There is lots of real value in the report and for those with time I would recommend a full read as the report and the sources it has drawn on are very insightful.

Many of the areas it covers address how the Bank pursues its regulatory obligations but many of the topics directly or indirectly impact treasurers. This article discusses those themes I feel are most relevant to treasurers in the UK, though as many of the observations are global in nature, they will be of interest to treasurers elsewhere.

I have also included a section of facts that I found interesting and finish with a short section on the areas I have not covered, and which are more focused on the regulatory role of the Bank.

The economy is undergoing profound changes that affect all aspects of life for individuals and businesses and raise challenges to current views on risks and approaches to regulation, economic modelling and banking.

Finance can:

New payments system: Much has been written already about the changes in the payment infrastructure in the UK with the replacement of the Real Time Gross Settlement System (CHAPS) and the design of a new payments architecture by pay.uk. The report has added to this by considering the increasing fragmentation of the payments chain and the potential need for tiering of regulation, and ways to supervise the entire payments value chain.

The Bank needs to review who can access its infrastructure, including reserves accounts, to support greater innovation, focusing also on the “regulatory package” for access. It needs to keep evaluating how financial innovation and changing business models will impact financial stability. This includes the growth in market-based finance (i.e. funding via the bond and stock markets) and the unbundling of financial services value chains.

The Bank will also need to consider the implications of separation of payments and lending from deposit-taking and the implications for the core banking system. Regulators will need to watch out for new platform-based businesses outside finance entering parts of financial services if they take on risks deemed as regulated activities.

Digital currencies: Whilst acknowledging new messaging standards and the rise of digital tokens, the report was clear that it did not see crypto assets not backed by currency as effective money. There was no compelling argument for a central bank digital currency given a number of uncertainties and the report felt that the Bank would be better placed to focus its resources on improving efficiency and cyber-security and enabling the core payment systems to be a platform for private sector innovation.

Cloud: Complex regulatory requirements are felt to have limited the use of cloud technologies by the financial services sector with UK banks and insurers seen as lagging behind global leaders. Despite the regulatory drag, it recognised that almost every vendor to financial service firms and fintechs are already cloud hosted meaning that the UK system is already heavily reliant on cloud.

Cloud computing provides flexible and agile infrastructure and reduces barriers to entry for smaller players who might not be able to invest in their own solutions, offering ready-made platforms for early-stage companies, including fintechs to cut their time (and cost) to market.

McKinsey & Company estimate that 40%–90% of banks’ workloads globally could be hosted on public cloud or use software as a service in a decade (compared with 14% today). Finastra has found that 30% of financial institutions surveyed in the UK and 33% in the US have moved towards payments or collaboration in the cloud, behind Singapore with 42%.

Banks primarily use the cloud for customer relationship management, human resources and financial accounting. But a growing number could expand to consumer payments, credit scoring and asset management. And increasingly, financial firms’ technology vendors are dependent on the cloud, creating reliance in the supply chain.

Credit files: Building standards and protocols that enables business data to be easily incorporated into lending decisions has the potential to make lending decisions (especially for small and medium size enterprises) more efficient and fairer. Research suggests that the use of company permissioned tax data could have a significant impact on financing solutions for this sector.

Peer-to peer payments: Adoption in the UK of these types of payments is much lower than many other countries. Sweden, Netherlands and Denmark have seen significant use of this network of payments and it has extended from the P2P market to the B2C market – especially for retail and utility payments.

Cyber-attacks: The payments sector must be resilient to increasingly sophisticated cyber-attacks. The complexity of payment networks including the growing dependence on shared solutions, such as APIs, can create common vulnerabilities.

Payment liability: Greater clarity on who holds liability and carries risks for consumer redress will help the market to innovate. This includes the areas of AML/KYC, fraud, failed transactions, mis-selling, cyber-risks and privacy. The Bank will need to consider whether the liability and risks sit with incumbents or new payment providers and the implications for innovation and market stability.

The regulatory framework for firms involved in the payment chain may need amendments to make sure providers have enough financial resources to protect their customers if things go wrong.

|

What does this mean for the treasurer? Treasurers need to be aware of the changes to the payment landscape and the role of cloud when making changes to their own technology solutions. Understanding how their own suppliers use the cloud will help identify any concentration risk. Treasurers also need to understand the increase in risks with shared applications and what their roles and responsibilities are with a more fragmented payment value chain. |

As part of the upgrade of the payments infrastructure, the Bank is future-proofing the system by:

Cloud: There is a recognition that as fintechs and incumbent financial institutions move services onto cloud platforms, major cloud providers may become systemically important.

