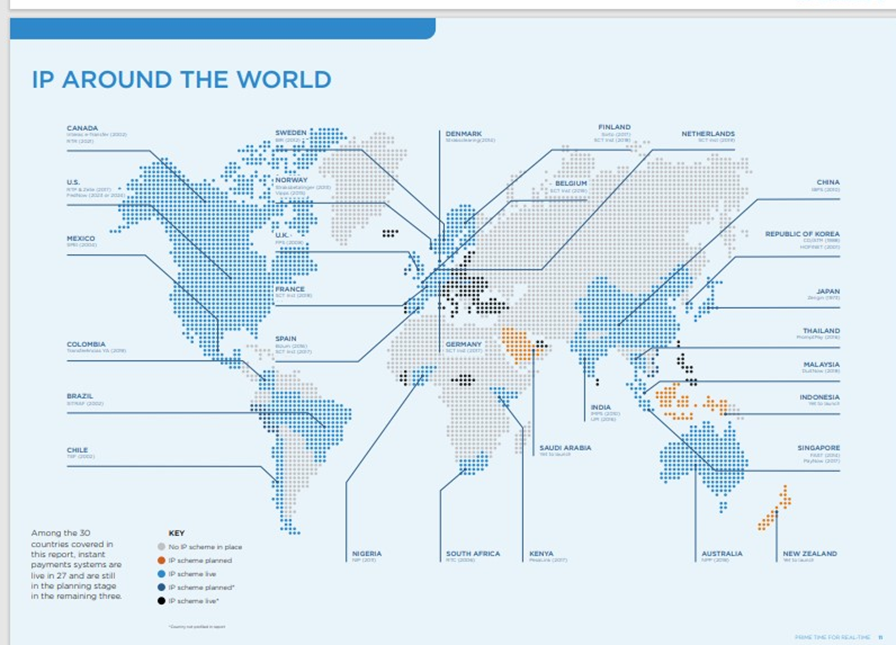

ACI issued its annual report. The report identifies the following areas as having the largest increase in instant payment volumes:

- Nordics: Denmark, Finland, Sweden and Norway as part of the P27 initiative

- United States

- ASEAN region: Indonesia, Malaysia, Singapore and Thailand as part of the Asian Payments Network

- India

- European Union as part of the rollout of the PSD2 directive

It also includes the infographic below showing the extent of instant payments across the world.

UK payments landscape

- The Competition and Markets Authority issued a consultation on the future oversight and governance of its open banking initiative. The initiative was established in 2017 to allow consumers and small and medium-sized enterprises to share bank account information with intermediaries so that the intermediaries can help find them better and more suitable financial products. The implementation phase of the initiative is nearing completion and the CMA is now consulting on oversight and governance arrangements. Responses are due by 29 March.

- The Kalifa Review of UK FinTech was released and one of its recommendations was that financial regulators such as the Bank of England, the Treasury and the FCA should get more involved in digital currencies and crypto-assets.

- The PSR launched a consultation on ways to reduce risks to the successful renewal of the UK’s interbank payment systems and proposals to mitigate risks to competition and innovation. It is concerned about risks to competition and innovation relating to when the NPA is operational, and how this may affect the quality, range and pricing of payment services delivered using the NPA. Any comments should be sent to PSRNPA@psr.org.uk. The following deadline applies:

- 5 May 2021 - deadline for comments on questions 7 to 14 of our consultation (and other comments on competition and pricing).

- The Chancellor of the Exchequer has approved an increase in the contactless payments limit from £45 to £100. This is a break with current EU arrangements.

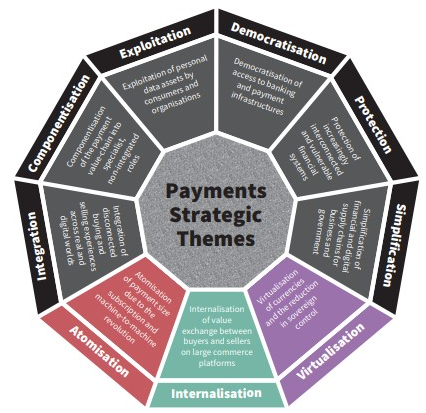

- Pay.uk issued a Strategic trends: Retail payments in a future world report. The report identifies 9 drivers of payment trends:

Global payments landscape

- The Italian Banking Association is promoting Spunta Banca distributed ledger technology. It has been fully operational for the interbank reconciliation process since last October.

- The European Commission has launched an impact assessment on an EU-wide instant payments scheme. This will investigate whether:

- new legislation is needed in this field

- non-legislative measures would be appropriate, or

- other policy options are suitable.

Naresh Aggarwal