This blog is part of a regular series of blogs on the wide topic of ESG and items that have caught my attention. ESG is the ACT’s key theme for 2020 reflecting the growing interest in this area by our members.

For most of us 2020 was the year that would be marked by further progress on the ESG agenda culminating in COP 26 in Glasgow and the Biodiversity COP 15 in Kunming, China. However, as we all know COVID-19 has intervened and COP 26 has now been moved to November 2021 and COP 15 is being rescheduled. As a result of the pandemic, resources are being diverted by both the private and public sectors away from ESG activities to supporting companies and individuals.

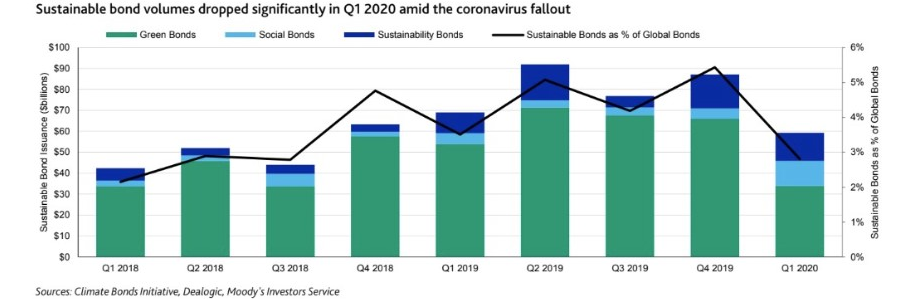

Despite this, the bonds markets in 2020 have already been active with sustainable bond volumes totalling approximately USD60 billion, of which green bonds represented 55%. The largest increase unsurprisingly was in the area of social bonds, with a number of development banks issuing “pandemic” bonds to support key businesses and individuals.

Key issues included:

• Republic of Ecuador issued the first ever sovereign social bond of USD400 million partially supported by a credit guarantee from the Inter-American Development Bank. The proceeds from the issuance will be used for housing loans with social and public interest for medium or low-income families

• Cadent, a large UK gas distribution company, issued the UK’s first “transition bond” of EUR500 million where proceeds will be used for eligible transition projects to retrofit gas transmission and distribution infrastructure (to facilitate future transmission of hydrogen and other low-carbon gases & reduce methane leakage), renewable energy, clean transportation, and energy efficiency

• Sydney Airport issued AUD100 million 20-year sustainability-linked bond in the form of a private placement under a multi-tranche, triple-currency transaction which raised around AUD600 million

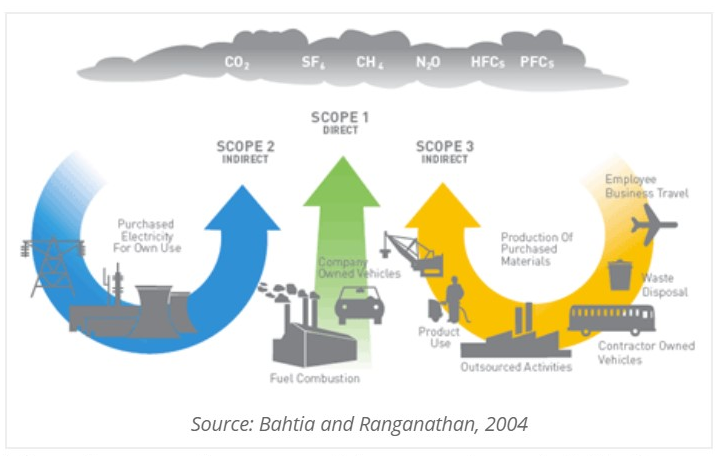

Greenhouse Gas (GHG) Protocol

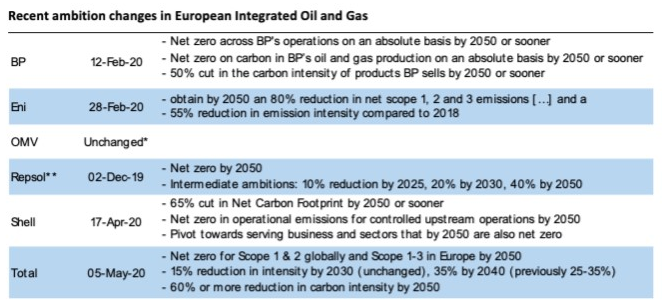

A number of companies have been making announcements recently on their ESG ambitions. In a recent report from the Transition Pathway Initiative (TPI), it was noted that the climate ambitions of European integrated oil and gas majors have strengthened markedly in the last six months, with Total, Shell, BP, Repsol and Eni all having made commitments to significantly reduce the carbon intensity of the energy they supply.

As the table below from TPI shows, many are making reference to the GHG Protocol in their reporting.

Life cycle emissions are all the emissions associated with the production and use of a specific product, from cradle to grave, including emissions from raw materials, manufacture, transport, storage, sale, use and disposal. The GHG protocol separates these into three scopes:

Scope 1 emissions are direct emissions produced by the burning of fuels of the emitter.

Scope 2 emissions are indirect emissions generated by the electricity consumed and purchased by the emitter.

Scope 3 emissions are indirect emissions produced by the emitter activity but not owned or controlled by the reporting emitter. They can often represent up to 90% of a company’s greenhouse gas emissions ..

Examples of Scope 3 include:

• Purchased goods and services

• Business travel

• Employee commuting

• Waste disposal

• Use of sold products

• Transportation and distribution (up- and downstream)

• Investments

• Leased assets and franchises

For many companies, the majority of their greenhouse gas (GHG) emissions and cost reduction opportunities lie outside their own operations. By measuring Scope 3 emissions, organisations can:

• Assess where the emission hotspots are in their supply chain;

• Identify resource and energy risks in their supply chain;

• Identify which suppliers are leaders and which are laggards in terms of their sustainability performance;

• Identify energy efficiency and cost reduction opportunities in their supply chain;

• Engage suppliers and assist them to implement sustainability initiatives;

• Improve the energy efficiency of their products; and

• Positively engage with employees to reduce emissions from business travel and employee commuting.

Oxford University report on the impact of COVID-19 on climate change

Oxford University published a report at the start of May which considered whether the pandemic would accelerate or retard progress on climate change.

The report is based on a survey of 231 central bank officials, finance ministry officials, and other economic experts from G20 countries and whilst the focus of this report is directed to policy makers, the findings are of relevance to organisations more broadly as they start to (re)consider their ESG agenda.

The report identifies five policy areas that are well-placed to contribute to achieving economic and climate goals. These are:

• Clean physical infrastructure investment;

• Building efficiency retrofits;

• Investment in education and training to address immediate unemployment from COVID-19 and structural unemployment from decarbonisation;

• Natural capital investment for ecosystem resilience and regeneration; and

• Clean R&D investment.