This blog is part of a regular series of blogs on the wide topic of Environmental, Social and Governance and covers items that have caught my attention.

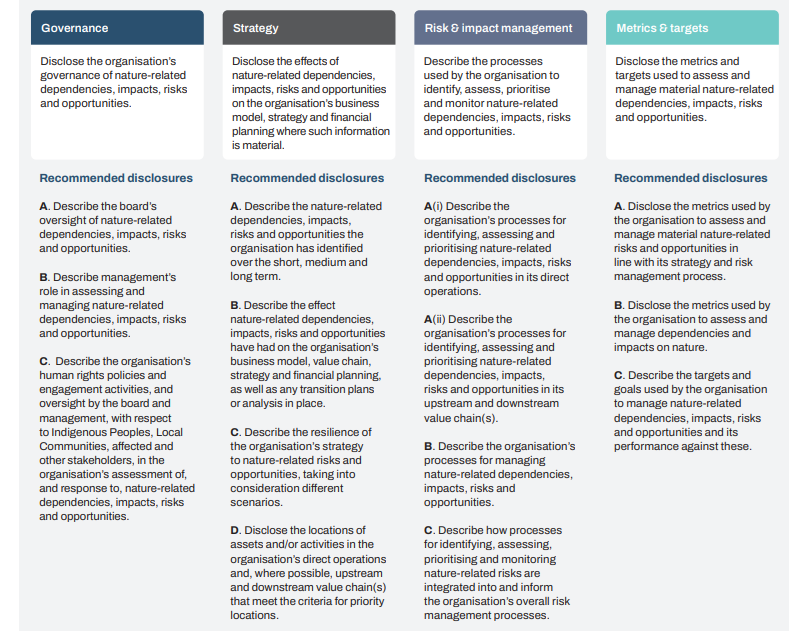

The Taskforce on Nature-related Financial Disclosures (TNFD) announced the publication of its long-awaited final recommendations for nature-related risk management and disclosure, aimed at helping inform better decision-making by companies and capital providers on nature and biodiversity-related risks, opportunities, dependencies and impacts, as well as to contribute to a shift in financial flows towards nature-positive outcomes and the achievement of global biodiversity and ecosystem preservation goals. It includes the following recommended disclosures:

The Council of the EU adopted a regulation creating a European green bond standard which lays down uniform requirements for issuers of bonds that wish to use the designation ‘European green bond’ or ‘EuGB’ for their environmentally sustainable bonds. It is hoped that the new standard will foster consistency and comparability in the green bond market, benefitting both issuers and investors of green bonds and that issuers will be able to demonstrate that they are funding legitimate green projects aligned with the EU taxonomy. Investors’ confidence in green investment will be enhanced thanks to a framework that reduces the risks posed by greenwashing, ultimately stimulating capital flows into environmentally sustainable projects.

As part of its 2024 Work Programme, the European Commission announced delays to key aspects of its Corporate Sustainable Reporting Directive (CSRD), including the adoption of requirements for companies to provide sector-specific sustainability disclosures and for sustainability reporting from companies outside of the EU.

The Commission is aiming to postpone the adoption date for the sector-specific ESRS by two years. The CSRD also included a requirement for large non-EU companies that operate in the EU to provide sustainability reporting, with ESRS adoption of rules applying to these businesses also scheduled for the end of June 2024, and with reporting requirements to begin in 2028. Under the new proposal, the Commission also recommended delaying the adoption of these rules by 2 years.

The postponement of these rules will fulfil objectives including “allowing companies to focus on the implementation of the first set of ESRS,” “ensure that EFRAG has time to develop sectoral ESRS that are efficient,” and “limit the reporting requirements to the minimum necessary.”

Morgan Stanley’s Institute for Sustainable Investing and the Stanford University-based Natural Capital Project announced the development of a new tool aimed at enabling companies and investors to assess the potential impacts of projects and activities on natural ecosystems. The tool is open-source and free to use. It allows companies choosing between locations to develop a new facility to compare impacts, such as water quality from loss of ecosystems, people’s ability to access nature, as well as exposure to coastal flooding and erosion.

Resources, Reports and Announcements

Naresh Aggarwal