The small number of service providers could risk becoming a single point of failure and it’s possible that supervisory powers might have to be extended if supervising “through” regulated firms is no longer deemed sufficient. Regulators may have to engage with service providers directly to ensure they meet supervisory expectations. Alternatively, cloud providers could become regulated public utilities, creating a “certified cloud”. It is also possible that regulators will evaluate specific areas such as managing service level agreements and fall-back arrangements.

(Policymakers recognise that, similar to the use of central counterparties for the clearing of standardised derivatives, creating concentrated nodes could make the overall system safer.)

|

What does this mean for the treasurer? Despite the reticence of most treasurers to use distributed ledger technology, the fact that the Bank of England is preparing for it suggests that Treasurers need to understand the flexibility of their own payments infrastructure. The increasing use of the cloud suggests that treasurers need to ensure their IT teams have understood how their choice of banking partners may increase their overall exposure to a single cloud provider. |

Data standards: The volume of data is increasing at an exponential rate and one of the challenges for business will be how to harness the information to lead to better outcomes. Creating standards and protocols could bring several benefits including:

AI and Machine Learning: Machine learning can facilitate faster, more efficient and more personalised financial services at a lower cost. Firms can gain insights from customer data on everyday transactions, spending habits and preferences, especially when supplemented by data from social media platforms, wearables and location devices. AI could improve the safety and soundness of organisations, too, by making risk management more effective and reducing fraud. AI is already being used to understand and predict developments in financial markets, analyse risk scenarios, identify fraud and to monitor transactions.

Ethics: Despite the benefits of data, its use is of great concern to regulators, businesses and citizens. To promote trust, standards and guidelines will need to be developed. This will encourage the design and application of new use cases and confidence in exploring new ideas. To support a fair use of data and AI, three areas of focus are:

Finance platforms for SMEs: Data available on SMEs is much greater than ever before and as a result the right lenders, with the right information, can make better and more informed lending decisions. Examples include Amazon extending trade credit to businesses selling on its marketplace and PayPal offering credit to online customers based on their transaction history. In the UK, Xero have an agreement with RBS which enables them to onboard customers using their account information. This deeper financial history may unlock working capital, and invoice and trade finance.

Open Banking and the increased use of APIs may make it easier for businesses to compile their business profile and to find financial service providers that are more focused on their specific business needs. It may reduce the effort and costs involved in moving from one bank to another.

|

What does this mean for the treasurer? Treasurers should be part of any internal working group that looks at the use of big data and the application of AI to customer and supplier information from a credit risk and working capital perspective to ensure that it complies with regulations and emerging good practice. For smaller businesses, there are an increasing number of choices when it comes to assessing credit and lenders who can review a wider range of data than traditional lenders did, offering new financing opportunities. |

As a consequence of industrialisation, we’re seeing the highest rate of atmospheric CO2 for hundreds of thousands of years with surface temperatures increasing by 1°C and sea levels 20cm higher since 1850. Unchecked, this trend will present grave threats to the environment and the economy.

Risk drivers: There are two channels driving risks:

Barriers: Despite the urgency of the issue, there remains a lack of consistency in how businesses and policy makers are taking action. Some of the reasons for this are:

|

What does this mean for the treasurer? Treasurers need to be part of an internal process to assess their current carbon footprint and to consider how to manage the current financial risks that climate changes poses to their business and how they will finance a transition to a low carbon economy. |

One of the defining changes over the past ten years, which will shape the future of finance and markets for now and in the coming years, is the reform of the financial system and the rise of market-based finance.

New entrants are unbundling financial services and dividing them into their core activities. These include payments, settlement, safeguarding assets, savings, lending, insurance and investments. Unbundling can involve activities transferring to new players, including those who may be outside of the regulator. It can also lead to narrower, more specialised business models that can bring efficiency and customer focus, but may be more vulnerable in downturns due to their focus on a relatively narrow set of clients and activities.

