Status Update – LIBOR transition

For those of you who have been away over the Summer (or just avoided thinking about LIBOR transition for a few weeks), here’s a quick round-up of recent developments and the current state of play.

GBP Markets – whilst not entirely ‘job done’, the majority of the feedback from the GBP markets is that participants generally have moved to the active transition stage and are ‘just’ working through the details of getting individual transactions transitioned away from LIBOR.

Corporates should definitely have heard from their banks and agreed on how the transition should take place (to what replacement rate, effective date, documentation approach - there is LMA guidance on this final point - etc.). If you haven’t heard, chase them and then let us at the ACT know – particularly if you’re not getting the help you need. As active members of the various LIBOR working groups for the last few years, we have connections across the markets (and with the regulators) that we can access off the record if you need.

However, the picture across the market as a whole is not quite perfect:

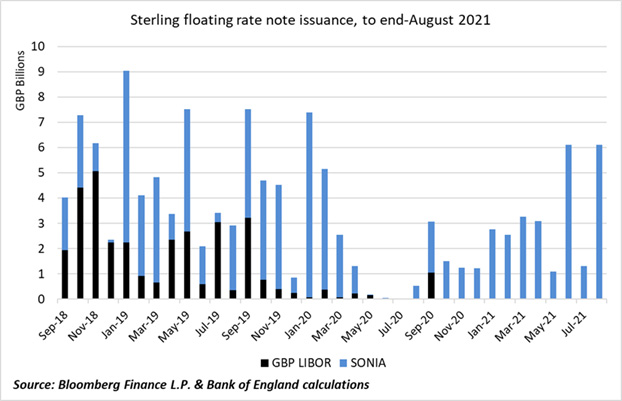

On the one hand, this chart highlights the complete transition away from LIBOR in GBP floating rate notes – there has been no new GBP LIBOR-linked issuance since March 2021, in line with the Working Group’s recommended end-Q1 milestone.

On the other, arguably the last major outstanding issue is related to tough legacy and the practicalities surrounding those transactions that cannot be transitioned. The FCA has published a number of consultations exploring how they might manage the provision of a synthetic LIBOR for use in tough legacy contracts and there is legislation working its way through Parliament to provide legal certainty. However, this is all happening quite late in the day and so amendments may have to happen at the last minute on these contracts - perhaps another reason to get everything else sorted now.

One comment that we are hearing repeatedly is a reminder from the regulators that whilst a synthetic LIBOR might solve the immediate problem, there is no guarantee how long such a rate would be published – and therefore, synthetic LIBOR should only be viewed as a temporary (bridging) solution.

USD Markets – have been busy over the Summer, and it’s beginning to feel as it the direction of travel is more aligned.

In particular, the recommendation of a SOFR Term rate has been widely welcomed and should reduce the demand from some parts of the market for credit sensitive rates (such as BSBY) as an alternative to LIBOR. In support of Term SOFR, the ARRC published recommendations for loan conventions and best practices for use of a forward-looking SOFR Term Rate. They also followed up with an FAQs document.

The U.S. Department of the Treasury responded to a letter sent by U.S. treasury associations including the NACT which flagged the apparent lack of engagement by US banks in LIBOR transition. Much has changed since the original letter in April, but the US Treasury response puts banks on notice that they are watching carefully to ensure there are no unintended consequences as a result of LIBOR transition for Main Street USA, and by association corporates exposed to USD LIBOR.

Other markets

There have been a number of ‘RFR first’ initiatives, designed to encourage transition of the derivatives markets (which as the largest, most liquid users of LIBOR are key to successful market wide transition).

As part of encouraging the transition from EONIA to €STR, The Chair of the euro Risk-Free Rates Working Group wrote to the European Commission to propose the designation of a statutory replacement rate for EONIA as €STR plus 8.5 basis points as a fallback for those contracts not otherwise transitioned.

The World Bank announced that it will enable use of RFRs (SOFR, SONIA and TONA) for new and existing loans effective from 1 January 2022 for new transactions.

In Singapore, the Steering Committee for SOR & SIBOR Transition to SORA (SC-STS) published updated timelines and recommendations for the transition of legacy exposures based on SOR.

Appendix

We are going to include this appendix each month as a quick reference for useful sources:

For the latest markets data, we’d recommend ‘going to the source’, so the RFR WG in the UK; the ARRC in the USA etc.

By currency, the ‘source’ information comes from:

The RFRWG also publishes a monthly newsletter offering a one-page summary of latest developments. Sign up to receive it monthly - the latest (August) version is here.

If you are looking for suggested ways of approaching the transition project, the ACT website has resources.

Other useful resources include relationship banks, advisers, trade associations such as UK Finance and the FICC Markets Standards Board (FMSB).