This blog is part of a regular series of blogs on the wide topic of Environmental, Social and Governance and covers items that have caught my attention.

COP27

COP27 is underway in Sharm el-Sheikh, and finance took a centre stage on 9 November. Key announcements included:

- A G7-led plan dubbed "Global Shield" to provide funding to countries suffering climate disasters was launched and coordinated by G7 president Germany and the V20 group of climate-vulnerable countries. It aims to rapidly provide pre-arranged insurance and disaster protection funding after floods, droughts, and hurricanes hit.

- China would be willing to support a mechanism for compensating poorer countries for losses and damage caused by climate change but said that would not involve contributing cash.

- U.S. Special Presidential Envoy for Climate John Kerry, the Bezos Earth Fund, and The Rockefeller Foundation announced a process to design an Energy Transition Accelerator (ETA) with the potential to catalyse private capital for the clean energy transition in emerging and developing economies. According to the IEA, the world needs $4.2 trillion in clean energy investment, half of which is required in developing and emerging economies. The process aims to design a new type of high-quality carbon credit framed by robust guardrails to channel much-needed private sector investment to phase out fossil fuels and accelerate renewable energy. The Science Based Targets Initiative (SBTi), the Voluntary Carbon Markets Initiative (VCMI), the Integrity Council for the Voluntary Carbon Market (ICVCM), and WRI for the Greenhouse Gas Protocol will be consulted to ensure broad alignment with best practice environmental and carbon market standards.

- GenderSmart, the Women in Finance Climate Action Group and the 2X Collaborative called on all allocators of public and private climate finance and other key stakeholders in the financial system to take urgent action to improve gender equality when designing, delivering and accessing climate finance.

- The sustainable debt coalition was established to bring like-minded countries to commit to the delivery of sustainable debt principles aligned with the Paris Agreement's goals. This would bring together initiatives to increase access to affordable green finance and facilitate either refinancing of existing debt or the issuance of new debt aligned to climate key performance indicators.

- “Reducing the Cost of Green and Sustainable Borrowing” initiative in climate-vulnerable countries was launched. It is aimed at addressing the more significant issues of deteriorating fiscal health under threat by potential output losses linked to climate hazards and disaster recovery costs, as well as transition risks that may hit the economy at large. Noting that “Liquidity constraints remain some of the foremost barriers to allowing African countries to invest towards climate resilience and the Sustainable Development Goals. The focus will be on Green and Social and Sustainable (GSS) Bonds to fill the SDG financial gaps. This initiative will strengthen the ability of African states to borrow at an affordable rate, mobilise more green funding, and attract private capital.”

- African countries can lower green borrowing costs by pulling various levers, such as the Liquidity and Sustainability Facility (LSF), which seeks to reduce governments’ borrowing costs by increasing demand on their sovereign bonds. It includes the proposal of a Sustainability Sovereign Debt Hub (SSDH) considered vital to lowering green borrowing costs by facilitating sovereign debt issuances aligned with climate and nature building.

Official announcements

- At its October meeting the ISSB voted unanimously to require company disclosures on Scope 1, Scope 2 and Scope 3 greenhouse gas (GHG) emissions, applying the current version of the GHG Protocol Corporate Standard. As part of these requirements, the ISSB will develop relief provisions to help companies apply the Scope 3 requirements. This relief will be decided at a future meeting and could include giving companies more time to provide Scope 3 disclosures and working with jurisdictions on so-called ‘safe harbour’ provisions.

- The ISSB has decided to focus its future work on two components―foundational work supporting the adoption and application of its first two Standards; and new areas of work on which it will consult in the first half of 2023. The foundational work will include providing supporting materials and developing a digital taxonomy to enable digital reporting; enhancing SASB Standards by making targeted improvements to make them more internationally applicable; coordinating work with the International Accounting Standards Board to support connectivity in the two boards’ requirements and considering operability with the work of others―including GRI and EFRAG; and researching areas for potential incremental enhancements to its proposed Climate Standard.

- At its November meeting, the ISSB looked at interoperability with other standards and:

- It was confirmed that content from the former Climate Disclosure Standards Board (which are also now materials of the ISSB) might be considered by companies as a valuable framework to identify sustainability risks and opportunities as well as disclosures. This is particularly the case for topics such as biodiversity and water, which the ISSB will work on as an extension to S2 concerning climate risks and opportunities.

- S1 should reference additional standards that are created for a broader stakeholder’s group extending beyond the primary users that are the focus of ISSB standards. S1 establishes the global baseline for reporting by requiring an entity to provide material information for investors about all of its sustainability risks and opportunities in its full value chain. In the absence of directly applicable ISSB standards, the ISSB discussed whether companies applying S1 should be permitted to consider metrics developed by the Global Reporting Initiative (GRI), along with European Sustainability Reporting Standards (ESRS) developed by the EFRAG (European Financial Reporting Advisory Group), as a useful source of disclosures to the extent that those disclosures meet the information needs of investors. It was noted that allowing entities to use these materials in the absence of a specific ISSB Standard will reduce the reporting burden for companies applying these standards for other purposes but that it was important to ensure that the information presented was consistent with the ISSB’s role of meeting the needs of primary users.

Podcasts from the ISSB following their monthly meetings can be accessed here.

- The UK’s FCA provided a summary of its climate-related reporting requirements noting that if your firm falls into one of the following groups, you may need to consider ESG-related risks and opportunities when determining what to disclose:

- listed issuers.

- other issuers with securities admitted to trading on regulated markets.

- other entities in scope of requirements under the Market Abuse Regulation (MAR) and the Prospectus Regulation.