It’s not clear what the future landscape will look like but we may see some combination of:

|

What does this mean for the treasurer? Whilst many of the changes will take time to develop, treasurers should understand the strategy of their existing financial institutions and keep an eye on the services being offered by new entrants. |

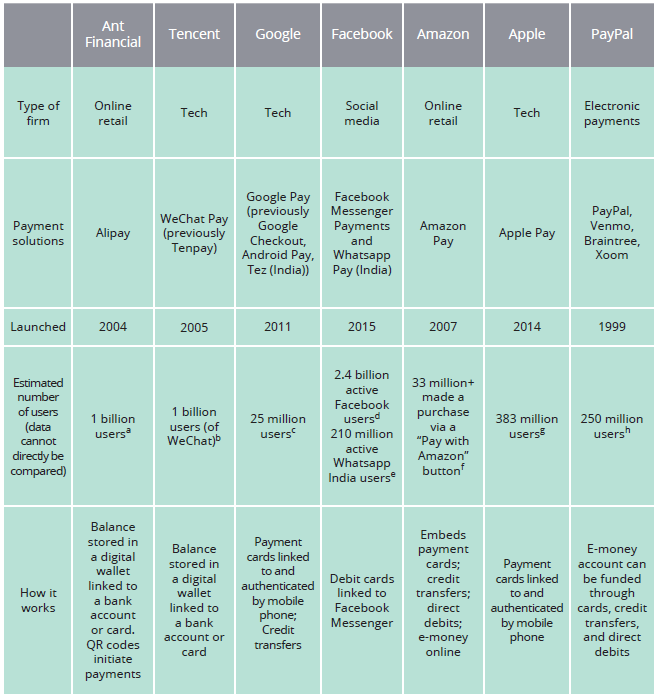

Overview of selected payment providers

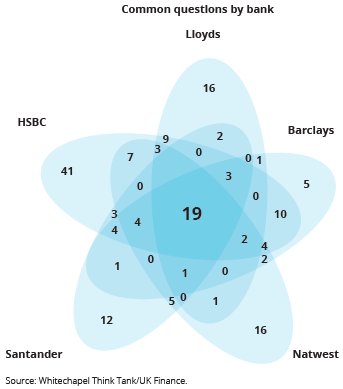

Questions asked of SMEs when opening an account in the UK

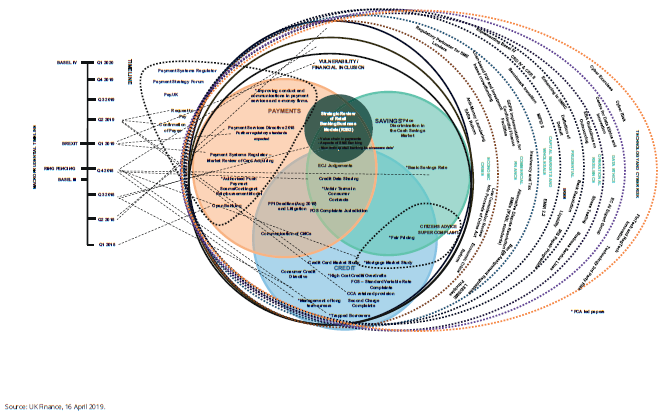

The complex and overlapping world of regulation

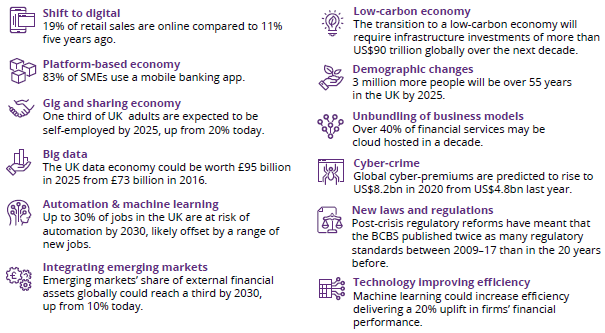

Did you know that:

Cyber: Cyber‑security is at the top of the financial sector’s agenda. In the latest Bank of England Systemic Risk Survey, cyber‑risk was the second‑most cited source of risk by firms at 66%. Only “Brexit/political risk” was more common at 97%. The Bank employs penetration testing and runs exercises such as SIMEX and international ones such as the Resilient Shield Exercise with the US. In addition, firms need to have recovery plans in place.

Demographics: As our population ages, policy changes will be needed to facilitate greater security in retirement. Finance will also need to support major changes in demographics and working patterns as well as the evolving needs of savers and borrowers.

Cash: The Bank will need to consider how to manage the decline in the use of cash whilst ensuring that all citizens continue to have access to cash machines.

Digital ID: Although the costs of verifying customer identity is very high, the absence of a digital identity supports fraudulent activity. The government should consider the merits of secure and efficient information gateways to trusted official sources.

Global standards for finance: As a global financial centre, UK firms are exposed to a number of emerging markets and the Bank will need to foster strong global financial standards and deep supervisory co-operation.

Digital regulation: The Bank needs to look at how to use data analytics and AI to improve its supervisory operations. This may include requesting data rather than returns and developing tools to interrogate the data. The use of machine-readable rules and AI could help firms and supervisors navigate the rulebook more effectively and efficiently.