Official announcements

1. Key highlights from COP26 included:

- Fossil fuels. The agreement included references to the need for reduced fossil fuel use for the first time in the COP framework, though the language was weaker than many had hoped.

- Climate finance. The 2015 Paris Agreement called for developed nations to ramp support for their developing counterparts in the form of at least $100 billion in climate finance per year by 2020. The conference saw a significant step-up in climate finance pledges and urged full delivery of the $100 billion goal annually through 2025.

- Near term climate goals. The past two years had seen a dramatic increase in countries pledging to achieve net zero emissions, with 80% of global emissions now covered under these long-term targets. The pact calls for countries to revisit and strengthen their 2030 emissions targets, or Nationally Determined Contributions (NDCs) over the next year.

- Carbon markets. Six years after kicking of in the Paris Agreement’s “Article 6,” a rulebook for carbon markets has been established at COP26, marking a significant step in the development of the massive emerging market for carbon credits by providing a consistent and transparent framework.

2. The European Commission has delayed the implementation of disclosure requirements under the Sustainable Finance Disclosure Regulation (SFDR) related to sustainable investment products by financial market participants to January 2023, its second delay, resulting in application of the rules coming into place a year past the initially planned date.

The regulations require financial market participants and asset owners to provide disclosures including the manner in which sustainability risks are integrated into their investment decisions, and assessments of the likely impacts of sustainability risks on the returns of financial products.

The decision to push back to 2023 was made due to the “length and technical detail” of the standards, requiring “additional time in the adoption process.”

3. IOSCO issued its final report on Environmental, Social and Governance (ESG) Ratings and Data Products Providers. The 56-page report included the following recommendations:

- ESG ratings and data products providers could consider adopting and implementing written procedures designed to help ensure the issuance of high quality ESG ratings and data products based on publicly disclosed data sources where possible and other information sources where necessary, using transparent and defined methodologies.

- ESG ratings and data products providers could consider adopting and implementing written policies and procedures designed to help ensure their decisions are independent, free from political or economic interference, and appropriately address potential conflicts of interest that may arise from, among other things, the ESG ratings and data products providers’ organisational structure, business or financial activities, or the financial interests of the ESG ratings and ESG data products providers and their officers and employees.

- ESG ratings and data products providers could consider identifying, avoiding or appropriately managing, mitigating and disclosing potential conflicts of interest that may compromise the independence and objectivity of the ESG ratings and ESG data products provider’s operations.

- ESG ratings and data products providers could consider making adequate levels of public disclosure and transparency a priority for their ESG ratings and data products, including their methodologies and processes to enable the users of the product to understand what the product is and how it is produced, including any potential conflicts of interest and while maintaining a balance with respect to proprietary or confidential information, data and methodologies.

- ESG ratings and data products providers could consider adopting and implementing written policies and procedures designed to address and protect all non-public information received from or communicated to them by any entity, or its agents, related to their ESG ratings and data products, in a manner appropriate in the circumstances.

- Market participants could consider conducting due diligence or gathering and reviewing information on the ESG ratings and data products that they use in their internal processes. This due diligence or information gathering and review could include an understanding of what is being rated or assessed by the product, how it is being rated or assessed and, limitations and the purposes for which the product is being used.

- ESG ratings and data products providers could consider improving information gathering processes with entities covered by their products in a manner that leads to more efficient information procurement for both the providers and these entities.

- Where feasible and appropriate, ESG ratings and data products providers could consider responding to and addressing issues flagged by entities covered by their ESG ratings and data products while maintaining the objectivity of these products.

- Entities subject to assessment by ESG ratings and data products providers could consider streamlining their disclosure processes for sustainability related information to the extent possible, bearing in mind jurisdictions’ applicable regulatory and other legal requirements.

