This blog is part of a regular series of blogs on the wide topic of ESG and items that have caught my attention.

Although it’s a new year, somethings haven’t changed much. We still have COP 26 in Glasgow in November and Biodiversity COP 15 in Kunming, China in May.

- A frequent complaint I hear is the multiplicity of reporting frameworks. At the end of 2020 the Sustainability Accounting Standards Board (SASB) and the International Integrated Reporting Council (IIRC) announced plans to merge and form the Value Reporting Foundation. The VRF aim to provide investors and companies with a comprehensive corporate reporting framework across the full range of enterprise value drivers and standards to drive global sustainability performance. The merger will advance the work of CDP, CDSB, GRI, IIRC and SASB in the Statement of Intent To Work Together Towards Comprehensive Corporate Reporting, which outlines a vision for a comprehensive corporate reporting system. By integrating the IIRC and SASB – two entities that enable enterprise value creation – this merger demonstrates momentum towards simplifying the corporate reporting landscape. The Foundation’s planned CEO noted that the Value Reporting Foundation stands ready to engage with the efforts of the IFRS Foundation, IOSCO, EFRAG, and others working towards global alignment on a corporate reporting system.

- The Impact Investing Institute submitted its response to the IFRS Foundation’s Consultation Paper on Sustainability Reporting. The III is a non-profit organisation, which brought together the Taskforce for Growing a Culture of Social Impact Investing in the UK and the UK National Advisory Board on Impact Investing.

- ICMA issued a handbook to provide clear guidance and common expectations to capital markets participants on the practices, actions and disclosures to be made available when raising funds in debt markets for climate transition-related purposes, whether this be in the format of:

- Use of Proceeds instruments, defined as those aligned to the Green and Social Bond Principles or Sustainability Bond Guidelines or,

- General Corporate Purpose instruments aligned to the Sustainability-Linked Bond Principles.

- The UK’s Climate Change Committee issued its Sixth Carbon Budget. It’s recommended pathway requires a 78% reduction in UK territorial emissions between 1990 and 2035. In effect, bringing forward the UK’s previous 80% target by nearly 15 years. This will be achieved through four key steps:

- Take up of low-carbon solutions

- Expansion of low-carbon energy supplies

- Reducing demand for carbon-intensive activities

- Land and greenhouse gas removals

- HSBC shareholders filed a climate resolution ahead of the bank’s annual meeting in April calling on HSBC to publish a strategy and targets to reduce its exposure to fossil fuel assets. The bank has already pledged up to $1tn of support in the next decade to help clients become more environmentally friendly. It also cut its oil sands financing from $1.3bn in 2017 to $231m in 2019, leaving it only the ninth largest bank in that sector, according to Rainforest Action Network data.

- Having won a tender issued by the EU, Blackrock issued an interim study on the development of tools and mechanisms for the integration of ESG factors into the EU banking prudential framework and into banks' business strategies and investment policies.

Blackrock has created Aladdin Climate to help investors quantify climate risk in their portfolios. In partnership with Sustainalytics and Refinitive it enables investors to measure the physical risk of climate change and the transition risk to a low-carbon economy on portfolios with climate-adjusted security valuations and risk metrics. Blackrock claims the platform allows investors to analyse climate risk and opportunities at the security level and measure the impact of policy changes, technology, and energy supply on specific investments.

- At a webinar hosted by the Bank of England, Sarah Breeden, who leads the Bank’s work on climate-related risks, said the cost of pollution allowances will need to rise significantly in order to achieve targets in the Paris Agreement to limit global warming to below 2 degrees Celsius. Carbon prices may even exceed $100 if the transition to a low carbon economy is abrupt, or bumpy, she said. The current price to pollute in the European Union is around 33 euros ($40) a ton. “I do think if risk is priced, it will drive the right behaviors,” said Breeden

Hundreds of businesses have started to set internal carbon prices, and they’re under pressure to ensure that analysis will guide investment decisions and provide an incentive to rein in emissions. Last year, the British oil major BP Plc adopted an assumption that prices would reach $100 per ton in 2030, up from the $40 per tonne figure it previously factored in.

The number of companies using an internal carbon price rose from 607 in 2017 to 853 in 2020, according to CDP. Carbon in the EU emissions trading system has averaged 25 euros a ton over the past year and has been over 30 euros for the past month. But Breeden said businesses should consider future carbon prices, rather than those today.

