The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last three months. If you think I’ve missed anything important, please send an email to technical@treasurers.org.

Regulatory announcements

- The Bank of England continues to seek feedback on a possible extension of the opening hours of the CHAPS system. The Policy and Technical team has been working closely with the Bank and we hope to gather a group of payment leaders from businesses operating in the UK during Q4 to discuss the next steps.

If you have any views or would like to join the group, please drop an email to technical@treasurers.org.

- The Payments Systems Regulator (PSR) published a Working Paper – Market review of UK-EEA cross-border interchange fees. Amongst its observations was that:

- Mastercard and Visa have increased IFs for card-not-present (CNP) UK-EEA transactions using consumer and debit cards from 0.2% and 0.3% to 1.15% and 1.15% respectively and fees paid by acquirers increased by approximately £75 million to £100 million in the first half of 2022.

- UK merchants who are selling online to EEA customers and are not able to relocate may find themselves at a competitive disadvantage compared with EEA competitors selling online to the same EEA customers.

Interesting reports

- The Financial Stability Board issued its 2023 Consolidated progress report on the G20 Roadmap for Enhancing Cross-border Payments. The report noted the following:

- For the first time, data exists to measure how far we need to go to achieve the 2027 targets that G20 Leaders have endorsed for material improvements in the speed, cost, accessibility and transparency of payments across borders.

- There are encouraging signs of progress, and the data provide some clear indications of where investment and action by the public and the private sector could make the most significant contribution to achieving the targets.

- We have also made good progress at putting in place the structures we need to encourage and facilitate the necessary action by both the public and private sectors, without which the targets will not be met. But there is a considerable distance to go and more needs to be done across all of the key areas for action. The picture varies considerably by region and by type of payment – the data shows where we need to foster the greatest improvement, which will be the priority for future work.

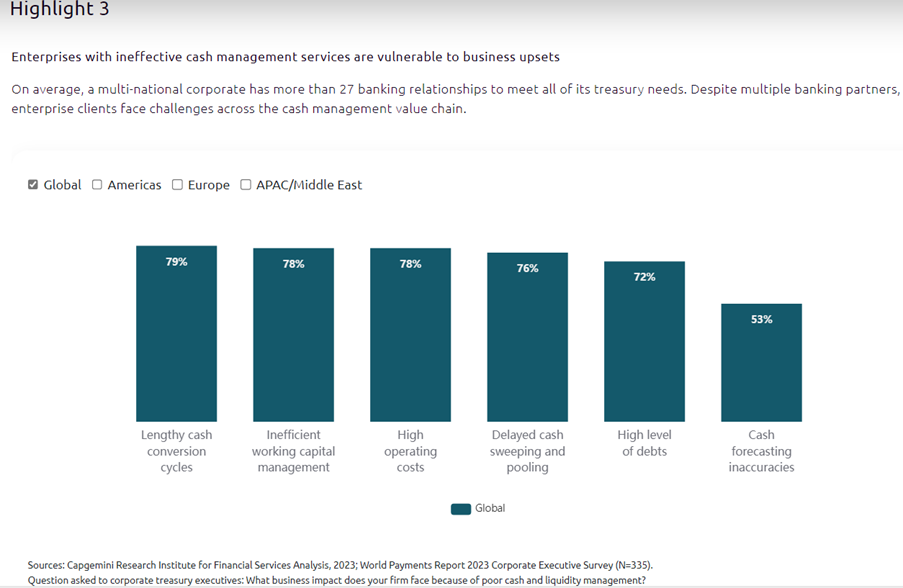

- Capgemini has released its World Payments Report 2023. One of the highlights in the report is extracted below:

- McKinsey’s released the 2023 edition of its Global Payments Report. The report includes the following observations:

- Cash usage declined by nearly 4% globally in 2022. Worldwide, the decline in cash usage during the pandemic shows no evidence of being reversed, led downward by the cash-reliant economies of India and Brazil, where the share of cash transactions fell by seven to ten percentage points. Brazil’s cash declines are concurrent with the rapid uptake of the country’s PIX instant-payments network.

- In Nigeria, where instant-payments capabilities are being built into point-of-sale devices to facilitate merchant enablement the share of cash transactions fell from 95% in 2019 to 80% in 2022. Over the same period, instant payments’ share quadrupled to 8%.

- Instant payments are playing a key role in the transition out of cash - in Brazil, almost half of transactional revenue growth through 2027 is expected to come from instant payments. Against this, instant payments in India are expected to contribute less than 10% of future revenue growth because no fees are currently charged for the Unified Payments Interface.

- By 2027, cash-heavy developing economies are likely to make further significant shifts toward instant payments, bringing these transactions’ share to roughly half of overall payment transactions – almost three times greater than in 2022. By contrast, our analysis indicates that near-term impact in mature markets such as the US and UK will be nominal. July 2023’s launch of the Federal Reserve’s FedNow real-time payment rails may prove to be an inflection point, but the effect will be gradual.

- Instant payments constitute 12% of the credit transfer volume in the Single Euro Payments Area (SEPA). Absent regulatory intervention, this share could double by 2027, and if regulators proceed with anticipated actions to encourage adoption, this share could rise to 45% of SEPA’s 23 billion annual transactions and a far higher share of account-to-account (A2A) payments, including transfers done through Automated Clearing House (ACH), real-time gross settlement (RTGS), and instant payments.

- According to a report from PYMNTS and The Clearing House, Corporate Changes in Payment Practices: The Retail Industry is Ramping Up Real-Time Payments, real-time payments are strengthening B2B relationships, with partners on both sides of the transaction reporting that they benefit from the payment method.

Naresh Aggarwal

16 October 2023