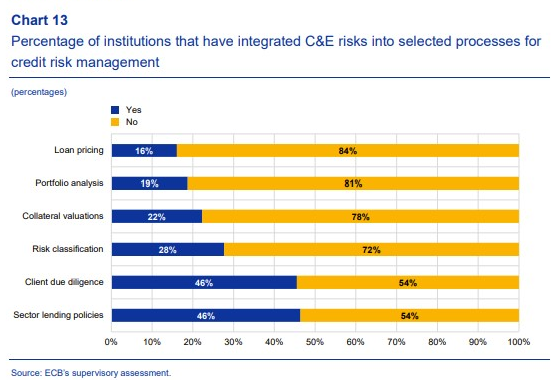

4. A recent report from the European Central Bank found that of a group of 112 significant institutions, none were close to fully aligning their practices with the supervisory expectations. In addition it found that while steps were being taken to adapt policies and procedures, few institutions had put in place climate-related and environmental risk practices with a discernible impact on their strategy and risk profile. It includes the following charts:

5. The European Central Bank published its Opinion on the proposal for the Corporate Sustainability Reporting Directive (CSRD) as well as the timeline suggesting the adoption of the first sustainability reporting standards in Oct 2022. It welcomed the proposal and noted that current sustainability disclosure standards were not sufficient to address sustainability-related risks.

Resources, Reports and Announcements

1. At COP26, the IFRS Foundation announced the creation of the ISSB and the consolidation with the CDSB and the Value Reporting Foundation (VRF) (which comprises the SASB Standards and the Integrated Reporting Framework). The merger of IFRS with the CDSB and the VRF offers the potential to accelerate the release of IFRS Sustainability Disclosure Standards, based on the updated prototype disclosure standards.

The IFRS Foundation’s Technical Readiness Working Group (TRWG) also published prototype climate and general disclosure standards, which reflect the consolidated efforts of the CDSB, the IASB, the TCFD, the VRF, and the World Economic Forum requirements and are expected to focus on issues relevant to enterprise value creation.

In the US, the SEC has responded with an all agency approach to growing investor demands for more and better ESG information since the Biden Administration came into office in January and is widely expected to announce new disclosure regulations for climate and other ESG-related issues before the end of the year. In the UK, the government, which had previously announced a commitment to make TCFD-aligned disclosures mandatory, recently announced it expects the ISSB standards will form the backbone of its corporate reporting requirements. In Canada, provincial securities regulators have proposed climate-related disclosure requirements for publicly-listed companies.

It is possible that final standards for both climate change and sustainability topics could be implemented more broadly between late 2022 and mid 2023.

2. ESG ratings and research provider Sustainalytics announced the launch of its Corporate Supply Chain ESG Solutions, aimed at enabling companies to assess and manage ESG risks within their supply chains.

3. Moody’s ESG Solutions quarterly Sustainable Finance report found that:

- Global sustainable bond issuance grew 25% year-over-year in the third quarter of 2021 to $217 billion, though volumes declined from the record-breaking Q1 and Q2 quarters, which saw issuances of $285 billion and $273 billion, respectively. Year-to-date, sustainable bond issuance reached $775 million at the end of Q3 2021, nearly doubling the $402 billion in the year-ago period.

- By bond type, green bond issuance was $115 billion in the quarter, up 18% year over year, and $380 billion year-to-date, increasing 75%, following weaker COVID-19 impacted quarters in H1 2020. Q3 Social bond issuance was $29 billion, declining 7% compared to the prior year period, following several record quarters driven by the European Commission’s EU SURE bonds program. Year-to-date social bond issuance of $173 billion as already surpassed the full year 2020 volumes. Sustainability bond issuance increased 26% year-over-year to $52 billion for the quarter, and more than 61% year-to-date to $160 billion.

- The fastest growing sector of the market remains the emerging sustainability-linked bond market, with issuance year-to-date of $62 billion, eclipsing the $9 billion issued in all of 2020. Sustainability-linked securities are an increasingly popular form of sustainable finance instruments, with attributes including interest payments tied to an issuer’s achievement of specific sustainability targets.

4. An alliance of financial institutions, investors and sustainable investment-focused service providers including HSBC, Deutsche Bank and the GRI have launched the ESG Book - a central source for accessible, transparent and comparable ESG data. It’s mission is to create ESG data as a public good, available to all companies, investors, standard-setters and stakeholders, and supports the ten principles of the UN Global Compact, which encompass human rights, labour, environment, and anti-corruption.

5. In a new survey - Climate Change & the People Factor from KPMG and Eversheds Sutherland many corporate executives expected their companies’ decarbonisation strategies to have a negative impact on their employees, with almost half expecting a high level of resistance from the workforce. While 34% reported that some adverse impact can be met with employee retraining and reskilling, 30% expect some positions to become redundant in a low-carbon organization, resulting in job losses.