- The FCA has launched CP22/20: Sustainability Disclosure Requirements (SDR) and investment labels in order to clamp down on greenwashing. The consultation closes on 25 January 2023 and you are welcome to share views directly with the FCA or send them to the ACT’s Policy & Technical team at technical@treasurers.org.

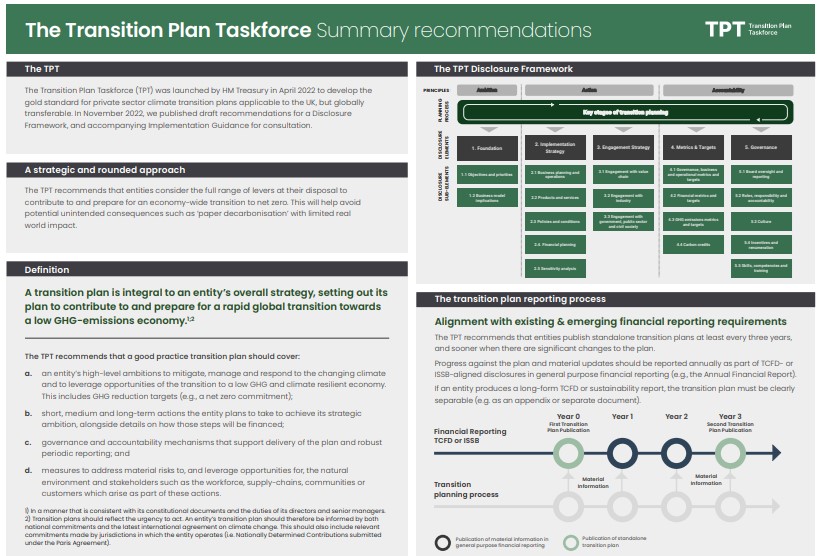

- In the UK, the UK Transition Plan Taskforce (TPT) has published its Disclosure Framework and accompanying Implementation Guidance. It has also launched a Sandbox for companies and financial institutions to test implementation.

- The TPT Disclosure Framework (‘the Framework’) makes recommendations for companies and financial institutions to develop gold-standard transition plans.

- The TPT Implementation Guidance (‘the Guidance’) sets out the steps to develop a transition plan, and when, where and how to disclose their plan.

The Sandbox will test the Framework and Guidance to help users and preparers create their transition plans.

It includes the following summary:

- UK Export Finance (UKEF) will become the world’s first export credit agency to introduce climate-resilient debt clauses (CRDCs) into its loan agreements, which will provide low-income countries and small island developing states the ability to defer debt repayments in the event of a severe climate shock or natural disaster. Additionally, the Private Sector Working Group, chaired by the UK Treasury, will launch a “model term sheet” to embed climate resilient debt deferral into standard bond and loan contracts.

Resources, Reports and Announcements

- The Network for Greening the Financial System (NGFS) has released a new dashboard (last updated March 2021) that aims to track and understand the greening of national financial systems. Covering 21 different activities, the dashboard covers areas such as:

- Carbon emissions

- Carbon pricing initiatives

- Fossil fuel subsidies

- Natural resources rent

- Flow of capital

The dashboard also includes metadata with the charts and a structured Excel file with the source data.

- Accounting for Sustainability issued the results of its inaugural survey of senior finance professionals from around the world, including Chief Financial Officers, Chief Investment Officers and accountancy leaders to gauge, at a global level, the current understanding and attitudes of finance leaders towards embedding sustainability into their decision-making processes. Key highlights included:

- There is a gap between sustainability ambitions and the work to make them a reality. Agreement on the necessary direction is there, but when it comes to ‘walking the talk’ there remains a sizable ambition gap. 93% agree it’s very important for their business to transform financial decision-making to reflect ESG issues. However, almost one in five (19%) reported that they do not consider ESG information when making decisions, instead relying almost exclusively on traditional financial considerations.

- CFOs must be a champion for change and bridge the skills gap. When capturing some of the opportunities related to ESG adoption, our respondents fully expect the CFO to step up to the plate. But there was also a clear opportunity for CFOs to build finance teams that are fit for the future through technology, skills and capacity building:

- 77% said the CFO is mostly or entirely responsible for realizing the opportunity of developing new technologies and innovations to share sustainable outcomes.

- Less than 1/2 believed their finance team had the skills and competencies for supporting ESG efforts (48%). Yet, 82% either don’t assess ESG competence during recruitment or promotions or do so only when recruiting for specialist roles.

- 81% said ESG information is considered important in their organisations’ decision-making, but 2/3 believe their organisation lacks the full suite of reliable tools and techniques to make this happen.

- Leadership ambitions and day-to-day operations are not matching up. Our more senior respondents backed ambition; however, this did not seem to be fully communicated to the rest of the staff. With staff retention being such a key driver for change, CFOs should look to improve internal communication and the culture of the finance team.

- 76% of Group CFOs said they personally backed this ambition; however, just one third (33%) of their more junior counterparts perceived such commitment from their own Group CFO.

- Nature is falling behind as a priority. Providing solutions to tackle climate change and improving diversity, equity and inclusion are now firmly in the sights of the finance community as the most significant opportunities. However, dealing with the drastic decline in nature is comparatively behind.

- Less than 1/4 identified redressing biodiversity loss as among their biggest ESG-related opportunities (24%). Compared to 3/5 when considering climate.

- 1/2 believe their organisation has made little or no progress in mitigating the risk of biodiversity loss and depletion of natural resources (50%).

- Accounting For Sustainability released a guide to incentivising action across the value chain. This will become increasingly important as many organisations will be required to start reporting on Scope 3 activities.

- The UK Infrastructure Bank has announced the first three pilots for its local authority advisory function – Bristol, Greater Manchester, and West Yorkshire.

Naresh Aggarwal