This blog is part of a regular series of blogs on the wide topic of ESG and items that have caught my attention.

1. The European Central Bank published its Opinion on the proposal for the Corporate Sustainability Reporting Directive (CSRD) as well as the timeline suggesting the adoption of the first sustainability reporting standards in Oct 2022. It welcomed the proposal and noted that current sustainability disclosure standards were not sufficient to address sustainability-related risks.

2. The International Sustainability Standards Board (ISSB) is being set up by the IFRS Foundation in time for the COP26 UN climate change summit in Scotland in November. Supported by organisations such as IOSCO and IFAC, the aim is to replace a patchwork of voluntary guidance with a single set of norms for firms reporting the impact of climate change on their business at a time when the volume of investment in companies with green credentials is rising.

3. The EC has adopted a NextGenerationEU (NGEU) Green Bond framework to proceed with a first green bond issuance up to €250 billion, which is planned for October 2021. Aimed at financing green investments and reforms in the EU, the NGEU Green bond framework is closely aligned with the European green bond standard. Overall, the framework will report on both allocation and environmental impact thus providing investors information regarding how their investments will be used.

4. A dedicated subgroup (#4) of the Platform on Sustainable Finance is advising the European Commission on minimum social safeguards and the possibility of extending the taxonomy to social objectives. Its draft report was recently issued and included the following observations:

Benefits:

• The need for investment in social sustainability, which means preventing social harm (for example, by ensuring companies respect human rights) and improving the provision of basic goods and services, especially for vulnerable people and groups.

• The need for investment in a fair transition, maximising the benefits of a sustainable economy while minimising hardship for workers, consumers and communities affected by that change.

• Meeting investor demand for socially orientated investment.

• Managing sustainability risks, including investment risks relating to human rights, labour standards and other social risks.

• The need to develop the definition and measurement of the essential characteristics of social investment.

• The report also identifies arguments against extending the Taxonomy to cover social objectives.

Drawbacks:

• Objectives of a social taxonomy go beyond the scope of the EU in social affairs, which are predominantly managed at a national level. It is not possible to define activities as "socially sustainable" or causing no significant harm without regard to national social contexts.

• A taxonomy might favour companies located in countries with more stringent social legislation, for example, in relation to labour standards.

• Potentially directing investment to certain companies, detracting from the need to support all companies to contribute to social sustainability, including job creation.

• Increasing an already heavy reporting burden for companies.

5. The Singapore Exchange Regulation (SGX RegCo) is proposing a roadmap for climate-related disclosures to be made mandatory in issuers’ sustainability reports (SRs) amid urgent demand for such information from lenders, investors and other key stakeholders. It is also consulting the public on requiring assurance of SRs and one-time sustainability training for all directors.

On climate reporting, SGX RegCo wants issuers to make disclosures based on recommendations of the Task Force on Climate-related Financial Disclosures (TCFD). The TCFD’s internationally recognised recommendations will guide companies in providing consistent and decision-useful information for market participants. This is a first step to better prepare issuers for reporting against anticipated global baseline sustainability reporting standards to be developed by the International Financial Reporting Standards Foundation, which build on existing work of leading sustainability reporting organisations including TCFD.

A phased approach to mandatory climate reporting is proposed.

• All issuers to adopt climate reporting on a ‘comply or explain’ basis for their financial year (FY) commencing in 2022.

• From the FY commencing in 2023 onwards, climate reporting will be mandatory for some sectors of issuers while ‘comply or explain’ will remain the approach for the others.

• From the FY commencing in 2024 onwards, more sectors of issuers will adopt mandatory climate reporting with the rest doing so on a ‘comply or explain’ basis.

6. The Taskforce on Nature-related Financial Disclosures (TNFD announced Taskforce Members and Launch of its Consultative Forum, Leveraging Global Nature and Finance Expertise. The Taskforce Members are convening for the first time on the 6th of October to kick off their work developing and delivering a risk management and financial disclosure framework to support a shift in global financial flows away from nature-negative outcomes and towards nature-positive outcomes. The finalised framework is earmarked for release in late 2023. However, a draft beta version will be circulated in early 2022 to be tested and refined via an open-innovation approach with market participants throughout next year.

The five initial Working Groups through which the specific, technical work will begin to develop the TNFD framework will focus on:

• Defining nature-related risks

• Data availability

• Landscape of standards and metrics

• Development of a Beta framework

• Pilot testing and integration

7. The TNFD Forum is a global multi-disciplinary consultative group of institutions launching with over 100 Forum members. These institutions share the vision and mission of the TNFD and have expressed the willingness to make themselves available to contribute to the work of the Taskforce. The TNFD Forum is open for membership and expected to grow over time as more organisations become aware of the importance of their engagement and come on board to support a shift in financial flows towards nature-positive outcomes. In addition to the already confirmed Forum members, a further 100 institutions have also expressed interest in joining the Forum in the short term.

1. A group of global private equity firms and pensions funds managing over $4 trillion in assets said on Thursday they have agreed to standardize reporting on environmental, social and corporate governance (ESG) performance of portfolio companies.

The group includes Canada Pension Plan Investment Board (CPPIB), Blackstone Inc (BX.N), Sweden's EQT AB (EQTAB.ST), Permira and CVC Capital Partners. ed by Carlyle Group (CG.O) and the California Public Employees' Retirement System (CalPERS), will track data on greenhouse gas emissions, renewable energy, board diversity and other metrics of companies in their portfolio.