The U.K. government has said it will require companies to report on their climate change risks by 2025. The full details of that policy are still being worked out by the Department for Business, Energy and Industrial Strategy. Breeden said the government was seeking to strike a balance to ensure that private companies are also required to disclose, but that small businesses are exempt.

She urged businesses to start investigating their exposure to climate risk, even if they don’t yet have all the data. “Don’t let imperfection be an excuse for inaction,” she said.

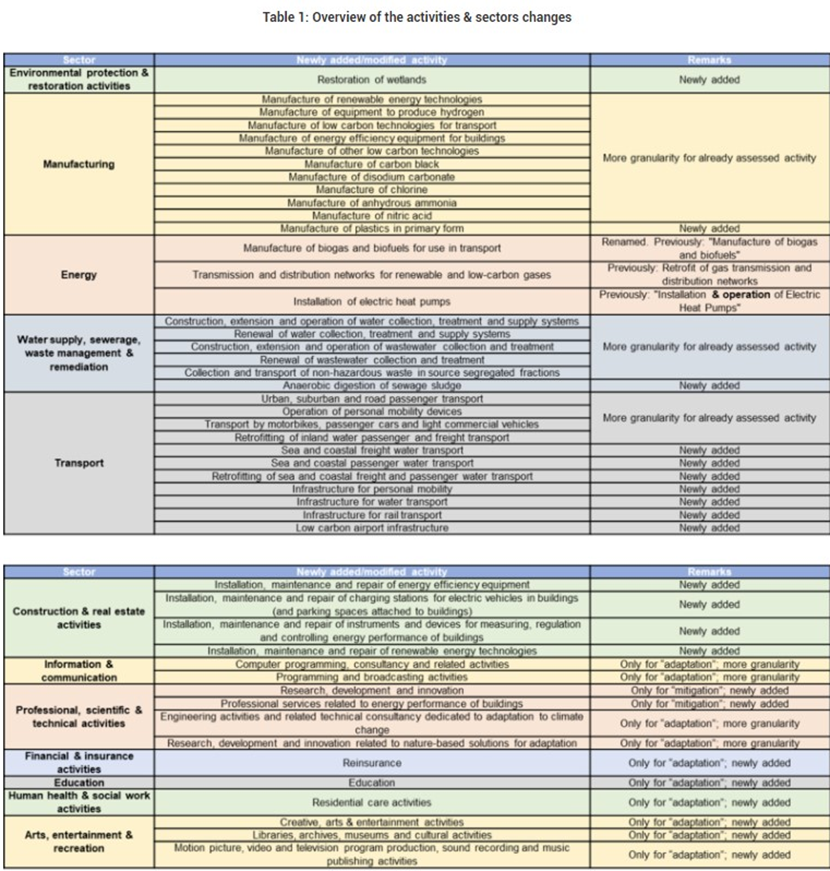

- In November 2020 the European Commission published the Draft Delegated Act under the Taxonomy Regulation on climate change mitigation and climate change adaptation. This legal text specifies the technical screening criteria under which specific economic activities qualify as contributing substantially to climate change mitigation and adaptation and for determining whether those economic activities cause significant harm to any of the other relevant environmental objectives. The activities and criteria considered to be enshrined in law are based on the recommendations of the Technical Expert Group (TEG) on Sustainable Finance published in March 2020. The Draft Delegated Act for these two objectives is now under a four-week public consultation before approval by the European Parliament and Council of the European Union (EU) by the end of the year.

The technical screening criteria for the four other environmental objectives — sustainable use and protection of water and marine resources; transition to a circular economy, waste prevention and recycling; pollution prevention and control and protection of healthy ecosystems — will be established by the end of 2021.

Compared to the TEG’s March 2020 report, this Draft included more granularity for the classification of activities in manufacturing, energy, transport and building sector. Sub-categories have been created within existing sectors, in addition to newly created sectors such as “Information & communication”, “Professional, scientific & technical activities”, “Financial & insurance activities”, “Education”, “Human health & social work activities” and “Arts, entertainment & recreation” sectors. Metrics and criteria have been developed for newly assessed activities, reaching a total of 90 activities assessed for mitigation (against 70 in the previous version) and 98 for adaptation (against 69 in the previous version). The table below provides a synthetic view of the changes across the categories of activities assessed. Sea and coastal freight and passenger water transport or low carbon airport infrastructure have been included in the technical screening criteria for “brown activities” that were previously out of the TEG’s review scope.