Under the initiative, private equity firms will gather and report ESG metrics from their portfolio companies, starting from this year. Boston Consulting Group will aggregate the data into an anonymised benchmark.

2. The UK Government launched its first green gilt, with reports that investors had placed a record £90bn in orders for the bond. Projects such as zero-emissions buses, energy-efficient housing schemes, offshore wind projects and initiatives that improve climate adaptation such as flood defences and biodiversity improvements are all set to meet the criteria to access green finance. Sectors excluded from receiving bond proceeds include fossil fuel exploration, nuclear power, weapons, tobacco, gaming, palm oil and alcoholic beverages.

3. Deutsche Bank executed its first ever green repo transaction as part of a new initiative to broaden the range of ESG fixed income products available to clients. The transaction involved the bank transferring securities to long-standing client M&G Investments and receiving cash to fund Deutsche Bank’s green asset pool, including renewable energy projects such as wind or solar power plants and the improvement of energy efficiency for example, commercial buildings in line with the bank’s Green Financing Framework.

At the same time, the ICMA’s European Repo and Collateral Council has issued a summary report following its consultation on the role of repo in sustainable finance.

4. The consultancy firm Oliver Wyman issued its “Blueprint for a commercially smart climate transition” based on research with 27 global companies. It has also launched an interactive navigator tool that lets leaders see how far they need to go to close their emissions gap and exactly what they need to do to accomplish it. It assigns several actions out of 17 — like scaling low-carbon power generation or reducing transport emissions — to the world's most carbon-heavy regions and sectors. Each action in the navigator shows its mitigation potential, giving business and government leaders each piece of the puzzle to realize their 2030 climate goals.

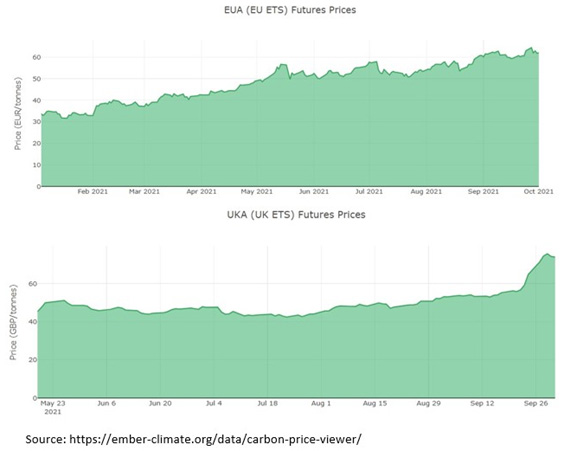

5. A recent report from the Carbon Pricing Leadership Coalition claimed that carbon pricing, including international cooperation through carbon markets, should be included in the arsenal of measures to enable the achievement to net-zero targets. Carbon prices must also be high enough to provide effective signals to society, to drive the level of investment and technological changes necessary to reach net-zero and be taken in conjunction with complementary policy actions to make carbon pricing relevant across company value chains. This can be achieved by expanding pricing mechanisms and coordination across countries to cover a higher proportion of global emissions. As the graphs below show, the price of carbon futures continues to rise and has almost doubled in the EU.

6. A credit rating and analysis firm based in Germany and focused on the European markets is launching the first dedicated database to display Carbon Intensity Indicator (CII) ratings for the world’s commercial maritime fleet. According to Scope ESG Analysis, the database product known as Ship Review, will enhance the transparency of ships’ environmental, sustainability, and reliability/safety performance by incorporating independent ESG assessments of more than 70,000 vessels based on estimates of several carbon intensity indicators, including the Annual Efficiency Ratio, the Energy Efficiency Operational Indicator, and total CO2 emitted in a year. According to Scope, by comparing the emissions of different ship types, ship management companies, and specific voyages, users can drill down and select alternatives that emit less CO2 per cargo carried.

7. Information and communication technology company Ericsson announced that it has signed a $2 billion sustainability-linked credit facility, tying its cost of debt to its progress on the company’s climate goals, and to its suppliers’ climate targets. Under the terms of Ericsson’s credit facility, interest margin will be linked to two KPIs, including the company’s goal to achieve carbon neutrality in its operations by 2030, and its ambition to have suppliers set 1.5 C° aligned climate targets. Ericsson’s supply chain represents the vast majority of the company’s carbon footprint, and the company has set a goal to engage with 350 high-emitting and strategic suppliers to set their own 1.5°C aligned climate targets by 2025.

8. The Science Based Targets initiative (SBTi), one of the key organisations focused on aligning corporate environmental sustainability action with the global goals of limiting climate change, announced the results of a research study indicating that while companies are increasingly setting climate targets, the vast majority fail to align with climate science.

The research, outlined in the newly published report, “Taking the Temperature: Assessing and scaling-up climate ambition in the G20 business sector,” found that of the more than 4,200 companies in the G20 that have set climate targets, only 20% are science-based. Results were slightly better in G7 countries, where 25% of targets were science-based, with only 6% of G13 (G20 countries outside of the G7) reaching this benchmark. The report found that several G20 countries did not have any companies with science-based targets, including Argentina, Indonesia, South Korea, Russia, and Saudi Arabia.